By John Helmer, Moscow

In the criminal fraternity it’s believed that light fingers are a juvenile condition it’s best for the practicioner to grow out of when more serious property transfers are in contemplation.

Alexei Mordashov (lead image, right), the Russian steelmaker and goldminer, is a quick learner and a grown-up. With a net worth currently estimated at over $15 billion from Severstal, Nordgold, and other Russian businesses, his record of asset buying has more often been one of paying too much, and losing money, especially in the US. Last month, however, in litigation in Ontario, Canada, he was charged by shareholders of the gold prospector Northquest Limited, with manipulation of the company’s executives and board in order to take over the company’s gold for a steal.

The resisting shareholders who took their case to the Ontario Superior Court, are veteran geologists with three decades of experience of gold deposits in the Nunavut territory of northeastern Canada, which are Mordashov’s target. The resisters claim Mordashov’s goldmine holding Nordgold has taken over Northquest at a fraction of its real value. “In our view,” Brian Randa, one of the dissenting shareholders, told the court in October, according to the court records, “the valuation [of Northquest’s gold prospects] is not worth the paper it is written on. They [Nordgold] mispresented the true potential of this project by comparing the project to those with much less potential [in gold resources], and by excluding from consideration a vast tract of the licence area. They tricked the shareholders into tendering [their shares at a low price]. The timing of this series of events was deliberately made to happen before the astonishing major Howitzer anomaly was further explored in the summer of 2016.”

Low-balling is a takeover tactic Nordgold has been accused of by Canadian goldmine shareholders at High River Gold and Crew Gold for many years. Mordashov won those battles; for details, read this and this. In those cases, resisting shareholders claimed the light fingers went into Mordashov’s pockets. The Canadian courts and the Ontario regulator didn’t agree.

Northquest has a shorter history than the Pistol Bay gold prospect which is the asset Mordashov wanted. At its initial listing on the Toronto Venture Exchange in October 2009, Northquest was aiming to develop goldmines from prospects in Ontario, and also in the African republic of Mali, as well as in Myanmar (Burma). Follow the document history, here. A year later, Northquest’s founding shareholder and chief executive, Jon North (right), announced a change of geography.

gold prospect which is the asset Mordashov wanted. At its initial listing on the Toronto Venture Exchange in October 2009, Northquest was aiming to develop goldmines from prospects in Ontario, and also in the African republic of Mali, as well as in Myanmar (Burma). Follow the document history, here. A year later, Northquest’s founding shareholder and chief executive, Jon North (right), announced a change of geography.

“Essentially, I choose which rocks to work on and that’s where I go,” North (right) told a regional Canadian mining publication. “Today, the Pistol Bay Gold Project is the company’s top priority. Every aspect of exploration that we have done on this property has shown spectacular results. The Pistol Bay Gold Project’s results are the best results of my career – and I’ve been doing this for 30 years now.”

North didn’t say so, but he was far from being the first geologist impresario at Pistol Bay, or on the gold-bearing seams running north and west for scores, if not hundreds of kilometres.

MAP OF NUNAVUT TERRITORY, WITH PISTOL BAY AND MELIADINE GOLD PROSPECTS

KEY: White=Pistol Bay (Northquest, Nordgold), red=Meliadine (Agnico Eagle)

According to stock prospectuses, the gold in this area of Nunavut had been discovered first by Inco, a major Canadian nickel miner in the 1980s (Inco merged with Brazil’s Vale in 2006). “The mining properties owned by Northquest were discovered originally by Inco in the 1980s. In my then position of Mining Lands Administrator at Inco,” Randa says, “I was responsible for maintaining the rights to the claims where the Vickers deposit is situated while Inco owned the claims during the 1980’s and 90’s.”

When North later came to report to Northquest shareholders on the Pistol Bay Gold Project, the area was enormous. “The Pistol Bay Gold Project consists of 861 square kilometres of mineral rights covering a 90-kilometre strike length of a two-kilometre wide deformation zone known as the Pistol Bay Corridor, which contains numerous gold occurrences. The initial, optioned claims consisted of six claims covering an area of 54.4 square kilometres. Four major campaigns of claim staking and permitting have been completed since and the property now consists of 104 claims covering an area of 861.5 square kilometres. Field operations began in April 2011, and major drilling campaigns have occurred in every summer since.” Vickers was one of the claims. Howitzer was another.

