By John Helmer, Moscow

Eurochem, a Russian fertilizer miner and manufacturer owned by Andrei Melnichenko, is suing the South African mine technology company Shaft Sinkers for $800 million on account of a mining technology which Eurochem says has failed in Volgograd (image right). Shaft Sinkers says the technology works perfectly well, in Yorkshire (left) for example. $800 million is the sum of Eurochem’s claims. Much less than that is at stake — according to Shaft Sinkers $15 million in unpaid invoices – but also much more, in Kazakhstan, where Eurochem’s plan for a large new phosphate mine is in trouble of another sort. About that Eurochem doesn’t want to talk at all.

In 2008 Eurochem made several announcements about its new potash mine, Gremyachinskoye mine in Volgograd. In the context of Melnichenko’s proposal to reduce his personal exposure in the company, and sell assets to Gazprom or shares to international investors, Eurochem reported growing reserves, speed in mining new output, and jumping sales revenues. Gremyachinskoye was to be commissioned in two stages, start shipping 2.3 million tonnes of potash per annum in 2012, and by 2015 double that volume.

EuroChem chief executive Dmitry Strezhnev said at the time that total investment for the project came to $2.2 billion; that included $100 million for the mine license; $50 million for preparatory works; $600 million for the processing plant; $300 million for infrastructure to support the mine; and more than $600 million for the two principal shaft builders, Thyssen Schachtbau (Germany) and Shaft Sinkers (South Africa).

“When we studied the profitability of this project,” Strezhnev said, “it was profitable even at a potash price of $500. We do not expect prices to go lower than $700-$800, so our investments carry almost no financial risks.” Nikolay Pilipenko, Eurochem’s financial director, added: “We were ready for an IPO already last year. The Eurobond [$300 million, issued March 2007] was a very good disclosure exercise that we’ve now passed. If [the IPO] will be decided by the management we can prepare very quickly.”

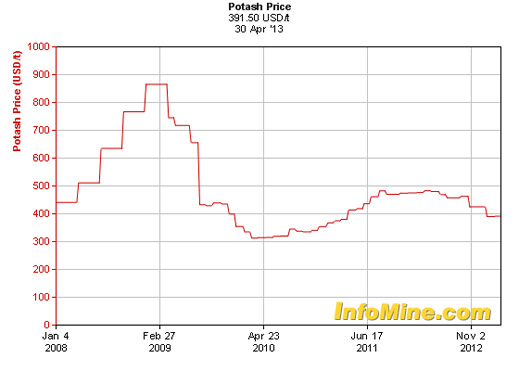

Potash hasn’t been the winning bet Melnichenko (92% of Eurochem’s shares) and Strezhnev (8%) were counting on. The commodity price peaked at $900 per tonne; collapsed to $300; and is currently at $391.50. During the five years in which Shaft Sinkers has been excavating at Gremyachinskoye potash has failed to reach Eurochem’s breakeven point.

In 2008, when Shaft Sinkers confirmed its $270 million contract, Rob Shroder, then chief executive of Shaft Sinkers, described the technology intended for Gremyachinskoye as only the second such application to a potash mine in the world; the other was at Boulby in the UK. “Älthough this is our first venture into Russia, we have sunk shafts throughout the world with the exception of North America. We specifically bring our grouting techniques, used successfully in the majority of these other projects, and are certain this will bring significant time and cost savings for this Project.”

According to Shroder, “Instead of freezing, where one drills holes 500 metres deep, freezes the ground to this depth, and then sinks the main shaft through frozen ground, we cover-drill up to 42 metres ahead of ourselves. If we intersect water or running sands, we pump cement or resin grouts into the material, until it solidifies. then we drill and blast through.” This is a Canadian description of the grouting technology for holding back water and preventing cave-in – common hazards in potash mining the world over.

Eurochem thought it was hedging against the potash price by investing in Shaft Sinkers grouting technology as a cheaper, faster way of getting saleable potash from underground and into the market – 25% cheaper, according to Alexander Tugolukov, the technical director at Eurochem. The German and South African contractors had been chosen, he said in 2008, “with a kind of socialist emulation between them to determine who will do the job better, quicker and cheaper. These tactics may also be used on our Verkhnekamskoye deposit [potash, in the Urals] to cut the timing of mine development and construction from the conservative 7-8 years to about 5-6 years.”

