By John Helmer, Moscow

When money is at risk, open stock markets generally insist on openness, although there are murky exceptions, especially in Canada.

It also turns out that business secrets are much harder to keep in the Russian market than elsewhere. That’s one reason the Russian risk discount is so high: the ability of Russian stakeholders to conceal material facts of asset value and title, related party transactions, and tax, transfer price and other administrative sanctions is far weaker than you will find in the developed stock exchanges or even in other emerging markets.

Global Ports Investments (GPI), which belongs to Nikita Mishin, Andrei Filatov, and Konstantin Nikolaev, did what the London regulator, Financial Services Authority, required in the prospectus they released on June 16. But then they asked their underwriters – Deutsche Bank, Goldman Sachs, Morgan Stanley, and Troika Dialog (now owned by Sberbank) – to prevent as many people as possible from reading it.

To make the 373-page text even more difficult to follow, the customary inclusion of a search box and scan programme were omitted. So to understand what investors are being told – and also not told – by GPI, it is necessary to read every page. With appreciation to Morgan Stanley and Goldman Sachs, here for everybody’s purposes is the prospectus in full.

For one thing, it is now clear that Mishin, Filatov, and Nikolaev don’t control their business empire through Transportation Investments Holding Ltd. (TIHL) of Cyprus. That entity, according to the prospectus, owns 90% of GPI, and is itself fully owned by Mirbay International, Inc, a company incorporated in the Bahamas. According to the prospectus, Mishin et al. owned 100% of TIHL in 2008. But that was a bad year for Russian transportation, and GPI’s balance-sheet was collapsing:

For a reason that goes almost unrevealed, and certainly not explained, a 10% stake in GPI was sold by the three shareholders to someone else during 2009. What remains in control is Mirbay, but the prospectus says nothing about how Mishin, Filatov and Nikolaev own that company, and with whom.

What is made clear, publicly, is that they have agreed among themselves not to upset their GPI apple-cart without informing the others, and allowing a first option buy-out. “Acquisition of a controlling interest in any shareholder by a third party which is not a member of the shareholder’s group requires that shareholder to notify the other shareholder of the change of control. Under the shareholders agreements, controlling interest is defined as meaning the acquisition of more than 50% of the voting share capital of the relevant undertaking; the ability to cast more than 50% of votes exercisable at general meetings of the relevant undertaking on all or substantially all, matters; the right to appoint or remove directors holding a majority of voting rights at meetings of the board of the relevant undertaking on all, or substantially all, matters; or any other power to exercise a dominant influence over the relevant undertaking.”

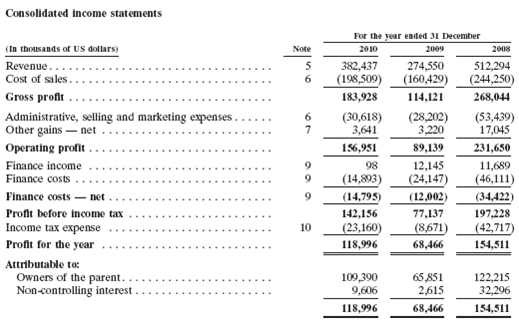

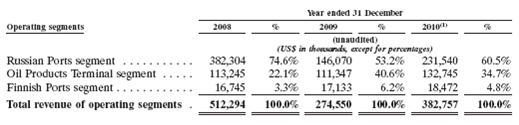

Business is getting better this year, compared to last, and approaching the annual level of sales and profits earned before the 2008 bust:

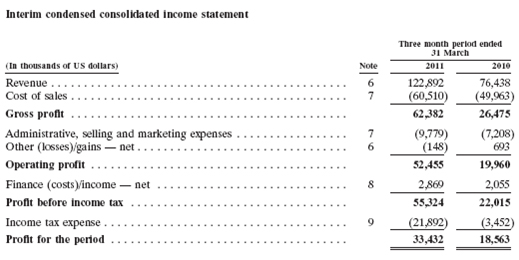

Earnings (adjusted Ebitda) come into clearer focus than is indicated from earlier published data. They look like this:

Taxes are relatively modest, in part because the prospectus reveals that St. Petersburg has granted unusual tax benefits; and in part because Estonia doesn’t tax at all. The St. Petersburg tax relief is for three years. It can be renewed if DPI invests $10 million. The arithmetic is nice – invest $10 million to avoid tax of $11.2 million (assuming annualized gross profit at the level of first-quarter 2011 – more if revenues and gross profit continue growing.)

