By John Helmer, Moscow

Fitch Ratings issued a modified warning on Sovcomflot this week, claiming that the big Russian’s tanker revenues were at risk of coming up short against the company’s obligations. In that event, Fitch London analyst Jeannine Arnold reports, Sovcomflot may have to sell off the hulls and newbuildings which are on order, but still on the shipyard slips in South Korea, China, and Finland.

Fitch is also acknowledging that the release of its new ratings report was delayed by several days, and that the ratings agency analysts have come under the pressure of persuasion from Sovcomflot to change their recommended rating.

The full report is restricted, but here is the Fitch press release.

On September 28, Fitch issued a warning that it was considering a negative ratings downgrade for Sovcomflot. The looming problem in Fitch language was the fleet company’s “increased capital expenditure programme over the next few years compared to Fitch’s previous expectations.” The bond market understood that this meant Sovcomflot’s financial capacity to cover its debts is sinking. The immediate impact was selling by holders of last October’s Sovcomflot Eurobond for $800 million, with a 7-year term, and a Fitch rating of BBB- . Had Fitch followed through with a downgrade of that rating, the selloff of the bond was bound to accelerate, and action by Sovcomflot’s bankers likely to follow.

But Fitch didn’t do that. Instead, this is what happened: “In accordance with Fitch’s policies the issuer appealed and provided additional information to Fitch that resulted in a rating action that is different than the original rating committee outcome.” According to Fitch, Sovcomflot’s rating remains unchanged, and the default probability converted from “Rating Watch Negative” to “Negative Outlook”.

The bankers have considerable power because, as Fitch points out, much (in fact, most) of the cash to cover Sovcomflot’s forward shipbuilding debts has yet to be disbursed. Fitch’s way of expressing this is as follows: “Fitch views SCF’s liquidity as adequate, supported by USD319m cash (USD45m restricted) and USD651m of available undrawn committed credit lines (as of 30 June 2011). Whilst excess liquidity is expected to finance a portion of the company’s committed capex programme, liquidity compares well to short-term debt of USD266m.”

Sovcomflot owns up in its last financial report, issued for June 30, to having total bank loans of $2.1 billion; current repayment liabilities of $257 million; and longer-term repayments of $1.8 billion. The use of the phrase “long-term” on the balance-sheet and auditor’s notes is misleading unless it is matched with the construction and delivery schedules of the new vessels. In other words, where’s the money going to come from when the finished vessels must be paid for, before delivery?

Fitch analysts were asked what additional information the agency was given to substantiate the core assumptions spelled out in the release, and on which the report is based – they are that the Russian state budget will guarantee Sovcomflot’s future debt repayments; and that the government’s proposals for privatizing the company and selling shares at an initial public offering (IPO) will result in the sale proceeds going into the company’s treasury for repayment of debt, and not into the state treasury where privatization revenues are usually placed. In practical effect, the two assumptions mean the same thing – if the global tanker market rates go badly for Sovcomflot, the state, Fitch has been assured, will bail the company out with budget funds.

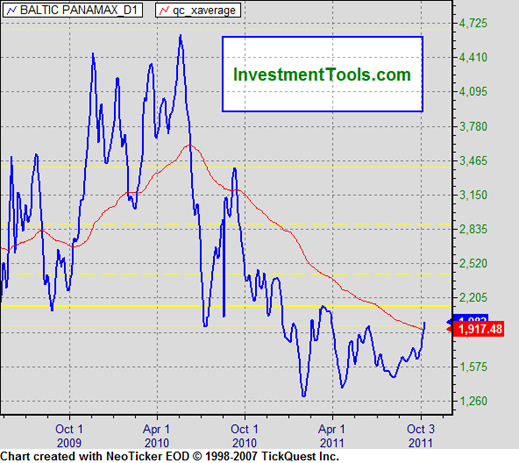

For illustration, this is how the Baltic Exchange of London, the benchmarker for the international tanker market, has charted the downward trend of spot rates for Panamax-sized oil tankers:

When rates were hitting peak between 2007 and 2009, Sovcomflot’s chief executive Sergei Frank and his board chairman, Sergei Naryshkin, decided to order new vessels for the fleet. But as the market rates turned down, Fitch is intimating now that this was a miscalculation. That’s because there are already too many new vessels cruising the seas looking for cargoes, depressing not only the charter rates and fleet revenues, but also Sovcomflot’s capacity to repay the premium prices at which Frank purchased his newbuildings.