Vladimir Torin, Eurochem’s spokesman, added: “We searched the global market for a company specializing in what we needed, and found Shaft Sinkers by ourselves. We then negotiated directly, sending Alexander Tugolukov, our technical director, to South Africa to study their previous and pending projects. They are the largest shaft constructors in the world, so the choice was obvious.”

For the next four years what seemed obvious was that everything was going swimmingly. The Eurochem contract – Shaft Sinkers’s biggest, representing about 30% of its order book – enabled Shaft Sinkers to move from private ownership shared between Shroder and black empowerment enterprise partners to an IPO on the London stock market in December 2010. By then the control shareholder was International Mineral Resources (IMR), an affiliate of ENRC, the Kazakh mining conglomerate, which had bought out most of the South Africans.

In June 2011 Eurochem reported that Shaft Sinkers’ work was going according to plan, and was “on track to allow potash production to start by late 2013. Shaft Sinkers acknowledged there was a problem well before Eurochem did, but the former was a public company operating under London market rules. On December 29, 2011, Shaft Sinkers said that “due to the continued slow progress resulting from extremely difficult ground conditions previously announced, it has entered into discussions with its client EuroChem with a view to amend or terminate the contract. Sinking works have now been suspended and the parties are in negotiation on the way forward.”

On June 1, 2012, Shaft Sinkers reported the problem had become bad news: “discussions are continuing with EuroChem on the settlement of outstanding amounts… The Group continues to pursue new projects and is awaiting client adjudication on several tenders and proposals in South Africa, The DRC, Russia, and Kazakhstan. Results from trading for the 2012 financial year are forecast to be in line with expectations and the Board remains confident of the Group’s prospects.” On August 30, 2012, it was clear the Russian mine project had stopped: “The full demobilisation of our EuroChem project is expected to be completed during the second half of 2012. Discussions continue with EuroChem to recover the amounts owing to the company.”

In fact, as much later announcements from Eurochem revealed, Eurochem told Shaft Sinkers it was terminating their contract at Gremyachinskoye on April 20, 2012. Why Eurochem pretended nothing was happening isn’t clear.

Here is Eurochem’s first- quarter IFRS financial report, issued on May 22, 2012, one month after the contract ended: “We continued making good progress on our two potash developments in the first quarter of the year. In southern Russia, shaft sinking operations at VolgaKaliy’s skip shaft #1 hit the 500 meter mark late in the first quarter. As at 18 May, the shaft had reached its approximate midway point of 550 meters. The future mine’s cage shaft continued being readied for freezing with sinking operations set to resume within the next twelve months.” Note that the skip shaft was the German project; the cage shaft was Shaft Sinkers’. Eurochem was intentionally misleading in this claim.

Eurochem’s first public disclosure of the dispute was this announcement of October 5, 2012. The wording is important because of the claim that the dispute was a contractual one based on the technical claim about the grouting technology: “Shaft Sinkers was chosen as the contractor to develop the cage shaft of the Gremyachinskoe deposit but subsequently proved unable to fulfill its contractual obligations. Shaft Sinkers’ grouting technology entirely failed, causing in excess of USD 161 million in direct costs and a delay to the project’s completion date which was subsequently revised to 2015.”

This announcement is also noteworthy because of Eurochem’s calculation of the liability. It took several more months before it was disclosed publicly that Eurochem was raising the amount of its claim to $800 million to include purported lost profits because of the production delay. This amount appears in a Shaftsinkers report on February 13, this year. Russian courts don’t accept this type of damage claim. Whether it will be allowed by the two arbitration tribunals in Zurich and Paris, to which Eurochem has applied, remains to be seen, not least of all because Eurochem claims lost profits when the price of potash is still below the cost of mining and selling it.

