By John Helmer, Moscow

Theologians may wrestle to Kingdom Come before they will agree that a gusher of faith can be drilled out of a bedrock of reason. In the case of junior Russian oil companies taking money from investors on the London Stock Exchange (LSE), the gushers are proving to be short-lived. The loss of faith can be measured in the collapse of share price and market capitalization – and in the files of Mirabaud Securities, the Swiss promoter of a great deal of short-lived enthusiasm.

Timan Oil and Gas, for example, failed to produce what it promised from prospects in the Arctic region of Timan Pechora; defaulted on its loans; delisted its shares; and is now in liquidation [1]. Ruspetro, operating in the Khanty-Mansiysk region of western Siberia, listed [2] its shares at the start of 2012, but in two years they have collapsed to a tenth of their peak value. Mirabaud was a lead manager for both issues.

Imperial Energy, a junior operator in Tomsk, southeastern Siberia, was bought out of the LSE in 2008 when the Indian government paid £1.4 billion ($2.1 billion) for the lossmaker. Today it cannot sustain its production level, despite the money which has been thrown [3] at it. The accounts of ONGC Videsh, the state owner, reveal [4] that Imperial Energy is still a lossmaker, while the asset value of the Russian unit is currently booked at $607.99 million.

Then there is the Chinese adventure — Nobel Holdings Investments, with producing wells in Timan Pechora and exploration prospects in Khanty-Mansiysk. In 2009, despite licence and reserve count disputes with LUKoil and the federal licensing authority, Rosnedra, China Investment Corporation (CIC), a Beijing-controlled fund, valued the Russian oilfield reserves at HK$4 billion ($516 million); paid $100 million for a 45% shareholding, ostensibly valuing the entire company at $222 million. CIC promised to invest another $450 million for the costs of drilling and arranged with another two Chinese entities, Oriental Patron Financial Group and Kaisun Energy Ltd., for a Hong Kong Stock Exchange listing to resell their shares to all-comers.

Had that happened when it was promised, Nobel might have been the very first Russian business to be listed in Hong Kong, months before United Company Rusal, the state aluminium monopoly. But this didn’t happen; and since 2009 Kaisun Energy has been lossmaking, its current market capitalization close to zero on the Hong Kong exchange. Though their common parent Oriental Patron, Kaisun Energy is associated with the London-listed aluminium trader and producer Vimetco, whose Romanian business was notorious in the past. Today it, too, is lossmaking with a market capitalization that is equally worthless.

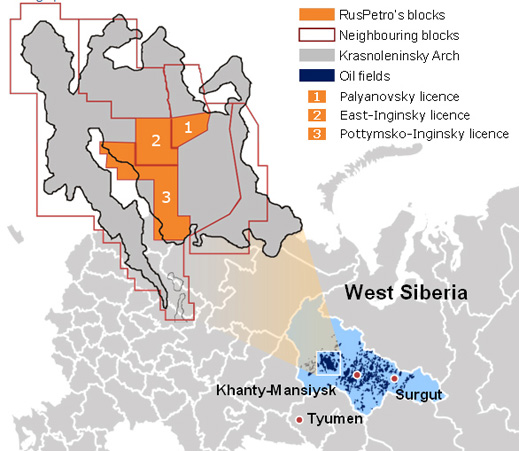

For souvenirs of where the oil was purportedly buried in such volumes as to persuade investors there was a fortune to be made — only it wasn’t — here are the asset maps of Ruspetro:

And of Nobel Holdings Ltd (aka Nobel Oil):

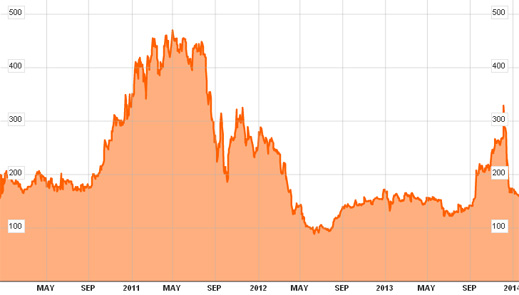

The geography of Russian asset evaporation doesn’t mean that you can’t get rich buying into Russian oilfields which none of the major Russian oil companies takes seriously enough to want. Just ask Mikhail Gutseriyev (image foreground) and Alexei Khotin (rear). Theirs is the story of Exillon Energy, which began its public shareholding in London at the end of 2009. At listing its share price was £1.53, with a market cap of £247 million. Peak value was in April 2011, when the share price hit £4.68, £756 million in market cap. Between mid-2012 and mid-2013 the share price collapsed to the range of 85 to 120 pence. Its recovery since then has been stimulated by Gutseriyev’s and Khotin’s buy bids, and by speculation on their intentions. That has now subsided, and this week Exillon’s share price is down where it started — £1.59 per share, £258 million in market cap.

