By John Helmer in Moscow

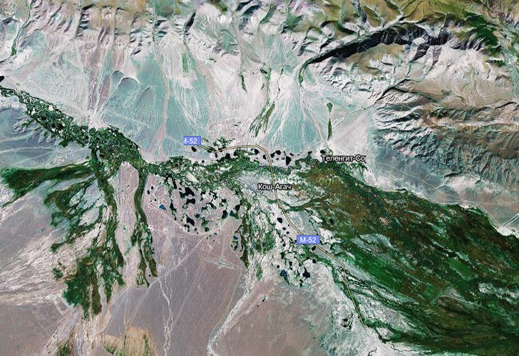

Kosh-Agach is a steppe word meaning ‘so long, tree’. It’s the world’s end, the driest and direst place in fareastern Russia at a remote corner where the frontiers of Kazakhstan, Mongolia, and China meet. It is also the location of a large reserve of rare metals, including cobalt. So rare is cobalt that since 2008 Russian law doesn’t allow foreigners to dig it out of the ground, sell it, or export it without special permission.

So why has the European Bank for Reconstruction and Development (EBRD) spent $30 million so far on investing in a project, details of which it insists on keeping secret? Why are none of the other foreign investors partnering EBRD in the mine project identifying themselves, or reported in the EBRD project documents?

The EBRD is financed by 61 shareholding countries of Europe, North America, and Australasia, plus the European Union and the European Investment Bank. The EBRD’s website claims the bank “seeks to develop a sound investment climate based on an effective legal and regulatory framework and promotes corporate governance, including sound management practices, a firm stance against corrupt practices, disclosure of information, and clear and consistent accounting and auditing practices.”

In practice, this is less than true. Olivier Descamps (picture, centre), managing director of EBRD for eastern Europe and Central Asia, is responsible for sector projects like Karakul. To the south, he is also responsible for Tajikistan, where he has supervised external financing for government corruption that has been exposed by the UK High Court, a Norwegian parliamentary committee, the US Government, even the International Monetary Fund and World Bank.

Another EBRD executive, Enery Quinones (picture, right), is in charge of legal compliance and anti-corruption. She consistently refuses to answer questions about her supervision of EBRD lending to Tajikistan.

On January 8, 2008, this is what the minutes of the EBRD board of directors report as happening at Kosh-Agach: “The Board approved an equity investment of up to USD 30 million (EUR 21.4 million) to Imperial Mining Holding Company. The equity investment will be used to finance preparation of a full feasibility study (including a full international-standard EIA), implement preparatory work for the development of Karakul cobalt-copper deposit in Altai region of Russia, and expected acquisition of nearby satellite deposits.”

The minutes record that the decision was taken by the then president Jean Lemierre (picture, front left), three of his deputies, including the EBRD’s chief lawyer. Voting in favour were 22 directors and 21 alternates. The director for Russia voted in favour; her name is Elena Kotova, and she is still the Russia director.

Seated around the walls of the board room, and attending in a staff capacity, were 22 EBRD executives, Descamps and Quinones included.

Almost all equity investments, mine project loans, and cash disbursements the EBRD has made in Russia are heavily documented in the bank’s public record before they are approved at board level. EBRD says that from its inception in 1991 it counts 613 projects altogether in Russia, and has paid out €12.4 billion. To count only mining and natural resource projects, there have been 25. Five of these focus on timber, gold, zinc, iron-ore, and mineral water; all the others involve energy resources, such as oil and gas. There is no reference to Imperial Mining or the Karakul cobalt mining project.

Counting the EBRD’s equity investments in Russia since 1991, there are more than 40 projects in total. The money has gone for shares in banks, brokerages, venture funds, regional development funds, a truck maker, carmaker, railway operator, airline, and a shipping company. The list is interesting because at least two of the banks, in which EBRD invested, disappeared in scandalous circumstances – Tokobank and Inkombank. Again, there is no reference to an equity interest in Imperial Mining or the Karakul cobalt mining project.

Here is EBRD’s complete list of 395 project, disbursement, and investment identifications since 1991. They range from sausage factories to bakeries, telephones to bottles, sewers to supermarkets — but not a reference to Karakul cobalt.