“The applicable tax rate used for 2010 and 2009 is 20% (2008: 24%) as this is the income statutory tax rate applicable to Russian operating subsidiaries, where a substantial part of the taxable income arises. In the end of 2008 the applicable tax rate for the Russian subsidiaries was reduced from 24% to 20% effective from 1 January 2009. The statutory tax rate for OAO Petrolesport (included in Russian ports segment) is 15.5% (2009: 15.5%; 2008: 20%) because of tax benefits granted by the authorities of St. Petersburg. Effective from 31 December 2009 the tax rate for PLP is 15.5% for the three years that the benefit is granted and 20% thereafter. The effect of this benefit is shown in the tax reconciliation note above as ‘‘Tax effect of reduced tax rates of OAO Petrolesport’’. This benefit expires in three years unless additional investments in qualifying assets over RUR 300 million (approximately US$10 million) will be made in the following year.

“For subsidiaries in Estonia the annual profit earned by enterprises is not taxed and thus no income tax or deferred tax asset/liabilities arise. Instead of taxing the net profit, the distribution of statutory retained earnings is subject to a dividend tax rate of 21/79 of net dividend paid. The effect is included within income not subject to tax in the tax reconciliation note. The statutory tax rate for the Finnish entities is 26%. Deferred tax is provided on the undistributed profits of subsidiaries and joint ventures, except when the policy of the Group is not to distribute dividends from the specific investment in the foreseeable future and the Group can control the payment of dividends. The Company is subject to [Cyprus] corporation tax on taxable profits at the rate of 10%. Up to 31 December 2008, under certain conditions interest may be subject to [Cyprus] defence contribution at the rate of 10%. In such cases 50% of the same interest will be exempt from corporation tax thus having an effective tax rate burden of approximately 15%. From 1 January 2009 onwards, under certain conditions, interest may be exempt from [Cyprus] income tax and only subject to defence contribution at the rate of 10%. In certain cases dividends received from abroad may be subject to defence contribution at the rate of 15%.”

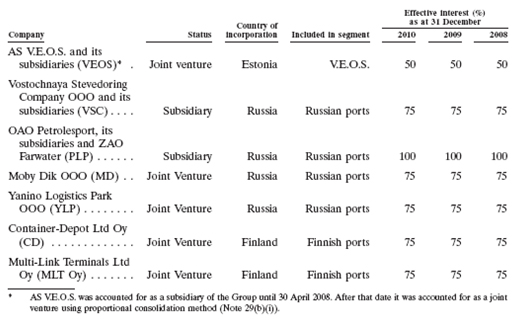

Here’s how the controlling shareholders control the operating units comprising the group.

But the Kremlin’s willingness for political strategic reasons to allow crude oil exports through the Baltic states waxes and wanes, depending on how the Baltic states behave. It should be clear that if Russian crude oil and petroleum exports were reduced by Kremlin order to Estonia, this part of GPI’s business would suffer. That’s because the proportion of revenue accounted for by the Estonian terminal has ranged from 22% of the aggregate to 41%.

