By John Helmer, Moscow

Oleg Mukhamedshin, the man in charge of raising money and covering debt for United Company Rusal, was spotted last week in London carrying bags into his mansion. This is what has been happening to the aluminium he has been selling:

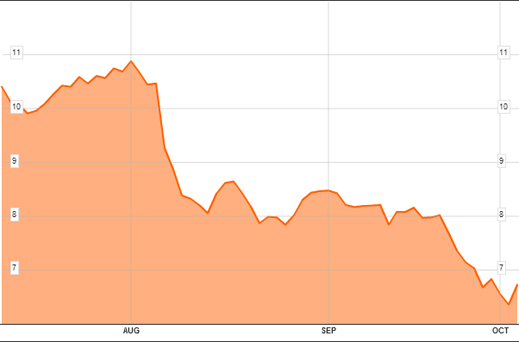

And to Rusal’s three-month share price:

In the past fortnight, the Finance Ministry and Central Bank have raised their estimate of net private capital outflow from Russia this year from $36 billion to over $50 billion. And in the same interval, $516 million of foreign portfolio investment in Russian equity and commodity funds were withdrawn. The good news – the rate of outflow, net private Russian and foreign funds under management, appears to be slowing down this quarter; but perhaps that is because the jittering class had emptied most of their wallets in the third quarter.

As for signs on the ground in Moscow of what there is to be jittery about, there was the assassination of Andrei Burlakov to silence what he was alleging in the press and in court about the conduct of high government officials in the diversion of state budget funds; that was on September 29.

Then this week there has been the outbreak of war between the Federal Security Service (FSB), the Ministry of Interior (MVD), and the General Prosecutor’s Office in the matter of MVD generals Ivan Glukhov and Andrei Khorev, and the arrest and investigation of Nelli Dmitrieva, senior investigator for very important cases of the Investigations Unit for Organized Criminal Activities Investigation of the Main Investigative Department (GSU) of the Main Department (GU) of the MVD of Russia in the city of Moscow. Uncorroborated reports claim that loyalty-tested Dzerzhinsky Division troops have been deployed to prevent the law enforcement officials from drawing guns on each other. For what is happening on the surface – extortion, bribery, frame-up — read this and this, and this too.

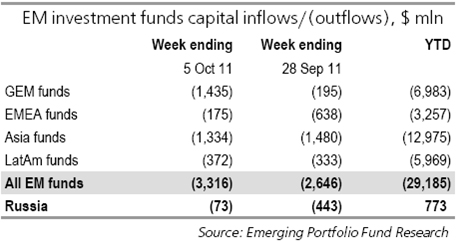

The sentiment among managers of funds invested in Russian equities and commodity-based exchange-traded funds (ETFs) is tracked by Emerging Portfolio Fund Research (EPFR), and as of this week, the picture looks decidedly negative:

For Uralsib Bank market strategist, Slava Smolyaninov, reporting to clients today, “we welcome the first signs of investors stopping targeting EMEA [Europe, the Middle East and Africa] in favor of other regions. While we believe it premature to expect a sustained reversal of flows and anticipate volatile data over the next few weeks, we are more optimistic about EMEA fund-flow performance relative to other regions, and see Russian equities as direct benefactors of the newly emerging trend. Hence, we continue to expect EMEA funds to fare better on a relative basis in 4Q11.”

The basis for this optimistic assessment is that during the past week of fund outflows from Russia, just $73 million worth of equity value was pulled out, compared to six times that amount, or $443 million, the week before.

Looked at by the week, the movement of the RTS share market index amplifies the hopeful assessment that the slowing haemorrhage will shortly be followed by transfusion:

Looked at for the year, however, the RTS started down when investor sentiment turned negative, the latter accelerating the downward trajectory of the former since the beginning of July:

Timing and acceleration for investors in Russian equities always reflect the movement in the price of the economy’s principal commodity, crude oil, and so they have this time around:

But the heightened state of the jitters has been noticed at the highest levels of government for more months than the market indicators have been going down.

