By John Helmer, Moscow

The Fitch ratings agency has issued a downgrade for Sovcomflot, the state-owned tanker group, claiming the failure of the company to privatize and sell shares, planned for this year, is weakening its ability to cover its current debts, as revenues remain under pressure from poor freight rates. But the debt picture is worsening as more than another billion dollars in bills for the new fleet commissioned by chief executive Sergei Frank (image second from right) come due next year, and in 2014.

Sovcomflot has reported that as of June 30 it must repay short-term loans of $253.3 million over the next twelve months, and is carrying longer-term debts of $2.3 billion; the latter figure is up 8% compared to the debt level on June 30, 2011. In its financial report for the first half of this year, Sovcomflot says its Time Charter Equivalent revenues came to $500.5 million, a year-on-year gain of 4%, but net profit fell 21% to $50.9 million.

According to the latest Fitch release, Sovcomflot’s rating has been cut a notch from BB+ to BB, with Fitch’s added warning that the long-term outlook for Sovcomflot is negative. “The Negative Outlook,” says Fitch, “reflects the inherent uncertainty in the company’s IPO plans pertaining to the timing, the amount to be raised and the proportion to be re-invested into the company. While government privatisation plans remain on the agenda, previous changes of the IPO’s timing, along with poor shipping industry conditions may undermine its likelihood in early 2013, as currently expected, making the company’s recapitalisation plans more ambiguous.”

The ratings report also warns that Fitch “may further downgrade the ratings if the IPO is materially delayed, the proceeds are significantly lower than expected by Fitch and/or shipping sector market conditions are substantially weaker than Fitch’s forecast. The agency may also re-consider its assessment of state support if SCF’s credit metrics continue to deteriorate and re-capitalisation of its balance sheet does not occur.”

Privatization and a public share sale for Sovcomflot have been scheduled and postponed repeatedly by chief executive Frank, by former board chairman Igor Shuvalov (third from right), currently first deputy prime minister, and by other government officials. Part of their problem is that financial advisor Morgan Stanley and other banks are reluctant to underwrite the share sale in a weak tanker market.

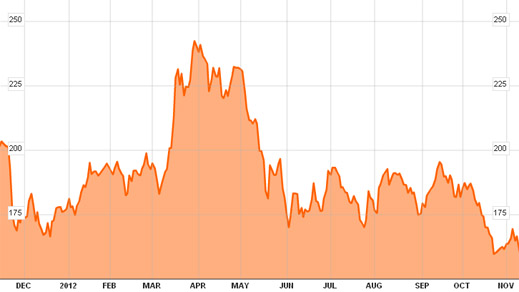

The weakness of global tanker charter rates has translated into highly unpredictable seesawing in the market capitalization of listed tanker companies, as indexed by Bloomberg:

BLOOMBERG INDEX OF TANKER COMPANY CAPITALIZATION, ONE YEAR CHART

Sovcomflot is in a relatively worse position. Transcripts from the UK High Court case Frank brought against his predecessor, Dmitry Skarga, former chief executive of Novoship, Tagir Izmailov (Izmaylov), and former chartering partner Yury Nikitin, and public judgements issued against Frank by Justice Andrew Smith, have sharpened the transparency and accountability problems facing prospectus writers for an initial public offering by Sovcomflot on a regulated stock exchange.

Potential strategic investors approved by the Kremlin, like Gennady Timchenko (far right) and Vladimir Lisin, had been encouraged by Igor Sechin when he supervised the maritime sector as first deputy prime minister. But Sechin’s reassignment to Rosneftegas has reduced his clout over Russian shipping, and sharpened faction-fighting among corporate and government officials who want to share in the rewards of an asset sale – or at least prevent their rivals getting a disproportionate share. As a recent profile by Forbes’s Russian edition of Timchenko’s assets intimates, Frank, his son, and his daughter-in-law, Timchenko’s daughter, are tied to Timchenko’s coattails.

The tanker company is facing more than $1.1 billion in new bills for vessels on order and still under construction. The company says these include one crude oil Aframax tanker, two multifunctional ice-breakers, two Very Large Crude Carriers, two oil product Aframax tankers (LR2 type), two Panamax bulk carriers, two Liquid Petroleum Gas carriers and four Liquefied Natural Gas carriers. These are planned for delivery up to October 2014 at a contract price of $1.58 billion. Less than 30% of that, $441.5 million, has been paid so far.

Last month in London Sovcomflot began UK court-ordered payments of costs and compensation to Izmailov of Novoship. A court ruling on additional claims of bribery by Nikitin, heard in a trial early this year by High Court Justice Christopher Clarke, is expected this week. That will clear the way to a judgement by the UK Court of Appeal on Sovcomflot’s bid to reverse part of the Smith judgements. After that, Nikitin will relaunch his damages lawsuit against Sovcomflot; he is claiming more than $180 million.

Leave a Reply