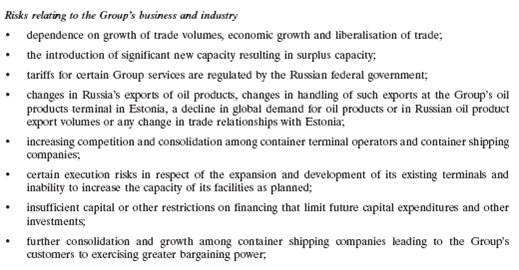

When it comes to identifying the risks of its operations, or of its strategic planning, the GPI prospectus is intentionally vague:

In the amplification of the fourth point, there is no discussion of the variability of oil deliveries between Russia and the Baltic ports, resulting from political conflicts. GPI’s silence on these verges on deception, at least as far as the recent history is concerned. Whatever Russian-Estonian relations may prove to be in future, GPI is apparently banking on stable, in fact increasing oil flows from Russia to Estonia. “The Group plans to commission approximately 360,000 cbm of new storage capacity to be completed in two stages by the end of 2014, which will be able to accommodate different quality of fuel oil, including heavier fractions, and to construct an additional dual-sided 132-position railway unloading facility. In particular, the Group believes that the new railway unloading facility will allow it to accomodate cargo flows from refineries in Russia and other CIS countries located further from the terminals (and requiring more heating and unloading time), not currently served by VEOS. The Group will continue to evaluate opportunities to expand the capacity of its terminal operations in line with market demand.”

If, for example, the politically influential Gunvor group decides that the competitive interest of its new petroleum products terminal at Ust-Luga, on the Russian shore of the Gulf of Finland, would benefit from cuts in the export volumes to rival Estonian ports, does anyone at GPI imagine they would be shy in pursuing that objective? The possibility has not been considered appropriate for GPI investors to consider.

On GPI’s current market share in the Russian container business, its domestic competitors, and the impact of Russian rail company privatization, this is all the prospectus says: “The container terminal industry has in recent years experienced, and continues to experience, significant consolidation, both internally and with the container shipping industry. Consolidation within the container terminal industry results in the Group having to compete with other terminal operators that may be larger and have greater financial resources than the Group and therefore may be able to invest more heavily or effectively in their facilities or withstand price competition. Consolidation between competitor container ports and container shipping companies could also have the effect of reducing the number of shipping customers available to the Group and increasing the access that its competing ports have to the major shipping lines. For example, major shipping lines, such as Maersk, Mediterranean Shipping Company, S.A. (MSC), Evergreen and CMA CGM, operate their own terminals in some countries, and if they were to seek to expand these operations and purchase existing Russian terminals or partner with the Group’s competitors to obtain greater access to Russian terminals, competition may intensify in the Russian container handling market, which could substantially impair the Group’s growth prospects and could have a material adverse effect on the Group’s business, results of operations, financial condition or prospects and the trading price of the GDRs.”

As for its business strategy and the targets of capital investment and acquisition, the prospectus is dully uninformative: “The Group plans to expand its asset portfolio and grow its operations by pursuing ‘‘greenfield’’ projects and through a selective and disciplined approach to acquisitions. The Group will evaluate potential targets against their strategic fit with its existing assets, such as by pursuing targets in regions focused on Russian cargo flows, and the potential for high growth in the relevant market, particularly in Russia, the CIS and other countries with high expected growth and which are complementary to its existing operations. The expansion potential of targets, the ability to achieve operational control and the likely return for shareholders are among key criteria for the Group’s development with a clear focus on the potential value to be created rather than the overall size of a potential project or acquisition. For ‘‘greenfield’’ projects, the Group plans to actively seek ‘‘brownfield’’ terminal sites with the potential to be developed into large-scale container terminals, as well as sites for inland container terminals in and around urban centres in Russia.

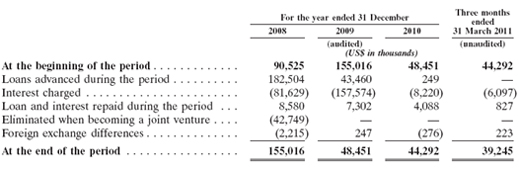

The prospectus treatment of related-party transactions reveals that the control shareholders were borrowing heavily from the operating cashflow of GPI during 2008 and 2009:

Leave a Reply