In short, unlike any other EBRD payout to Russia for mining resources, there is just a 2-sentence record that the board approved it – and nothing else. EBRD’s spokesman Anthony Williams was asked to say whether the equity investment EBRD has made in the venture is in a Russian company, or in a company controlled by the Oberoi group? whether EBRD believes the licence it has spent $30 million to exercise carries mining rights, or is limited to exploration and proving? And finally, whether EBRD knows that, according to the Russian law on mining strategic metals, cobalt is prohibited for mining by a foreign company without Kremlin permission?

Williams answered: “I have no comment to make on this issue”. Rarely can so little mean so much that EBRD wants to keep secret.

But first, consider the Kosh-Agachinsky region, in the southeast corner of Russia’s Altai territory:

A travelogue reports that the steppe hereabouts is “extremely interesting and exotic for the traveler from the viewpoint of its landscape, flora and fauna, with a slightly undulating plain at the altitude of 1700-1900 metres above the sea level, surrounded by mountain ridges covered with snow. Severe climate, dry and windless, means that the permafrost runs to 90 metres in depth. Wormwood and thorn bush are the only obvious vegetation.

| Pressed wool rugs (felt) are of special interest; the patterns will be recognized as more Kazakh than Russian. |  |

| But cobalt is even more interesting. The metal is used in diverse industrial and military applications. The most serious of these is in superalloys, which are used to make jet engine parts. It is almost always mined as a by-product of other more abundant metals. Currently, more than half of the world’s supply is produced as a by-product of copper mining and refining in Democratic Republic of Congo and Zambia. Cobalt production in Russia and most other countries is a by-product of nickel mining. Although some producers can increase or decrease the amount of cobalt mined or refined, most cobalt production is ultimately dependent on the production of copper and nickel. |  |

The global bust for commodities and metals that began in autumn of 2008 resulted in reduced demand for and supply of cobalt. According to a report from the US Geological Service (USGS), during the first half of 2009, the world availability of refined cobalt was 13% lower than that of the first half of 2008. This decline was primarily because of a decline in 2009 production from China, and the closure of a Zambian refinery in late 2008. During the second half of 2009, a strike at a company in Canada resulted in reduced production of refined cobalt from that country. Beginning in late 2008, production of cobalt-bearing concentrates and intermediate metals was hurt by cutbacks at many nickel mines around the world, and at some copper-cobalt operations in DRC (Kinshasa). Financing, construction, and startup of proposed brownfield and greenfield projects were delayed because the demand for the metal was falling, along with prices; and banks weren’t ready to lend to new mines.

The chart shows cobalt falling like a stone – down 73% from the May 2008 peak to the December 2008 bottom. Since then the price recovery has been modest.

Vale (Brazil), BHP Billiton (Australia), Xstrata (Switzerland), Teck Resources (Canada), Antofagasta Plc (UK), and Katanga Mining (Switzerland) are the biggest of the mining companies which produce cobalt.

Norilsk Nickel is Russia’s sole miner of cobalt; the two other Russian producers of copper do not have cobalt by-production. But Norilsk Nickel says as little as possible about its cobalt reserves or output. The last financial report for 2009 gave no information at all. The 2008 report indicated that the main company had signed contracts to provide up to 6,500 tonnes of cobalt per year for refining at the OM Group’s Harjavalta plant in Finland, which Norilsk Nickel had taken over the year before.

Output numbers appear from time to time when Norilsk Nickel executives let them slip. In 2004, when a new Russian cobalt refinery was being planned, its annual capacity was said to be 2,500 tonnes. In the first half of 2008, when the OM refining deal was disclosed, cobalt production for that period was said to be 1,160 tonnes.

Norilsk Nickel’s annual report for 2009 avoids revealing cobalt production for the year, but notes that revenues were down on account of falling price. “The main reason for the decline in revenue from the sale of by-products was a sharp fall in sales prices of rhodium — from USD 6,600 per ounce in 2008 to USD 1,600 per ounce in 2009, and cobalt — from USD 73,000 per tonne in 2008 to USD 32,500 per tonne in 2009.” The report fails to disclose revenues from cobalt sales.

Norilsk Nickel’s main cobalt reserves are hidden. In a pseudo-disclosure, deposits under exploration, which are described in the company’s literature, are reported to contain a grand total of 850 tonnes, according to the Russian C1 and C2 classifications.