North told the market what Randa and his Inco colleagues, as well as other miners in Nunavut, believed they were all after. “Geologically,” according to North, “the rock formations at Meadowbank, Meliadine, and Pistol Bay are the same age and there is no geological reason for why additional gold deposits will not be discovered and put into production in Nunavut.”

Meadowbank is already an operating goldmine, owned by Agnico Eagle, a Toronto-listed company with a current market capitalization of C$12.8 billion. Meadowbank is currently producing about 1.6 million troy ounces of gold; its reserves and resources, according to Agnico Eagle, may add up to 20 million oz. To the south of Meadowbank Agnico Eagle also owns Meliadine West and East, two potentially rich prospects. They are just 80 kilometres north of Pistol Bay.

The Meliadine prospects were explored between 2006 and 2008 by Comaplex Minerals of Calgary. It then sold out to Agnico Eagle, which commenced its takeover with a down-payment of C$46.9 million for 15.6% of the company. See more here and here. Agnico Eagle has announced that Meliadine turns out to have 3.4 million oz in proven and probable reserves.

North wasn’t the only one who figured the riches filling out Agnico Eagle’s multi-billion dollar value in the market ought to be counted towards Northquest’s capitalization and share value, once Northquest could prove how much gold there was at Vickers and Howitzer, and start lifting it out of the ground. This is how the share prices of the two companies moved over the past five years.

5-YEAR SHARE PRICE TRAJECTORY OF NORTHQUEST AND AGNICO EAGLE

Source: https://www.bloomberg.com/quote/NQ:CN

KEY: yellow=Northquest, blue=Agnico Eagle

The lines can be misleading. As a gold producer, Agnico Eagle was immediately more valuable to investors and share-buyers than Northquest, an explorer. But how much was the gold underground worth? North failed to persuade the market that Northquest was likely to be the El Dorado Agnico Eagle was developing nearby. But North did persuade Mordashov and his men at Nordgold. The Russians decided to try capturing Northquest while the share price was a bargain.

As the chart shows, Northquest’s share price peaked at 89 Canadian cents in mid-October 2012; at that point the market capitalization of Northquest was C$99.3 million. From then on it was downhill. The share price and company value plummeted to a low in January 2015 of 7 Canadian cents for a market cap of just C$7.8 million. By the end of August of that year, the share price had edged up to 9 cents for a market cap of C$10 million.

What happened next was that North met with Russian executives of Nordgold, and they agreed – without exactly telling the market or other Northquest shareholders – that Nordgold would take over the entire company for a premium over 9 cents, but for a capital valuation of the company that was a fraction of what they already had reason to believe it was worth.

Nordgold had started buying Northquest shares carefully enough so as not to trigger too much market enthusiasm, and a large price increase for the share. In June 2014 from its Amsterdam headquarters, Nordgold announced that it had paid C$2.5 million for a 22.3% shareholding in Northquest. The Nordgold report of that deal acknowledged, discreetly, that the neighbours were rich: “The Pistol Bay property consists of 860 square kilometers of mineral rights within the underexplored Rankin-Ennadai greenstone belt. An operating mine at Meadowbank and a development project at Meliadine of Canadian gold producer Agnico Eagle Mines Ltd. are located in the same belt as Pistol Bay.”

Nordgold’s chief executive Nikolai Zelenski (right) was quoted in his company release as saying: “We continue to look for projects that complement and enhance our existing reserves base and we believe we have found in Pistol Bay a very promising asset with real potential. The Pistol Bay project meets our strict investment criteria – namely a potentially high grade deposit with a local partner, which has strong geological expertise in the region.” Actually, Nordgold’s “strict investment criteria” Mordashov had decided, and later disclosed in company papers and presentations, were “not less than 2Moz [2 million ounces] of Reserve potential with grade at above 2g/t [2 grams per tonne], low to medium strip ratio [plus] Potential annual production above 150 koz.”

was quoted in his company release as saying: “We continue to look for projects that complement and enhance our existing reserves base and we believe we have found in Pistol Bay a very promising asset with real potential. The Pistol Bay project meets our strict investment criteria – namely a potentially high grade deposit with a local partner, which has strong geological expertise in the region.” Actually, Nordgold’s “strict investment criteria” Mordashov had decided, and later disclosed in company papers and presentations, were “not less than 2Moz [2 million ounces] of Reserve potential with grade at above 2g/t [2 grams per tonne], low to medium strip ratio [plus] Potential annual production above 150 koz.”

