By John Helmer in Moscow

Everyone who is watching the World Cup has his or her favourite moments of the competition. Depending on their national or other allegiances, many prefer to speak of extraordinary wins; the South African team’s defeat of France 2 to 1, for example. For me, it’s been the bravery of defence against all odds that is more inspiring — Greece against the repeated onslaught against goal by Argentina, to go down 0 to 2; and New Zealand holding Italy to a 1:1 draw.

When rich men purchase football teams, fortitude isn’t what they think of buying, and losing certainly isn’t the target of their investment. On these scores, the Russian rich are no different from Arab oil sheikhs, Greek shipowners, or American bankers, except that there is a more urgent need on the part of the Russian rich to build offshore havens for their wealth, in case their assets are confiscated at home.

For such security, public relations agents are as valuable as lawyers, accountants and bodyguards. If all that the world could find out about Roman Abramovich was his verbal skill, his transaction history, or his tax minimization schemes, he is unlikely to be regarded as significant or as safe as the advertising of his ownership of the Chelsea Football Club has provided. And for that, Chelsea must keep winning. And for that, Abramovich must keep paying.

The problem with paying for winning is that most people believe there is a straight correlation – the more you pay, the more likely you are to win. But this is the public relations version – that the man in charge is responsible for victory; that paying more lifts the odds of success, that today’s win is a good predictor of tomorrow’s outcome. Actually, none of this is true. From the science of probability, all that is sure is that a lot of money properly distributed, and repeated regularly, can convince people that what is false is true.

The great mathematicians of probability theory, as well those who make bookmaking and betting on sport a business, have generated reams of research demonstrating that winning streaks on the football pitch, the basketball court, or the stock market are random dispersions. Take Amos Tversky’s work, for example, on the so-called hot hand in basketball. Fans, sportscasters, and the sports columnists tell you that a player shooting successfully in one or two games is enjoying a winning streak. In fact, when enough games are counted to make measurement of the probability reliable, the finding is that the success of a previous throw very slightly predicts a miss rather than another basket on the next shot.

The Texas Sharpshooter Fallacy is another well-known distortion of cause and effect, winning and losing sequences. Random data are viewed as having meaning in retrospect, because that’s the way we are persuaded to think. The sharpshooter turns out to have been drunk when firing at his barn wall. When he sobers up, he paints a target around the cluster, and claims to be a sharpshooter.

| After Hitler launched the V-1 and V-2 rocket attacks on London, the hits were analysed to suggest clever targeting. In fact, the rockets struck randomly. The thinking mistake was in attributing guidance systems to the rocket, and intelligence to the Germans. In reality, random variation of head and tailwinds, and other factors, were determinative. Apply that to Abramovich, and you might think he has a brain, and that that if he didn’t, Chelsea mightn’t win. Scientifically, the only certain things about this are that Chelsea’s winning and losing streaks are random; and that Abramovich’s money persuades the fans to think otherwise. |  |

Because betting on football is such a lucrative business, a great deal of data-processing effort has been spent on English football results, in order for betting system developers to figure out whether they can profitably predict wins, or goal spreads; or if they can’t, whether they can calculate the odds of game outcomes more accurately than the professional bookmakers. That way, even if wins are unpredictable, system bettors can invest in making money from beating the bookmakers’ mistaken odds.

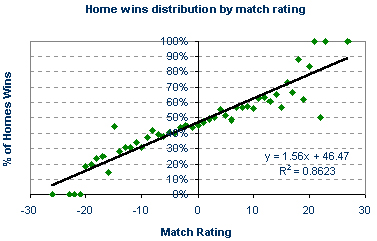

For all the research effort that has gone into this, the only near-certainty that has been discovered in the data is that playing at home in the English leagues increases the chance of a team’s win. If there are sociological or psychological reasons for that – these days very few English football players live in districts where the team stadiums are located, and not so many high-value professional players are English at all – they haven’t been discovered. But this is what one system bettor study claims to be the picture:

No much good, of course, for predicting or betting on World Cup football matches, because all but one team is not at home. Still, since the competition started in 1936, there have been 18 rounds, and the at-home host has won 6 times, and made it into the final another twice. The last time the home team won was four rounds ago, when the French team won in 1998.

| But this is to miss the point of football competition. More profit, much more profit is generated by betting on the game than playing it. The English football competition, for instance, represents the highest value in the world, and also the highest cost. A regular annual audit by Deloitte of the premier league clubs’ financials in the 2007 season found that the clubs grossed £1.53 billion in revenue between them, but spent £1.4 billion on players and other wages, and carried £2.5 billion in debt. |  |

In short, playing looks like a loss-maker. And the UK tax authority is now in court to challenge the way in which owners and players can extract money out of clubs that are insolvent, when all other creditors lose out.