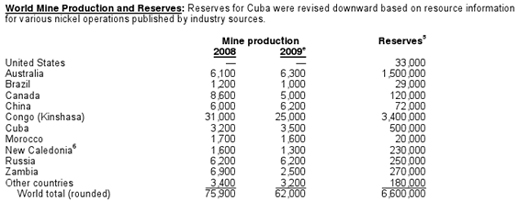

This is how the USGS reports Norilsk Nickel’s cobalt output and reserves, compared to other countries. The reality may be more or less, but because of the military uses of the metal, how much Russian holds underground in reserves, in stocks above ground in strategic stockpiles, and in annual trade remains a classified secret:

Source: USGS, June 2010

Altai regional sources report they have been hoping against hope that they are sitting on a cobalt mine of great value. Exploration began in the Soviet period, between 1978 and 1985. A deposit licence was issued in January 2006 to a Russian company called Altai Ruda Metall (ARM, “Altai Ore and Metal”). In May of 2007, this outfit told a local newspaper that it had “carried out technological expertise, and that currently an environmental assessment was being completed. Negotiations [were under way] with the European Bank for Reconstruction and Development to allocate a large loan to a mine production. The timing is not yet known, [the project is] waiting for the completion of appraisals.” Six months later, the EBRD came through with $30 million — far from enough to build a mine, but more than was needed to complete a bankable feasibility study. No reserves have been published, and the Ministry of Natural Resources in Moscow isn’t saying what their estimates are. The only clue to the deposit is a report that from drill samples, the ores are believed to contained 0.23% cobalt, 0.15% bismuth,0.32% copper, 0.55% tungsten trioxide, and traces of vanadium and gold.

| A regional environmental protection publication reported this year that if the mine goes ahead, it may destroy the habitat and migratory pattern of the argali, the horned mountain sheep, and several other rare species, including the steppe hawk. |  |

EBRD claims that it subjects all its project loans and investments to tough environmental compliance standards and impact assessments. But nothing appears to have been done before it handed out the cash this time.

Ilya Smelyansky, an expert for the Siberian Environmental Centre in Novosibirsk, has reported to the Bird Protection Union of Russia that he and his colleagues have held talks with ARM and Imperial Mining group on the impact of mining on bird life in the area. He confirms that “one deposit [Karakul] is already taken on licence by the company AltaiRudaMetall (Imperial Mining) and is being prepared for development; the rest [of the deposits] are included in the list of sites for auctions to be held in the near future.”

Smelyansky is in the field at present; his mobile telephone is turned off, and he is unavailable to answer questions. According to his report, the Siberian Environmental Centre and the Bird Protection Union want to form “a coalition of environmental organizations, which should seek recognition of the special status of the [Kosh-Agachinsky] territory and full compliance with environmental legislation by the Government of the Altai Republic, to initiate a dialogue with companies, in particular to develop a joint plan of action to minimize the adverse effects on birds, maintain a dialogue with municipal authorities and local communities. A special task was to achieve reduction in the total number of licensed deposits.”

Vladimir Gulevich is the chief executive officer of ARM. A spokesman confirms that his company holds the Karakul licence. Gulevich took several days before reponding to questions himself. “I can confirm,” he said, “that we hold a license for development of the Karakul deposit, we won an auction in 2006”. He refused to say whether ARM has connections to Imperial Mining or to other structures, saying this is “confidential information”. Asked about shareholders, he said they are also confidential. He did confirm that Emil Malzhanov has been working with ARM and Imperial Mining. According to Gulevich, “currently, Emil Malzhanov is not working for us.” About what Malzhanov had done in the ARM project in the past, Gulevich said that is confidential. He refused to say anything more.

Evidence that the Oberoi family is a shareholder of Imperial Mining and ARM appears in a website listing for Emil Malzhanov. He describes himself as having been the chief financial officer of Imperial Mining between November 2006 and April 2010. Imperial Mining, he says, “is a large regional mining company that owns 6 large deposits in Russia and Mongolia. Among its mineral suit [sic] is high grade Cobalt, Copper, Silver and Gold. Shareholders of the company include European Bank for Reconstruction and Development, large mining institutional Investors and [the] Oberoi Family.” Malzhanov, who now works for a private metals holding in Astana, Kazakhstan, is uncontactable, as is the company for which he works.

