By John Helmer, Moscow

BC Iron is a small but promising iron-ore miner from Western Australia, which is China’s mineral supply province and rival of Russian suppliers to China. The company is now testing the share price at which it was the target of an abortive takeover attempt a year ago. The bidder at that time, Regent Pacific, a Hong Kong-listed promoter of a junior mining stocks, is part-owned and part-chaired by Stephen Dattels, an impresario of stock market wagers. On the latest available financial reports, Regent Pacific is losing money at the mining game.

Regent Pacific is also the operator of a fixed-odds financial betting scheme which, according to the company website, is “the market leader in its [wagering] industry.” Gambling can be profitable; it seems Regent Markets Holdings Ltd, the betting affiliated unit of the group, is turning over far more money than the mining holding, and at last report generated a 6-month profit of US$1.07 million, compared with US$1.8 million loss for the mining business.

Betting on sure things is good business if you are a professional gambler; it isn’t viewed the same way in the mining markets.

In the year that has now elapsed since the BC Iron takeover, Dattels and his transaction record have come under investigation by the Australian market regulator, the Australian Securities and Investments Commission (ASIC). In parallel, he and a junior uranium prospector called Uramin he sold very profitably in 2007, have been under investigation in France. Much too profitably think the French. The Canadian police have also been invited to investigate.

The tell-tale details of an abortive junior diamond miner in Russia, from which Dattels made his profit before the company collapsed into worthlessness, may also be worth re-examining to see whether there is a common modus operandi here.

Dattels has been reported by a Canadian associate to have a London residence. He is also reported to have a Palm Beach, Florida, house, a picture of which has proved to be easier to find than a picture of Dattels himself. Canadian sources report that no press picture is available of him in that country; he himself won’t say why.

Dattels has been reported by a Canadian associate to have a London residence. He is also reported to have a Palm Beach, Florida, house, a picture of which has proved to be easier to find than a picture of Dattels himself. Canadian sources report that no press picture is available of him in that country; he himself won’t say why.

Western Australia is one of the world’s largest iron-ore provinces. But it is under increasing cost, tax and political pressure, compared with Russia’s iron-ore mines in the Kursk Magnetic Anomaly; the West African iron-ore fields, and Brazil. Russian steelmakers who don’t have enough iron-ore to feed their smelters like Magnitogorsk Metallurgical Combine (MMK), have invested in Western Australian mines (Fortescue, Flinders Mines) as a hedge against the rising price of iron-ore; and because the outlays are less, and the payback swifter, than investing in new iron-ore mines in Russia.

The Ukrainian metals magnate Gennady Bogolyubov has also invested in Western Australia to extract and trade several of the steelmaking alloy minerals – manganese, chromite, and iron-ore – to supply China, and also Ukraine-based steelmills. Bogolyubov’s investments in Consolidated Minerals (100%), BC Iron (24%), and the Mindy Mindy iron-ore development (50%) – make him currently one of the largest foreign investors in Australia; the largest of the non-Chinese investors.

The story of Regent Pacific’s A$3.30-per-share bid for BC Iron was first told in February of 2011. Bogolyubov’s opposition to the deal doomed it. He believed the takeover price was too low.

Before he knew what was happening, though, between the time the deal was done between representatives of Regent Pacific and BC Iron, and then officially announced; and then again in the days before the deal collapsed in March-April 2011, there was unusual stock market activity and share price movements on which someone made handy money. The tale of how the deal unravelled can be re-read here.

BC IRON 3-YEAR SHARE PRICE TRAJECTORY

As reported then, the Takeovers Panel, a government body run by the Treasury in Canberra, investigated the takeover bidding, and sanctioned Regent Pacific by requiring it to resubmit its offer and terms. By the time that process had been completed, and BC Iron withdrew its earlier acceptance, Regent Pacific was obliged to cough up US5.5 million in transaction termination penalties; that was the single largest revenue item in Regent Pacific’s consolidated income balance-sheet for the first half of 2011. It wiped out all other sources of mining or investment income for the period.

The second of the Australian regulators to open a dossier on the Regent Pacific-BC Iron takeover attempt and the share price evidence is ASIC. Its investigation appears to have commenced between February and April of 2011. At the time, it refused to comment on the case.

Now, after almost a year, the Commission has issued a partial summary of what it had investigated on March 8, 2012. It claims it has uncovered disclosure violations by BC Iron which had impacted the share price during the takeover negotiations. According to the ASIC release, BC Iron paid a $66,000 penalty which accompanied the infringement notice. ASIC also claims this was “a timely and efficient remedy for dealing with some breaches of the continuous disclosure laws and effective in maintaining confidence in the integrity of our market.”