The latest Deloitte report for the pre-crash 2008 season calculates that the premier league clubs took in £1.9 billion in revenues, and spent £1.2 billion on players and their auxiliaries. Broadcasting (or advertising – they amount to the same thing financially) contributed £931 million, or roughly half of the revenues. Net debt at the end of the season had risen 20% to £3.1 billion. Abramovich stands out in the audit, because he spent £123 million on his football club in the 2008 season, making a total of about £760 million spent in the five years Chelsea FC has been under his control.

Deloitte charges £600 for a full copy of the report; £60 if you are a student. But there is no calculation of how much revenue earned in, or borrowed from Russia in total – from Abramovich, Alisher Usmanov (Arsenal), and others, including the Gaydamak family (Portsmouth) – was spent on English football. Abramovich is not known to answer questions; what the others have said doesn’t explain what their profit and loss calculations really are.

In the bigger Russian game, winning football games is secondary to winning the right to be treated as proprietors of the cashflow – something the Kremlin concession system doesn’t allow at all. Never mind therefore that the correlation between that money and football success is limited, as Deloitte acknowledges in its report. “Across Premier League clubs,” the auditor says, “there is a relatively strong correlation between wages and league position. However, in the Championship there is no clear link, which highlights the division’s unpredictability and proof that high wages are not a guarantee of on pitch success at this level.”

When New Zealand held off Italy on the pitch last week, this point was made obvious to everyone in the world. But it will be forgotten just as swiftly, unless New Zealand keeps winning. And that’s improbable.

There is just as little correlation between the chief executive in charge and corporate profitability in non-sporting enterprise, and between fund manager performance at stock-picking and share price movements. Again, to convince punters that this is false, and that success isn’t random, a fortune is spent on broadcasting – advertising, public relations – every day.

Mathematicians call this particular distortion of reality after the town that has nothing to sell but casino games and tax shelters. The Monte Carlo Fallacy is a twist on the attempt gamblers like to make on predicting from retrospective data like coin tosses or roulette-wheel colours. Their mistake is to believe that if deviations from expected behaviour are observed in repeated trials of a random process, then these deviations are likely to be evened out by opposite deviations in the future. For example, if a coin is tossed repeatedly and tails comes up a larger number of times than is expected, the gambler may believe that this means that heads is more likely in future tosses, and he will bet accordingly. That’s his mistake. In fact, the relationship between observed results and future outcomes remains random. There’s no law of averages.

Even if the well-known Russian oligarchs don’t read or are innumerate, they pay handsomely for advisors who can do both. And if they own the casino, they know there is little chance that anyone can come in with a betting system to beat the house. But the Kremlin isn’t a casino, so, again, why do Russian oligarchs spend money on loss-making foreign football teams?

The answer can be found in a story about how their wealth, their winnings in Russia, are generated and transferred abroad each day. Many of these details have yet to be revealed, though the evidence records of current lawsuits under way in the UK High Court are a good place to find them. Until the full story can be published, or the wealth transfers stop, the Russian oligarchs invest heavily in the proposition that reality is football; that winning is everything; and that winners aren’t random hits.

The World Cup media coverage demonstrates just how persuasive this litany of success can be. In reality, the only way a winning streak in sport, the stock market, or Russian corporate profit can be non-random is if there is a fix. And that’s criminal.

By contrast, there is usually nothing wrong, legally or morally speaking, about losing. Also, it may be comforting to think that it’s not whether you win or lose that counts, but how you play the game. Grantland Rice, an American sportswriter, coined that maxim in 1917. If he worked for Deloitte’s sports business group today, Rice might modify the second part of the maxim to emphasize how you bet the game. Less famously, Rice also wrote this ditty about how to count in sports:

“Money to the left of them and money to the right

Money everywhere they turn from morning to the night

Only two things count at all from mountain to the sea

Part of it’s percentage, and the rest is guarantee”

Look carefully at the dice in the illustration, and you will see that they are loaded. For example, notice that some of the white spots that are visible through the transparent cubes appear slightly thicker than others. These are the spots that are loaded with miniature tungsten weights. The difference is clearly visible on the right side die at its upper left edge. If you compare the two white spots you can easily see that one is clearly thicker than the other. |

Leave a Reply