The implication — though no one in the Canadian market appears to have said it aloud at the time — was that Mordashov was buying shares in Northquest because he expected the company to have far more gold than the Canadian market was allowing the share price to reflect. Between the start of Nordgold’s first acquisition and the next one in June 2015, the share price of the company dropped, and the value of the company kept getting cheaper for Mordashov. On June 5, 2015, Nordgold revealed it had paid another C$4.4 million to boost its stake in Northquest to 42.9%. The share price at which it had done that, Nordgold said, was 20 cents. Between then and August 28, the Toronto exchange cut the price of Northquest to 8 cents, before it started rising to the year’s peak, on October 16, of 27 cents.

North met Oleg Pelevin (right), director of strategy and corporate development for Nordgold, at Niagara late in November 2015. Canadian sources say North told them of the meeting. Pelevin’s spokesman in Moscow refuses to confirm the meeting, the date, or what was agreed. By the end of the month, Nordgold had acquired more than 50% of the Northquest shares, and on December 15, it announced a buyout offer for the minority shares remaining. The announcement said Nordgold proposed to “acquire all of the outstanding common shares (“Common Shares”) of Northquest Ltd. (TSX-V:NQ, Frankfurt: NQ3) (“Northquest”) that it does not currently own at a price of CAD$0.253 in cash per Common Share. The Offer values Northquest at approximately CAD$26.9 million (approximately US$20 million) on an undiluted basis.” The 25.3-cent offer was a 15% premium on the December 11 Toronto Stock Exchange price for the share.

and corporate development for Nordgold, at Niagara late in November 2015. Canadian sources say North told them of the meeting. Pelevin’s spokesman in Moscow refuses to confirm the meeting, the date, or what was agreed. By the end of the month, Nordgold had acquired more than 50% of the Northquest shares, and on December 15, it announced a buyout offer for the minority shares remaining. The announcement said Nordgold proposed to “acquire all of the outstanding common shares (“Common Shares”) of Northquest Ltd. (TSX-V:NQ, Frankfurt: NQ3) (“Northquest”) that it does not currently own at a price of CAD$0.253 in cash per Common Share. The Offer values Northquest at approximately CAD$26.9 million (approximately US$20 million) on an undiluted basis.” The 25.3-cent offer was a 15% premium on the December 11 Toronto Stock Exchange price for the share.

Randa and the resisting Northquest shareholders were skeptical. Randa now says: “the [Pistol Bay] property is 90 kilometres long, containing 860 square kilometres. The Vickers deposit covers less than 1 sq. km. The only value assigned [in the expert valuation undertaken for the takeover] was on the Vickers deposit, which only had 69 diamond drill holes as of June 2016. There were 16 other gold targets including the Howitzer target, but they were assigned no value. So you have a Russian company taking out a Canadian company for about $25 million that already has identified one deposit containing $1 billion in gold, and that deposit is in its very early stages of exploration.”

Here’s the Mordashov rub, Randa says. “They are paying US$29 per ounce in situ. When Agnico Eagle took over Comaplex in 2010, they paid $144 per in situ oz., although the property at the time had 5 million ounces, and half of those ounces will have to be mined from underground. Vickers at this stage is a high-grade glory hole – an open pit with an abundance of free gold.”

Most of the Northquest shareholders sold out, but the resisters went to court in October of 2016.

By then Northquest had released a report in April claiming “the Pistol Bay Maiden Inferred Resources [were] 739 koz of gold at 2.95 g/t.” This was the low-ball number on which the takeover price depended. Here is the expert report by the Roscoe Postle Associates (RPA) mining consultancy, in which the calculation was made. Here is RPA’s tabulation:

This RPA estimate was dated March 31, 2016. A week later, on April 8, Beacon Securities of Toronto composed and sent its valuation of Northquest as an independent exercise commissioned by Northquest’s board of directors. Beacon repeated the RPA gold estimate. Based on that number, Beacon considered a sample of comparable transactions and calculated an “implied share price” for Northquest to be between 12 and 18 cents. It then added five different premiums from comparable goldmine deals to this base price, and calculated a weighted average of the results. Beacon’s conclusion – “the Fair Market Value of the subject [Northquest] shares is in the range of $0.251 to $0.335 per share.” Read the full report here. By offering 26 cents, Mordashov was right on the money, Beacon had decided.