In Eurochem’s reporting of the dispute with Shaft Sinkers, the details are to be found in the auditor’s notes to the financial reports for 2012. In its audited accounts Eurochem also fails to provision for Shaft Sinkers’ counterclaim ($54 million in press reports, $15 million in Shaft Sinkers’ reports). According to Eurochem’s auditor, “Write-off of a portion of the assets at the Gremyachinskoe potash deposit. Following an earlier termination of the construction contract, in October 2012 the Group filed a claim against Shaft Sinkers (Pty) Ltd. (Shaft Sinkers), seeking US$ 800 million compensation for the direct costs and substantial lost profits arising from the delay in commencing potash production. This was a result of the inability of Shaft Sinkers to fulfill its contractual obligations and complete the construction of the Gremyachinskoe cage shaft, primarily due to problems with the grouting technology. In October 2012 Shaft Sinkers presented an interim claim letter to the Group claiming compensation of US$45 million in costs incurred by them up to and inclusive of 30 September 2012 in connection with the termination of the construction contract. Management believes that this claim is without merit. The above disputes are subject to arbitration as specified in the contract. An outstanding advance given to Shaft Sinkers of RR 495,387 thousand was written off during the nine months ended 30 September 2012 (nine months ended 30 September 2011: nil). Due to the failure of the grouting technology employed in the cage shaft construction, expenses previously capitalised, amounting to RR 3,116,000 thousand, were written-off during the nine months ended 30 September 2012 (nine months ended 30 September 2011: nil).

Following Eurochem’s submission of its claims to arbitration in October, Shaft Sinkers issued this notice to the London Stock Exchange: “On 5 October 2012 the Company responded to the announcement by EuroChem that it had filed a claim against Shaft Sinkers (Pty) Ltd in relation to its project with EuroChem which was terminated with effect from 20 April 2012. The Company has reviewed the arbitration claims, and after consultation with legal counsel, continues to believe that the claims are without merit, and will contest them robustly. A claim for a net amount of $15 million has been submitted to EuroChem for amounts still owing under the contract.”

A spokesman for Shaft Sinkers was asked this week to clarify what happened, and also why the dispute escalated from a problem of mine delay to an $800 million claim. He responded: “Shaft Sinkers has built many shafts worldwide and we were involved in the construction of the other deep potash mine in Boulby in the UK. Shaft Sinkers was called in after other companies failed and we successfully completed building the mine. We believe that the [Boulby] mine continues to operate normally.”

“The technology is not experimental, having been used successfully in many mines around the world and it did not fail in this case. However deep shafts are clearly complex engineering projects where delays can happen due to a wide range of factors. In the case of Eurochem, the ground conditions were difficult and Shaft Sinkers were in the process of refining the specific application necessary for the shaft when Eurochem suspended the project. Whilst the exact details of the contract are covered by commercial confidentiality and are subject to legal restrictions, I can say that as Shaft Sinkers has – so far – not failed in its mining efforts, provision for failure was from Shaft Sinkers’ point of view unnecessary.”

Is there another reason why Melnichenko has stopped one of the mine shafts, and ordered his lawyers to pursue Shaft Sinkers on the technical claim?

Since the potash price is well below where the miners would like it to be, mining less potash is one way of putting a bottom under the price. Eurochem’s Russian potash rival Uralkali implemented a production cut in 2012 of 8%. In the first quarter of this year, Uralkali said it is cutting by another 40%. The Russian cuts match those of Canada’s Potash Corporation, the largest producer in the worl, which has taken 1 million tonnes off the market since last year. For Eurochem to hurry a fresh 2.3 million tonnes from Gremyachinskoye on to the market would be folly, as the price it would fetch would probably be lossmaking. Mining the law courts may look a better bet to Melnichenko, especially if he must pay his lawyers less than the $15 million in overdue invoices from Shaft Sinkers for the work done but not paid for when the contract was halted.

Is there any other reason for the attack on Shaft Sinkers and its Kazakh control shareholder?

The answer to that one may lie in problems which Eurochem is having in Kazakhstan, but which the company is reluctant to acknowledge.

Asked what problems in Kazakhstan Melnichenko and Eurochem have across the border, Eurochem sources initially claimed there weren’t any. Kazakhstan holds substantial reserves of mineable fertilizers, particular phosphates. These are concentrated in the southern regions of the country, between the cities of Shymkent and Taraz.

At Taraz the leading miner is Kazphosphate, which is incorporated in the UK. That entity has had what is known in the market as a controversial history since it was first taken over by two controversial Israelis, Nahum Galmor and Arkady Gaydamak. After fighting between themselves the property passed into local control and into the hands of three Kazakhs — Nurlan Bizakov, Galimzhan and Maxutbek Yessenoz.