P.R.S. Oberoi, the controlling member of the family in charge of the Oberoi and related EIH group of companies was asked to clarify the investment in Imperial Mining, and to say what he knows of the cobalt project in Russia. He replies: “We have never heard of Imperial Mining and have no shareholding or interest in the company. I, as Chairman of The Oberoi Group, was never involved with EBRD to secure any guarantees to Imperial Mining.”

A source at the Office of Foreign Investment Control, a branch of the Federal Antimonopoly Service (FAS) in Moscow, acknowledges that two statutes which Prime Minister Vladimir Putin signed into law in April of 2008, subject foreign owned or controlled companies to special restrictions in strategic sectors of Russian business; and define cobalt as a mineral of strategic value to Russia, whatever the size of the deposit where it has been found. These laws, FZ-57 and FZ-58, require an application by any foreign company seeking to own, or control, a cobalt mining venture to apply for government permission. This petition goes to the FAS in the first instance, where the papers are prepared for review by the Committee on Foreign Investment Control, which is chaired by Putin. The committee review is slow; eventual approval may be hedged with conditions, or not granted at all.

But according to the FAS, no petition has been filed by Imperial Mining or ARM for committee review and approval. That means that for the time being, it is legal for Imperial Mining and EBRD to own a company with a Russian cobalt mining licence, but no mining of cobalt is allowed until government authorization is granted.

Reviews of the legislation by well-known international law firms have been in wide circulation since the two laws came into force, and the effect of their provisions on foreign mining and other investment continues to be widely debated.

It cannot be likely, therefore, that EBRD’s lawyers and bankers do not know what their covert investment in the Karakul cobalt deposit would require, even if they were careless when the board of directors voted approval back in January of 2008. Even then it is improbable that the board and its Russian director, Kotova, didn’t know that cobalt was on the strategic list. Less than three months were to elapse before Putin signed the law into force, but the State Duma and Federation Council had been voting on drafts of the legislation well before the EBRD board acted.

Kotova happens to be working in Russia this week, and a spokesman relayed to her the question of what she knew, or knows, about Imperial Mining and the restrictions in Russian law on the cobalt project. She refused to reply.

After Williams had written to say EBRD won’t answer any question on the $30 million investment in Karakul cobalt, he was asked whether the lack of project, loan, or due diligence data for Karakul or Imperial Mining, published on the EBRD website, has any precedent for Russian project disclosure. Williams was also asked to explain why his refusal to respond to the questions asked should not be interpreted as a cover-up of wrongdoing at the EBRD. There has been no reply. Williams did answer a separate question on Kotova’s status, confirming that she “is the Director representing the Russian Federation on the EBRD’s Board of Directors…[and] sits on the Financial and Operations Policies Committee, currently as Vice Chair.”

A source at the Russian Ministry of Natural Resources in Moscow reveals there may be a catch in the cobalt mining rules. Cobalt mining is strategic, and subject to special permission by the Russian government, the source acknowledges. But if a licence holder like ARM and Imperial Mining, “started developing the field prior to the entry into force of the law [April 29, 2008], the permit is not required.” Since Soviet prospectors first discovered the Karakul deposit more than thirty years ago, what counts now is when exactly Imperial Mining and its local affiliate started development, and what counts as development under the Russian law.

According to the ministry, the cobalt mining venture may not be restricted, or subject to Kremlin permission, if the deposit was “let for use for the aim of geological studies, exploration and extraction carried out on a combined license, and for which the user has completed the subsurface geological studies, and begun in the prescribed manner exploration and extraction, before the coming into force of the present Federal Law.”

The EBRD board record appears to show that Imperial Mining had not completed its geological studies, nor started mining, in January of 2008. When the strategic legal restrictions came into force 111 days later, the situation was almost certainly the same. But the facts on the ground, the corporate records, and the ambiguities in the law remain unclear and unexplained. If the loophole disclosed by the mine authorities in Moscow provides one motive, then at least $30 million of EBRD cash makes an even bigger reason to keep this mine a secret.

Leave a Reply