But that was April, springtime at Pistol Bay. In July Northquest and Nordgold started a fresh drilling programme at the Vickers and Howitzer deposits. Beacon hadn’t mentioned them; RPA had identified them, and recommended a detailed exploration for both. But RPA didn’t have data to include Howitzer in its reserve count.

Critics of the Nordgold takeover, and of the role played by insiders at Northquest, claim the Northquest share sale was arranged without counting Howitzer, and without full disclosure to the market of its potential.

Nordgold was asked to explain how it was possible for the company to fix an acquisition target of “not less than 2Moz [2 million ounces] of Reserve potential with grade at above 2g/t [2 grams per tonne]”, while at the same time taking over Northquest with reserves of less than a third of that target – “Maiden Inferred Resources [of] 739 koz of gold at 2.95 g/t.” Had the summer drilling programme, which the company now describes as “focused on the Howitzer zone, as well as on extensions of existing drill holes at the Vickers Zone”, produced a trebling or more of reserves?

The company replied through spokesman Olga Ulyeva that it will not reveal what its fresh reserve calculations are until next year. “Nordgold will provide an update on Pistol Bay’s resources and all related expenses in the 2016 Integrated Report, which is not due to be published until 28 April 2017.”

According to the publicly accessible records of the Ontario court hearing at which Randa represented the resisting shareholders, North and the Northquest board, who supported the Russian takeover, and Nordgold executives like Pelevin had violated the stock exchange regulations governing disclosure, fair valuation, and shareholder approval. The dissenters asked the presiding judge, Justice Frank Newbould, to order the disclosure of particulars of the drilling programme at Howitzer, along with the initial exploration results for the volume of gold in that deposit, as well as the grade.

Newbould (right) ruled to dismiss the objections. He noted “[Randa for the resisters] thinks that the company’s prospects were and are better than the prices previously paid by Nordgold. All of that, however, is not before me… there is no evidence before me from which I could find that Nordgold has acted in bad faith in acquiring its shares in Northquest.” He concluded: “It is not for the court to second-guess the business judgement of directors or shareholders who decided to tender their shares unless the plan of arrangement is unfair and proven to be unfair. That is not the case here.”

He noted “[Randa for the resisters] thinks that the company’s prospects were and are better than the prices previously paid by Nordgold. All of that, however, is not before me… there is no evidence before me from which I could find that Nordgold has acted in bad faith in acquiring its shares in Northquest.” He concluded: “It is not for the court to second-guess the business judgement of directors or shareholders who decided to tender their shares unless the plan of arrangement is unfair and proven to be unfair. That is not the case here.”

The takeover offer of 26 cents, finalized by Newbould’s court order of October 6, amounted to a valuation of the company of $26 million.

According to Randa for the resisters, if the results of the summer drilling programme were published, they would “determine how much value we will be fighting for. We believe we can get another valuation, hopefully using different methodology. All I can say is that it is not $0.26.”

According to Ulyeva of Nordgold, as of October 31 of this year, Nordgold has spent US$21.7 million for its Northquest takeover. That’s equivalent to C$29 million — slightly more than the market valuation of the company. It is less than the C$30 million which market sources say North was offered by a rival goldminer in 2012 for a half-stake of the company. North refused the offer.

Then the global price of gold plummeted.

5-YEAR TRAJECTORY OF GOLD PRICE

Source: http://www.infomine.com/investment/metal-prices/gold/5-year/

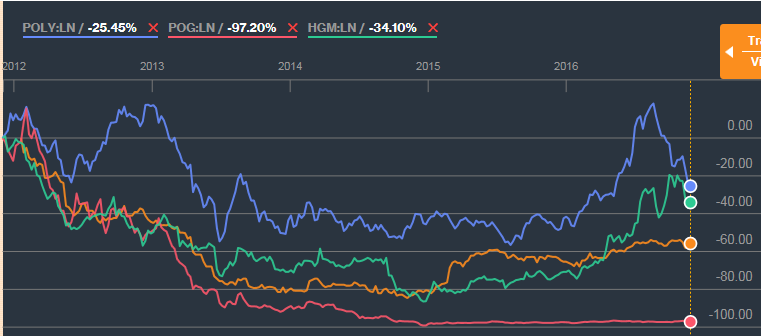

The share prices and the market capitalizations of the listed Russian goldminers also fell in the same period.