The nervousness was brought on by the fight over the political succession between President Dmitry Medvedev and Prime Minister Vladimir Putin, and the men whose fortunes are tied to each. Apprehension by one faction of the possibility that the rival faction would pull what the Americans call an “October surprise” – the Soviets used to term this a “provocation” – may have persuaded Putin of the desirability of making the succession public before October commenced, weeks earlier than had been expected. But Prime Minister-in-waiting Alexei Kudrin upset this purpose by announcing that the war between the factions would intensify, not diminish.

Putin’s question-and-answer session at the VTB Capital conference on October 5 was also timed to undo the damage Kudrin had done. But was Putin speaking of the indebtedness of the oligarchs and state companies when he issued this apparent guarantee of Treasury cover against corporate default? “Unlike many other global economies, the state and corporate sectors in Russia are not burdened with excessive debt. The sovereign debt to GDP ratio in Russia does not exceed 10%, with foreign borrowings amounting to less than 3%. I would like to say in this respect that yesterday we adopted a decision on additional incomes. We will not borrow on foreign or domestic markets and will therefore save approximately 350 billion roubles. We have decided not to borrow the planned sums on the domestic market, leaving the money at businesses’ disposal. Our companies have almost no risky short-term debts.”

The Fitch ratings report on the debt and default risk of state flagship company, tanker fleet operator Sovcomflot, managed by Sergei Frank and Sergei Naryshkin, the Kremlin chief of staff, may provide a measure of market credulity towards Putin’s point. Due for release early this week, Fitch is delaying without explanation.

A problem identified in this week’s flow-of-funds report by EPFR is that conventional equity funds, invested mostly in the Russian blue-chip sectors (oil, gas, metals), accounted for almost two-thirds of the outflow in recent days. The remainder — funds invested in those exchange-traded funds whose commodity focus links them to Russian producers and exporters — are motivated by commodity price movements globally, much less by Russian events. For most of the recent period of decline in flow of funds between and out of the emerging markets, ETF movements have been the biggest factor.

The best that Uralsib can find to say about this trend is that most other emerging market country equities are performing just as badly, or worse, than Russian. According to Smolyaninov, “the reported week was understandably poor on the country level, with the overwhelming majority of country funds losing money. Small inflows were seen only in a few places, with Mexico, South Africa, and Israel taking marginal inflows, while recent favorites such as South Korea, Thailand, and Chile funds lost in excess of 2% of AuM [assets under management].”

“Data for the week indicate that outflows from EMEA as a region have finally started to abate. The total for the region stood at $175 mln, or 0.51% of funds’ AuM. Withdrawals from Asia, excluding Japan, intensified, with the region losing $1,334 mln, or 0.68% of AuM, while LatAm funds saw outflows of $372 mln, or 0.91% of AuM. It was the 22nd consecutive week of outflows from EMEA regional funds. Investors have taken $7.6 bln from the funds over this period, which corresponds to 16.4% of AuM.”

| But there is reassuring news that the pair of safe hands which lost control of themselves a week ago, those of Finance Minister Kudrin, are themselves in bigger, safer hands, even if Kudrin has suffered the reproof of being diagnosed by the prime minister with a near-psychiatric condition. |  |

Speaking at the VTB Capital conference in Moscow yesterday, Putin said: “As for Alexei Kudrin, I must say that he is definitely one of the best specialists, not only in Russia but in the world as well. This is first. Second, he is our very personal and my good friend, with whom I have maintained a very close, intimate relationship for many years, beginning in the 1990s. As we know, this decision [to fire Kudrin] was taken by the President. [It was] taken on the basis of the fact that Alexei Leonidovich made some incorrect statements about the fact that his position does not coincide with the position of the President. What can I say here now? You want me to comment on this? I think that even comments on my part at this point would be incorrect. We spoke with Alexei Kudrin on this score. I want to tell you that – this is my opinion, and that of President Medvedev – despite this emotional breakdown, Aleksey Leonidovich is still a member of our team and we’ll work with him. I hope that he will work with us. He is useful and necessary to our people.”

Leave a Reply