According to a release from BC Iron (BCI) the week before, on March 1, it was as white as the driven snow, and that at least one newspaper which had intimated otherwise was “manifestly incorrect”. BCI had, the company declared, engaged an anonymous lawyer “to opine on the merits of ASIC’s notice”, who had advised that the ASIC infringement ruling was “fatally flawed.” BCI said it was paying the penalty under protest, and because it was cheaper to do that than to pay fees for lawyers to “opine”.

At the same time as BCI was going down, the share price was going up.

According to Australian Stock Exchange (ASX) mandatory disclosures, the Chinese off-taker for BCI’s iron-ore shipments, Henghou Industries (Hong Kong) Ltd., has been converting earlier BCI share options into voting shares this year; by early this month Henghou has built up a bloc of almost 10%. Henghou had been identified by BCI as arranging the purchase of 20 million tonnes of iron-ore for Chinese steelmills between 2010 and 2018. Henghou, on behalf of the mills, fronted up US$50 million in three instalments to help BCI open its mine and start shipments to China.

BCI revealed in November 2010 that as part of the loan and offtake deal, it was issuing 8 million share options to Henghou. In a presentation to the market that month, BCI also revealed it had committed 65% of its mine output in 2011 and 80% in 2012 to Henghou at an “agreed [undisclosed] discount”. Starting in 2013, Henghou’s discount covers 50% of the shipments, while the remainder goes out at spot market prices.

In January 2011, a few weeks after the share options were confirmed, Henghou may have been as surprised as Bogolyubov to find that the executives and board it had signed with at BCI had been busy doing a deal with Regent Pacific to sell out. The Ukrainian went public; what the Chinese told BCI isn’t known. The upshot is that after the Australian regulator has found fault with BCI’s conduct, Henghou has decided to reinforce its interests and strengthen its shareholding position in BCI.

But it isn’t the only one buying BCI shares. Over three weeks from February 15, Regent Pacific paid almost A$3.1 million to add another 1.2 million shares to its stake in BCI. Its shareholding now totals 21.9%.

Last week, Bogolyubov’s Consolidated Minerals (Consmin) reported to the ASX that it has been buying BCI shares too. It has spent more than A$3.2 million to lift its stake in BCI by 1.2 million shares to almost 29%. Combining the Henghou, Regent Pacific and Consmin stakes, 61% of BCI is now under the control of just three shareholders. The stakes in the company held by board chairman Tony Kiernan, managing director Mike Young and other directors or related parties was reported on March 21 in a company presentation as 2.6%. That means that someone on the board has been selling, since the annual report of BC for the last financial year claims the directors held 3.4% as of last June.

So if the Chinese were playing catch-up and prevent BCI getting away from them, why has the loss-making Regent Pacific been spending its scarce cash on BCI? Is it planning another strategic move on BCI, and if so, who is paying for it?

At Regent Pacific Dattels shares control of the company with co-chairman James Mellon; as of November 1, 2011, Dattels is reported to have been holding 8.16% of the shares; Mellon 14.74%. Dattels, a Canadian national with a reported residence in London, has declined the invitation to respond to questions about his role in Regent Pacific at the time of the BCI takeover attempt or since.

Dattels is known to Russia’s former mining regulator Oleg Mitvol for the role he and a Russian partner, Sergei Kurzin, played in promoting Everfor Diamonds, which listed on the Alternative Investment Market (AIM) of the London Stock Exchange between 2005 and 2008. In 2004 Dattels and Kurzin arranged Russian diamond exploration licences that were controversial at their issue, and proved to be fruitless three years later. Pages 78-80 of the AIM Admission Document for Everfor relating to the issuance of these licences, the government officials responsible, the chain of Caribbean companies through which the licences passed into Everfor, and the fees paid to Dattels and others have been of special interest. Later Mitvol claimed he suspected a share price pump and dump scheme, but took no action before he himself was ousted from the Ministry of Natural Resources.

Everfor’s listing produced an initial market capitalization of ₤140 million. By the time it changed its name and went into liquidation, Dattels was long gone. He doesn’t mention the experience in his Regent Pacific biography.

Kurzin (right), Dattels’ partner in that venture, has also been reticent about the Everfor story, though he told a Forbes interviewer he was “feeling good” about it at the time. The Forbes report attempted to identify sensitive patterns in the way mining licences were obtained, companies floated, and windfall profits generated from “complicated deals involving offshore trusts and opaque Russian- and Kazakh-registered entities.”

Kurzin (right), Dattels’ partner in that venture, has also been reticent about the Everfor story, though he told a Forbes interviewer he was “feeling good” about it at the time. The Forbes report attempted to identify sensitive patterns in the way mining licences were obtained, companies floated, and windfall profits generated from “complicated deals involving offshore trusts and opaque Russian- and Kazakh-registered entities.”