EXILLON ENERGY SHARE PRICE OVER 5 YEARS

Source: Bloomberg

On every downturn, Mirabaud, underwriter of Exillon’s share sales on the LSE, has claimed to find an opportunity. A year ago, for example, conceding there had been “setbacks”, Mirabaud reported [5] to the market: “it is hardly an exception to the rule and recent operational performance on the ground has been strong. Indeed, we would argue that the outlook for Exillon is rosier than it has been for some time.”

By contrast, suggests an American hedge fund manager, the Exillon story is a case of market manipulation by a string of shareholders who convinced the market there would be a bidding war for shares as the company’s oil reserves appeared to be increasing. The starting sellers, according to this source, made substantial profits. But the remaining shareholders bought at premium prices which have failed to hold. “It’s interesting how all these Russian players came in and within weeks they have walked away already.”

In theory, the valuation of oil drillers depends on the volume of reserves which can be proven, estimated or projected underground. To that the assumption is added that these barrels can be lifted to the surface, and sold to the market. Ahead of initial public offerings, international reserve estimators like DeGolyer & MacNaughton and Miller & Lents are commissioned to make these calculations. Exillon’s London prospectus, for example, presents 78 pages of claims from Miller & Lents. From these, the promoters of the Exillon share sale (including Mirabaud) concluded [6]: “As part of its strategy, the Group intends to increase production which, according to Miller and Lents, is expected to peak at an average of approximately 60,107 barrels per day by 2014 and 101,959 barrels per day by 2016, based on 2P reserves and 3P reserves, respectively, and under the Group’s associated development plan. This increase is expected to be achieved by increasing the number of wells drilled per year, improving infrastructure to provide for all-season production and by enhancing production technology, including horizontal drilling, water flooding and production optimisation.”

In practice, as Ruspetro’s short career on the LSE has already demonstrated, schemes of horizontal drilling, hydrofracturing (fracking), and water injection run into the problem that wells run dry quicker than anticipated. Only by constant drilling of new wells to replace the depleted ones can production levels stay stable. To prevent output falling, however, can be costly.

In stock market terms, what this means is that a pyramid of sale and resale expectations must be built above ground, while underground, oil recovery techniques are pumping out the law of diminishing returns. New share issues must be sold to novice investors in order to cover rising costs. As shareholder disappointment grows, and the share price falls, the risk grows that the premium incoming share-buyers pay will be lost.

When Exillon commenced listing, the prospectus claimed its Timan oil output was running at 2,879 barrels per day; its West Siberian rate was 3,201 bd. According to the latest production report available at the LSE last week, the Timan rate in December was 3,927 bd; the West Siberian rate, 14,804 bd. Exillon’s combined [7] average flow rate for the fourth quarter came to 18,731 bd. A solid improvement over four years, indeed. But nowhere near the Miller & Lents estimate, nor the Mirabaud promo. For either of those claims to come true this year, Exillon will have to more than treble well-flow. At the Timan wells, whose production growth has been just 9.1% per annum, even with purchases of extra drilling areas, that looks like an impossibility.

Then there is wishful thinking. Sustaining Exillon’s share price have been announcements of big gains in reserves from Miller & Lents; much more modest improvements in sales revenue and earnings. The annual report for 2012 reveals that costs jumped by 59% as the number of wells drilled grew by 50% — that’s a faster rate than the 45% overall growth in output. After making a loss in 2011, the financial result for 2012 [8] was a net profit of just $12.1 million.

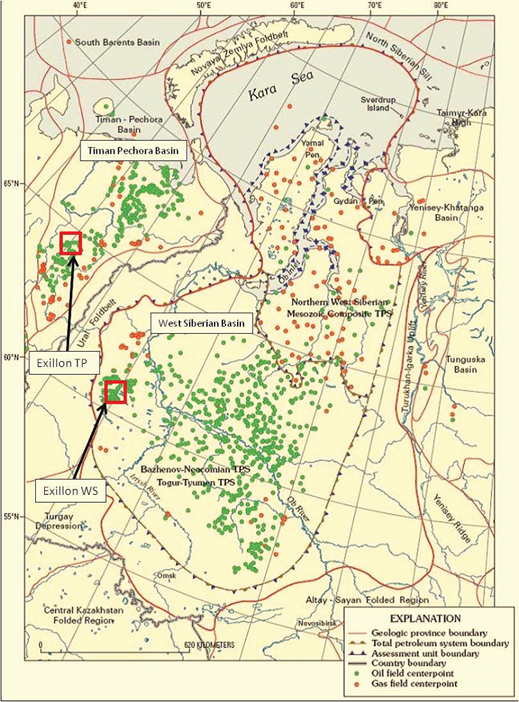

Here’s where Exillon’s assets are located geographically:

Source: http://www.exillonenergy.com/ [9]

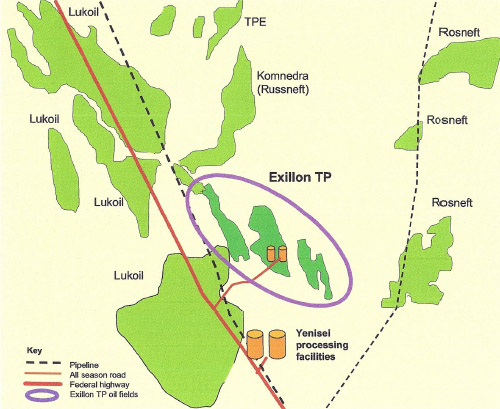

And here is the company’s diagram of where its Timan oil wells are located in relation to the major operators nearby:

If Exillon’s oil production is likely to become as voluminous, and grow as fast as the company has been claiming, LUKoil, whose wells share access to the Transneft pipeline to market, ought to be interested, not least to protect its own oil from being shut out of the pipeline. Asked if it has considered a bid for takeover and consolidation, a spokesman for LUKoil said the company “is not interested in this asset.”

A year ago, following a 66% drop in Exillon’s share price from its April 2011 peak, one of the minority shareholders, Worldview Capital Management (WCM), attacked Exillon’s management and board, accusing them of faulty strategy, misleading and inaccurate reporting, and feathering their own nests. With a 14.9% shareholding, WCM charged board chairman David Herbert and chief executive Mark Martin (right) with conflict of interest. (Both men came to Exillon from jobs promoting the share sale at ING Bank. Herbert was also associated with the Timan Oil & Gas collapse.) WCM’s bill of particulars also accused Exillon’s control shareholder, Maksat Arip, of conflict of interest and cash stripping.

A year ago, following a 66% drop in Exillon’s share price from its April 2011 peak, one of the minority shareholders, Worldview Capital Management (WCM), attacked Exillon’s management and board, accusing them of faulty strategy, misleading and inaccurate reporting, and feathering their own nests. With a 14.9% shareholding, WCM charged board chairman David Herbert and chief executive Mark Martin (right) with conflict of interest. (Both men came to Exillon from jobs promoting the share sale at ING Bank. Herbert was also associated with the Timan Oil & Gas collapse.) WCM’s bill of particulars also accused Exillon’s control shareholder, Maksat Arip, of conflict of interest and cash stripping.

Exillon’s performance, according [10] to WCM, was far weaker than it had disclosed to the market. “The reality is that the actual average daily production has in fact fallen below guidance for both the full year (12,862bopd vs 14,303bopd or minus 10%) and for the final quarter of 2012 (15,218bopd vs 17,398bopd or minus 13%). In addition, it is well below the forecast average daily production from proven reserves as projected in the Company’s independent geological report in February 2012”.

Andrey Kruglykhin of WCM told [11] the Financial Times: “Worldview believe that the Board has the wrong strategic focus by developing its high risk and less profitable assets in the Russian region of Timan-Pechora, which is diverting capital and other resources away from developing its assets in Western Siberia that have been shown to produce higher returns.”

Exillon had distinguished itself in one respect, WCM noted. It is the only Russian oil company to have been convicted of listing rule violations by the UK regulator, the Financial Services Authority (FSA). That indictment can be read in full here [12]. The FSA (now the Financial Conduct Authority, FCA) issued an unprecedented fine of £292,950 against Arip.

When WCM found itself outvoted by Arip and other shareholders, it decided to sell out. That didn’t happen until September of 2013, when Gutseriyev purchased the stake. Weeks before, Arip had attempted to repurchase a majority of the shares, but his move failed for lack of cash or borrowing capacity. That stemmed from conduct which has landed him as one of several defendants in a UK High Court proceeding. There Arip and his partners are accused [13] by the Kazakhstan Kagazy group of companies of “two large frauds, known in this action as the PEAK and the Astana frauds, by which the Defendants have stolen something over US$ 135 million…The Defendants deny the frauds altogether.”

