By John Helmer, Moscow

If Vnesheconombank (VEB), the state bailout bank chaired by Prime Minister Vladimir Putin, really has agreed to pay $5.3 billion for the 80% control shareholding of Raspadskaya, the coking coalminer, then this is going to be Roman Abramovich’s lucky day. His second lucky day, if to count the September 2005 transaction when state-owned Gazprom paid $13 billion for Abramovich’s 72.6% stake in the oil company Sibneft. Well, it’s everyone’s lucky day, because Abramovich is known to be a sharing kind of man. With almost everyone.

The decision of the VEB board to authorize negotiations for the sale and purchase of Raspadskaya has not been acknowledged before. Nor has a source been identified for the Interfax report, amplified today by a newspaper in Moscow and other news wires, that the bank board has approved a valuation of Raspadskaya at $6.6 billion. A board meeting is scheduled for today, so the press leak appears to have been timed ahead of the tabling of the deal for a board vote.

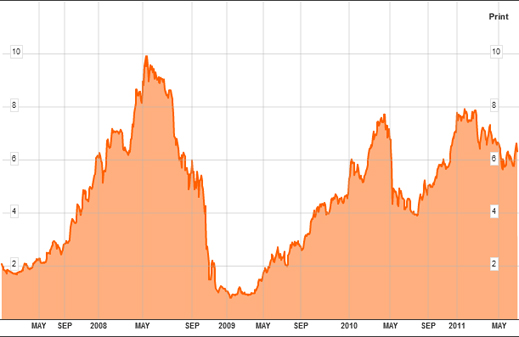

The price is 29% more than its current market capitalization on the Moscow exchange, with a share price equivalent of $8.49. In its entire history, the Siberian based mining company has enjoyed a share price at that level for just twelve weeks in mid-2008, when coking coal prices reached their boom peak, before that year’s commodity price crash; that was followed by the mine’s May 2010 explosion and shut-down.

Raspadskaya’s 4-year Share-Price History

As a state entity operating with public funds, VEB was asked to say if it has been negotiating to buy Raspadskaya, and if it has been studying the asset value of the company. VEB spokesman Yekaterina Karasina refused to say. So the spokesman was asked to confirm something which is public knowledge – how much money did VEB lend the Evraz steel group, controlled by Abramovich and his partners Eugene Shvidler and Alexander Abramov, when the group was on the verge of bankruptcy and default in November of 2008, with $9 billion in debts. VEB refuses to answer.

(Evraz has disclosed in its financial reports that the VEB loans amounted to $4 billion as of December 2008. But asked today to say how much of the VEB money has been repaid, how much is still owed, Evraz won’t say.)

Other Russian press reports, also with anonymous sources, have claimed that a sale of the control shareholding of Raspadskaya is in the works to the only source of cash apparently willing to pay a premium – the Russian state. These reports claim the transaction is valued between $7.80 and $8.20 per share. That’s a wee bit below the VEB offer – if there’s a genuine offer there. If you were Abramovich, with his 40% of the mining company, or Gennady Kosovoy and Alexander Vagin, the original mine managers with the other 40%, wouldn’t you be issuing anonymous press reports to jack up the price?

A source close to the Raspadskaya board of directors speculates that the entire scheme by Kosovoy and Vagin to add their 40% to the sale proposal for Abramovich’s 40% was designed from the start to make the cost of taking over the company too expensive for anyone to attempt. In short, Kosovoy and Vagin have been plotting to stop the sale altogether.

But that calculation appears to have come to them only after they had talked to the state banks in Moscow, as well as Deputy Prime Minister Igor Sechin, to see if they would be approved and given the money to buy out Abramovich. In the murk surrounding these negotiations, one thing is clear – Sechin and VEB aren’t willing to back Kosovoy and Vagin.

So who is behind the latest jackpot announcement? Abramovich hoping for a lucky bonanza at a higher price than the market or the state banks will allow? Kosovoy and Vagin? Then again it may be one of the Russian steel oligarchs who have told Sechin they would take the asset off Abramovich’s hands for a price of $2 billion to $3 billion – half today’s lucky number. For them, public disclosure of the $5.3 billion takeover price may be calculated to trigger enough shock that VEB will drop the hot potato.

Uralsib Bank admits it doesn’t know what is happening, but thinks it is worth wagering on a rise in price for Evraz, if not for Raspadskaya. “The deal may be approved at VEB’s supervisory board meeting, which will be held today. We believe that the sale of Raspadskaya to VEB is very positive for Evraz, while the prospects for Raspadskaya’s minorities are unclear at this stage. Yesterday, both stocks reacted positively to the news: Raspadskaya gained 3% on MICEX and Evraz gained 1% in London.”

“As we understand, Evraz and Raspadskaya’s management failed to find a buyer in the market for the mine and decided to sell the asset to VEB, which surprisingly agreed to pay a huge premium. We expect that going forward Raspadskaya will be sold on to other market players, including NLMK [Vladimir Lisin], Severstal [Alexei Mordashov] or Mechel [Igor Zyuzin]; however, it is unlikely that any of these companies are ready to pay $5 bln for a damaged asset. At this stage, the sale of Raspadskaya to VEB raises more questions than answers for us.”

Speculation of quasi-nationalization of Raspadskaya, even a temporary one, sends cold shivers through the investment markets, where it is understood that even if Abramovich shares his good fortune from the buyout, the non-Russian minority shareholders won’t be on the receiving end. According to Uralsib’s report, therefore, Raspadskaya’s share price should start falling.

And that’s exactly what Igor Zyuzin, proprietor of Mechel Mining, the next Russian coal group to try to sell shares in an initial public offering (IPO), may be hoping for – depress the price at which he can take the asset out of VEB’s warehouse; arrange VEB financing for the difference between its purchase and resale price; and then share with VEB the proceeds of the premium to be earned when the Raspadskaya-enhanced Mechel Mining shares are sold.

According to Uralsib analyst Dmitry Smolin: “The prospects of Raspadskaya’s minorities are unclear at this stage, as we do not expect any buy-back offer for minorities at a premium from VEB (VEB could acquire Corber, an offshore company, which owns 80% in RASP). We recommend using the current rally in the stock to exit the name.” Renaissance Capital also advised the markets to capitalize on their ignorance, and sell: “We recommend selling Raspadskaya into strength as a tactical play, due to the lack of transparency around the deal and the market’s overreaction to a new wave of speculation.”

The assessment from Mikhail Fridman’s Alfa Bank sees money-making opportunities in everything but holding on to Raspadskaya shares for longer than this afternoon, when the VEB board decision may be announced. For Abramovich’s Evraz, however, the future looks much brighter. Barry Ehrlich, Alfa’s steel analyst, reports: “If the deal is not just another round of speculation, the news would be POSITIVE for Raspadskaya shares mainly through the sentiment drawn from the generous premium offered. On the other hand, if VEB is the buyer, there will be: 1) still no clarity on who will be the final buyer and what will be the destiny of the asset; 2) government ownership of Raspadskaya and control of its operations; and 3) the deal will likely be structured in a way that will not offer a buyback for minorities.”

“For Evraz, the potential deal is also POSITIVE, as it will help to cut its FY11 year-end net debt to ~$3.5bn, resulting in a net debt/EBITDA ratio of close to 1x and making the company’s balance sheet capable of financing CAPEX extensive projects like Mezhegey or Timir. The deal will also bring an additional ~$660m to Evraz’s valuation on the market premium it would get from this deal.”

Leave a Reply