5-YEAR SHARE PRICE TRAJECTORY OF LONDON-LISTED RUSSIAN GOLDMINERS

CLICK ON CHART TO ENLARGE

KEY: blue=Polymetal (-26%; yellow=Nordgold (-56%); pink=Petropavlovsk (-97%); Highland Gold (-34%)

Source: https://www.bloomberg.com/quote/NORD:LI

For Nordgold, Mordashov could count that from February 2012, when his company’s market capitalization was $2.8 billion (share price of $7.40) to November 2014, when the cap was $444 million (share $1.20), he had lost more than $2.3 billion in equity value, not to mention borrowing capacity at the bank. A London mining analyst comments that if Mordashov calculated he had to boost Nordgold’s gold reserves in order to resurrect his share price, the only way he could do that was to find gold assets on the cheap. “There are no cheap Russian gold assets,” according to Moscow gold mining sources. One adds that Mordashov has overpaid for such assets in the past – “he can’t afford to do so again.”

North’s Northquest in Nunavut in Canada was ideal from Mordashov’s point of view. The company reported that its loss in the December quarter of 2015 was $1.3 million, almost double the loss of the same period of 2014. In North’s management report of February 23, 2016, the outlook for Northquest was grim. “The Corporation,” North told the market, “will need to secure additional financing to meet its ongoing obligations; however, there is no assurance that the Corporation will be able to do so.”

But North already knew Nordgold would underwrite the financing with more valuable assets to secure bank loans. North’s pay in the company was also booming. According to this company disclosure, in the last quarter of 2015 his compensation jumped 3.5 times compared to the last quarter of 2014:

Source: http://www.northquest.biz/uploads/File/financials/2015_12_31_MDA.pdf

Other directors also hit pay dirt. All of them, according to an INK paper on insider dealings, were heavy sellers of shares to Nordgold.

North was asked to confirm his meeting with Nordgold at Niagara in November 2015; the terms of his compensation when he agreed with Nordgold to step down from the board and resign as chief executive. He was also asked to say whether he had done better out of the Nordgold takeover than the $30 million he had refused in 2012 as too little. North has not replied at press time.

Nordgold was also asked to confirm the Niagara meeting and North’s exit terms. The company spokesman referred to a company notice to shareholders of June 2, 2016, in which it was reported that “in connection with the Amended Offer, Dr. North is required to resign as Chief Executive Officer and will, at the effective time of his resignation, become entitled to receive a lump sum payment in an amount equal to $708,908.” Did this mean that in addition to his severance deal with Northquest, North also had an exit deal with Nordgold? Ulyeva for Nordgold says “there were no other agreements or arrangements.”

By the Russian standard in annual production and volume of reserves, Nordgold is not the current leader. On the top-10 Russian miner table, Nordgold ranks 6th.

TOP-10 RUSSIAN GOLDMINING COMPANIES

Source: Northquest-Russian Gold_survey_2016_ENG.pdf

By market capitalization, Nordgold moves up a peg or two. Polyus, now Moscow (MICEX) listed, leads with the rouble equivalent of $13 billion. On the London Stock Exchange Polymetal comes second at £3.3 billion (US$4.1 billion). Nordgold trails well behind at $1.3 billion, but that’s still far ahead of Petropavlovsk and Highland Gold. Nordgold’s current debt, secured in part by its shares and share price, was reported at September 30 to be $871.3 million. The 9-month financial report also reveals that so far this year US$4.1 million had been spent on proving more reserves and resources at the Pistol Bay tenement, “focused on the Howitzer zone, as well as on extensions of existing drill holes at the Vickers Zone.”

Mining analysts in Moscow and London point out that in order for Nordgold to lift its share price and market cap, and lower its borrowing costs, it should show substantial growth in mineable reserves. “To do that, Mordashov found Northquest. At the takeover price, it was like gold lying on the surface.”

Randa concludes: “If all of the companies listed on the TSX Venture Exchange were allowed to be taken out like Northquest is being taken out by Nordgold, there would be no TSX Venture Exchange.”

Leave a Reply