Arip tried, but failed, to keep the evidence in the fraud case from becoming public “on the grounds” – reads the court judgement – “ that its subject matter is relevant to a pending public takeover bid [for Exillon] and…that further publicity is likely to cause damage to the bid’s success.” On November 20 last, Justice David Mackie ruled: “Someone is not telling the truth”; he reiterated the order locking up £70 million of Arip’s funds.

By then Arip was out of the running for Exillon, and Gutseriyev (right) claimed to be bidding for a takeover, eliminating Arip altogether. On the face of it, Gutseriyev’s bidding suggested that he was consolidating oilfields with those already operated by Russneft which Gutseriyev owns, along with his banker and trader, Glencore [14].

By then Arip was out of the running for Exillon, and Gutseriyev (right) claimed to be bidding for a takeover, eliminating Arip altogether. On the face of it, Gutseriyev’s bidding suggested that he was consolidating oilfields with those already operated by Russneft which Gutseriyev owns, along with his banker and trader, Glencore [14].

But by the end of December, Gutseriyev had sold out. Arip was gone too. The new shareholding lineup, according to Exillon, is Seneal International, a vehicle belonging to Alexander Khotin, which is holding a stake carefully calculated to avoid triggering the LSE’s mandatory buy-out offer to minority shareholders — 29.99% [15]. Khotin paid a premium almost 50% above Exillon’s market price before the sale was announced. Today Khotin’s stake is worth 58% less than he paid for it. That’s £106 million in paper loss.

The second shareholder is Alexander Klyachkin’s front company, Sinclare Holdings; his stake is 26.7%. The market disclosures [16] reveal that he paid almost as large a premium as Khotin’s, and his loss has been as great, at least on paper — £88 million. Measured against Exillon’s current share price Khotin and Klyachkin have reported to their banks that their combined equity loss to date is £194 million ($320 million).

Together, they now exercise an operating majority, and this week they began by appointing Russian trusties to positions previously dictated by Arip, Herbert and Martin. If Khotin and Klyachkin act in concert to manipulate their share price, they are breaking the UK Takeover Code. The other two shareholders with more than 5% are institutional funds of Capital Research & Management (6.95%) and Schroders (5.23%).

In December Black Rock, which had been sceptical of the Ruspetro promotion and avoided buying its shares in 2012, speculated on a rise in Exillon’s share price, buying 1.1%. In the following month the Black Rock wager lost 30% of its value.

Khotin is playing safe by keeping mum. In the Moscow press he and his father Yury are reported to own a substantial portfolio of commercial real estate in the city; how much of this value is clear of mortgages held by Sberbank, Alfa, Otkritie and other lenders isn’t known. Khotin junior avoids appearing in public and has made no public statement on his intentions for Exillon. At least one Moscow press report claims [17] he has had trouble with VTB over repayment of a Rb6.26 billion ($190 million).

Speaking through an LSE release by Seneal, Khotin said on December 4 he “is currently reviewing potential opportunities which include the possibility of making an offer for Exillon, however no decision has yet been made with regard to further action. At this stage, there can be no certainty that the RusOil group will make an offer for Exillon.” A fortnight later, Khotin said [18] he “does not intend to make an offer for the Company.” Speaking [19] this time through Sberbank, Khotin and the bank claimed they might change their minds, either to buy or to sell to a takeover bid, over the next six months.

Klyachkin also owns Moscow real estate, including the Azimut hotel group and the Metropol Hotel of Moscow. These two, plus CRM, Schroders, and Black Rock are all portfolio stakeholders, ready to sell and resell if the price is right. According to Andrei Polischuk, a Raiffeisen analyst, “the asset can be resold later. We see that the consolidation is clearly taking place, but the assets are bought with a premium. Such an asset already engaged in extraction will be interesting to all oil companies which expect to increase production. But what kind of struggle [there will be] between shareholders and buyers, I cannot say.”

Otkritie Bank analyst Alexander Burgansky reported to clients in November that an asset-based valuation for Exillon should give a target share price of £2.26 (226p). But he acknowledged that competition would drive this upward, as indeed it did. “We believe a multiple-based approach to valuation is now more appropriate, given the substantial synergies that could be achieved by combining EXI’s production with the neighbouring assets of its potential suitors. Based on the mid-range EV/2P reserves multiple of $1.75/boe, we have increased our target price by 48% to GBp334, reiterating our BUY rating.”

£3.28 per share was the limit for Exillon on December 4. From then until now Khotin and Klyachkin have been holding a shrinking bag.

Among the Russian oil majors this week no enthusiasm is expressed for a bidding contest to push Khotin’s and Klyachkin’s resale price above the level they have already paid. LUKoil, Rosneft, Gazpromneft, Bashneft, and the Sistema group disclaim interest in Exillon at any price.