For a resume of the new fleet Frank has signed for, here’s the Sovcomflot fleet list, with the newbuilds marked in the green, right-hand column. The shipyards at risk if Sovcomflot can’t meet its payment schedule, or tries selling off the contracts at a bargain price, are STX of south Korea, currently building two gas carriers; Bohai of China, which has two Very Large Crude Carriers (VLCC) under construction; Daewoo of South Korea, with orders for two Aframax tankers; Hyundai Mipo, also Korean, with 4 bulk carriers and 1 tanker; and Arctech Helsinki, 2 supply vessels.

Fitch’s release makes the point that Frank’s wager on new fleet to capitalize on rising rates has failed. “Whilst Fitch recognises SCF’s strategy to acquire vessels during a period of lower vessel purchase prices, and develop its more profitable and more stable LNG and offshore business, the increase in capex, particularly in the context of continuing weak industry dynamics, is preventing the generation of meaningful positive free cash flow as previously forecasted by Fitch.”

What that last phrase actually suggests is negative cashflow in future, hence “the original rating committee outcome” referred to at the bottom of the Fitch release.

Notwithstanding, Fitch claims to have been persuaded that Sovcomflot isn’t at risk because the Russian government will come to its rescue if the tanker market doesn’t improve. So Fitch analyst Jeannine Arnold, principal author of the new ratings report, has been asked the following question:

| One of the assumptions published over your name is incredible, and I wonder why you have introduced it three times without substantiating evidence or sourcing in the Russian government or in Sovcomflot itself:

— “this is to a large extent dependent on the proceeds raised by the intended IPO and the related amount that will be reinvested into the company”” — “The potential receipt of the IPO proceeds by the company would underpin the incorporation of a one notch uplift for state support.” — “SCF hereby has the potential to receive 100% of the IPO proceeds.” Please identify the source, any source, for these assumptions; and identify if you can one example of a Russian state share privatization in which commercial share buyers participated, in which the proceeds went not to the state treasury, as is always announced, but to the state company. |

Apart from the disclaimer in the Fitch release, there has been no response.

The purported decision by the Russian government to guarantee debt repayment by putting the sale proceeds of a Sovcomflot IPO into the company, instead of the state budget, is what Fitch calls its “assumption…IPO proceeds have been included in Fitch’s forecasts. Conversely, if the state is unwilling to at least share a large portion of proceeds with the company, this would undermine Fitch’s assessment of state support, and could result in a rating downgrade.”

Fitch’s release claims that support for its assumption of Russian government support comes from the “Presidential Decree, signed in July 2011 [which] authorises SCF to issue new shares on the condition that the Russian Government retains a 75% + 1 share stake. SCF hereby has the potential to receive 100% of the IPO proceeds.” But Fitch hasn’t compared that decree with the terms of the parallel one, issued by the Russian government on June 29., numbered 1103-P, signed by Prime Minister Vladimir Putin. Because the terms of the decrees aren’t the same, and because of a record of internal government disagreement over the Sovcomflot share sale and its timing, stretching back more than a year, Fitch was asked to identify who in the Russian government provided the assurance which changed its rating recommendation.

Sovcomflot refuses to answer questions from this reporter. Its only public statement to the market through the company’s London spokesman at the time of the Fitch warning was: “SCF don’t wish to make a comment on the Fitch news, except that…it is not a downgrade of their credit rating.”

The practice of ratings agencies seeking government underwriting assurances ahead of ratings decisions related to bond issues of state-owned companies is a sensitive one. In this case, Fitch isn’t confirming that there has been a Russian government undertaking at all. At least not one signed by the newly appointed chairman of the Sovcomflot board, Ilya Klebanov; his replacement of Naryshkin appears to have taken Fitch by as much surprise as it has taken Sovcomflot itself.

Leave a Reply