According to Eurochem’s financial report for 2012, issued on February 7, 2013, Melnichenko has two projects in Kazakhstan – one at Karatau, where Kazphosphate is already mining; and one at the Kok-Jon and Gimmelfarbskoe deposits, which have been partially explored but not yet mined. According to Eurochem’s papers, “to increase upstream integration, we plan to start phosphate rock mining in Kazakhstan’s Karatau Basin from 2013”; and “we are looking to increase our vertical integration by extracting phosphate rock from the Kok-Jon and Gimelfarbskoe deposits in Kazakhstan’s Zhambyl province”.

The releases from Eurochem include the announcement in February 2009 of Kazakh presidential approval for the Karatau project, with capital spending of $2.5 billion; production targets of 1 million tonnes of phosphates, 800,000 tonnes of nitrogenous fertilizers; a nitrogen, phosphate and potash combination (NPK) plant, and more, all by the year 2015. This was repeated for the benefit of Russian and Kazakh ministers in June 2009. Subsequent company publications claim that right now “we are developing the phosphate deposits and constructing a fertilizer plant in two locations, Zhanatas and Karatau.”

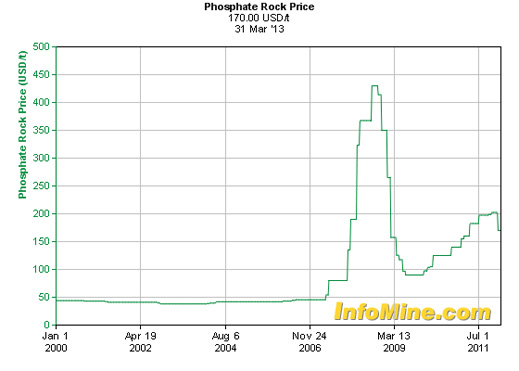

It would be madness for Melnichenko to be spending $2.5 billion on adding to phosphate supply when it is suffering from the same downturn in market demand and price as potash:

Melnichenko isn’t mad. But the Kazakhs are impatient. They think there is a four year-old promise to start the mine with targeted production tonnage and estimated revenue and cashflows. So how much has Eurochem actually spent at Karatau since 2009, and is there a problem between the company and the Kazakh mine licensing authorities?

A spokesman for Eurochem replies: “In terms of its activity in Kazakhstan, EuroChem is working through the various regulatory and legal requirements necessary to ensure that its operations conform with Kazakh legislation. Investment has been made into social projects there, with USD 5 million already committed. Further than that, I’m afraid we cannot comment.”

That doesn’t sound like the thunder of digging machines at Karatau. But promising to start excavation in 2009 and not starting, Eurochem has paid real money for additional phosphate reserves elsewhere. Eurochem’s financial report for last year notes payment of Rb1.1 billion ($35.8 million) for the mineral and mining rights at Kok-Jon and Gimmelfarbskoye. “During the year ended 31 December 2012 the Group signed a contract with the authorities of the Republic of Kazakhstan for the extraction of phosphate rock at the Kok-Jon and Gimmelfarbskoe deposits in Kazakhstan’s Zhambyl region. The Group plans to launch a mining and production project, which includes the development of phosphate rock deposits, the construction of integrated mining-and-processing facilities and a fertiliser production plant. Under the terms of valid licences for the exploration and development of mineral resource deposits, the Group is required to comply with a number of conditions, including preparation of design documentation, commencement of the construction of mining facilities and commencement of the extraction of mineral resources by certain dates. If the Group fails to materially comply with the terms of the licence agreements there are circumstances whereby the licences can be revoked. The management of the Group believes that the Group faces no material regulatory risks in relation to the validity and operation of any of its licences.”

There is domestic rivalry for Eurochem from several sources, according to those familiar with the matter, and this is too sensitive for Eurochem to acknowledge, particularly as it doesn’t have to do so for public shareholders. The phosphate prospects are also not so attractive that Kazphosphate was able to sell its shares in a London IPO it was contemplating in 2009. Nor was Melnichenko willing to buy a 50% stake in Kazphosphate the year before, at least not at the reported asking price of $400 million.

So can the Kazakh and Russian phosphate combines go it alone, each publicly promising billion-dollar investments in new mines? That depends on a great many things, not least the willingness of Kazakh government ministries and state-controlled suppliers of raw materials, gas and electricity to cooperate at a price that allows the mines to make their target rates of return. Right now, if you follow the phosphate price trajectory, the risks recommend doing nothing on the ground.

Leave a Reply