Dattels’ name and business conduct have been the target of more recent investigation after the French uranium giant Areva announced that it was writing down the purported asset value of uranium prospects Dattels had sold Areva in 2007. Dattels had sold Uramin, a junior miner listed in Canada, for US$2.5 billion. Here’s the way the deal looked when it was officially disclosed in June of that year. Last December Areva declared a loss of US$2 billion on the asset value.

English-language reporting of Dattels’s mining investment operations has been modest by contrast with the French coverage of this year’s investigations of the difference between Uramin’s selling price and what Areva now considers it is worth. According to an investigative report by by Andre Noel and Fabrice de Pierrebourg of La Presse, published in Montreal on February 11, Dattels began selling Uramin to Areva in October of 2005, just weeks after Dattels had formed the company with his partners. After Dattels was identified in the investigation by La Presse, the Senator for Bedford, Quebec, Céline Hervieux-Payette, charged in Senate proceedings that “there is reason to believe that UraMin might have engaged in insider trading and other fraudulent activity.” She asked the leader for the Canadian Government in the Senate to order the Royal Canadian Mounted Police “financial crime division [to] start an investigation immediately into UraMin’s dealing with Areva and clean up Canada’s reputation”.

Alleging that Uramin may have been joined in misrepresentation of its asset and transaction value to Areva, the senator added that “the Bank of Montreal acted as a financial advisor to UraMin in its transaction with Areva. Considering that the implication of a Canadian bank in this scandal, which is common knowledge in France, has the potential to harm Canada’s international reputation, can you guarantee to this chamber that the Office of the Superintendent of Financial Institutions will look into the role and actions of the Bank of Montreal in this affair?

Regent Pacific is not commenting on the outcome of the Australian regulator’s investigation of BCI share trading and disclosure of the takeover scheme. Nor will it discuss Dattels’s role in deciding Regent Pacific’s buy and sell strategy. Dattels refuses to respond to enquiries.

The company’s website is currently reporting that BCI is one of 12 mining company holdings in the Regent Pacific portfolio. Of this dozen, BCI is the only one in current production, and is almost certainly the most valuable to Regent Pacific. On BCI’s current market capitalization, the BCI stake is worth just over A$68 million. That represents more than a quarter of Regent Pacific’s entire net asset value.

But if BCI was a hot potato once, why make a grab for it a second time? One interpretation in the Hong Kong market is that Dattels and his associates have found a financial backer for a fresh takeover attempt, and that Regent Pacific is building a bloc of shares toward that end, with the aim of issuing a fresh bid at about the same price it offered before.

Another interpretation is that there is nothing strategic about the recent Regent Pacific buying, and that Dattels is doing do more than wagering on the bet that BCI has been undervalued since the collapse of the takeover, and must rise above the takeover offer.

That price was A$3.30. Argonaut Securities, an Australian broker which has been paid to advise BCI and received fees for promoting the Regent Pacific takeover, claimed in a December 2011 report that BCI’s share price should be fairly valued at A$3.40 if the iron-ore price sticks at U$140 per tonne. A report by Austock Securities, released last month, claims the share price should hit a target of A$3.36 if the iron-ore price remains stable or rises. Those are bets on China’s steel production and consumption plans, however.

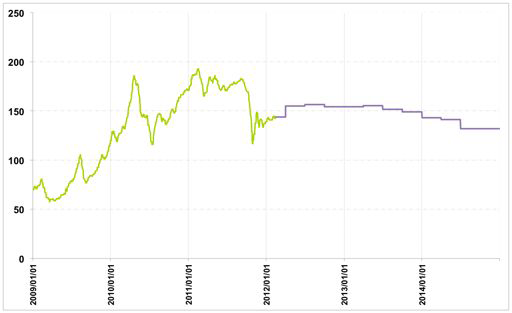

The Chinese iron-ore index shows no reason for short-term optimism:

In a presentation to investors released this week, BCI isn’t optimistic itself. This chart shows the company forecasting an iron-ore price (the benchmark is iron-ore of 62% Fe content delivered at Tianjin port) edging below the $150 per tonne level through 2014; thereafter, the BCI management is anticipating a further drop for iron-ore below the $100 per tonne mark:

Source: http://clients2.weblink.com.au/clients/bciron/article.asp?asx=BCI&view=6582973, p.18.

The fact now revealed that just three stakeholders, plus BCI’s management, control most of the shares means that although the share price may be rising, the liquidity of trading in the stock is drying up. So a bet by Regent Pacific may be defeated by the absence of enough bettors in the market to make the difference.

“In this market, and after all that has happened to BC Iron over the past fifteen months, no one in the market likes surprises,” according to Oleg Sheiko, speaking for the Consolidated Minerals group. “Normally, markets don’t like just two or three shareholders controlling the stock of a mining company. Meantime, we are obliged to defend our position.”

Leave a Reply