By John Helmer, Moscow

On December 7, 2012, Andrei Melnichenko (image right, right) told prospective buyers of $750 million in loan participation notes that he was gung-ho on the future of the potash business of his Eurochem group. For Eurochem — 92% owned by board chairman Melnichenko; 8% by chief executive Dmitry Strezhnev – potash was, still is, a brand-new line of business. But in a decade or so, Melnichenko told investors, he aimed to be number-1 for potash in Russia and in Europe; and for potash, nitrogen and phosphate fertilizers combined, close to number-1 in the world.

Apparently nothing stood in his way – not Uralkali, Russia’s current potash monopoly producer; nor Suleiman Kerimov (left, left), the control shareholder of Uralkali. Not Belaruskali, the state-owned potash monopoly of Belarus, nor Belarus President Alexander Lukashenko. Those four names don’t appear in the risk or strategy sections of Melnichenko’s investment prospectus, a copy of which has just fallen from a Eurochem truck. How he proposed to defeat such rivals the Eurochem prospectus didn’t even acknowledge as a problem. Can Melnichenko have been so unthinking as to expect his rivals to surrender their market positions and profits without a fight? Did Melnichenko take his bond buyers for dolts and boobies?

Just sixteen days after Melnichenko’ prospectus, on December 22, 2012, in Minsk, President Lukashenko signed Decree No.566. This cancelled the exclusive right of the Belarusian Potash Company (BPC) to export potash produced by the Belarus state producer, Belaruskali. The practical impact was unmistakeable – it threatened unrestricted competition from what Lukashenko’s decree called “other organizations selected by the head of state.” In the preceding weeks, the international spot price for potash had dropped from the year’s peak of $476.25per tonne to just $425 – a drop of 11%. After Lukashenko showed his hand, potash slipped to $395.

POTASH SPOT PRICE CHART, SEPTEMBER 2012-AUGUST 2013

Seven months later, Uralkali, the Russian partner in the potash sales cartel managed by BPC, fired its retaliation shot on July 30, 2013. Uralkali announced it was pulling out of BPC altogether, selling its own potash through its Swiss trading company in as large a volume and at as low a price as the market would bear. That story can be read here. The outcome is that for the foreseeable future the price of potash will be lower than the cost at which Eurochem’s proposed new mines can produce. As Lukashenko and Kerimov slug it out, they appear to have floored Melnichenko’s championship bid with a phantom punch.

That leaves the Eurochem prospectus of December 2012 – and the question of whether Eurochem misled its investors, either intentionally or negligently.

According to page iii, “the opinions, expectations and intentions expressed in this Prospectus with regard to EuroChem and the Group are honestly held, have been reached after considering all relevant circumstances and are based on reasonable assumptions; (iv) there are no other facts with respect to EuroChem, the Group, the Notes or the Loan the omission of which would, in the context of the issue and offering of the Notes, make any statement in this Prospectus misleading in any material respect.” Read the 432-page document here.

Potash was the key to Eurochem’s future, the prospectus declared, because Eurochem was promising to “become one of the five leading mineral fertiliser producers in the world in terms of production, sales and profitability. To achieve this objective, the Group has been implementing a strategy that includes the following key elements: diversifying product range, building and launching own potash production and further improving product quality.”

The prospectus indicated that Melnichenko was planning to spend $3.5 billion on boosting his potash business from zero production to 8.3 million tonnes per annum within a decade or so. Over the same period Uralkali’s annual capacity over the same period is projected to rise from 11 million and 15 million tonnes, with extra mineable volume of another 5.5 million tonnes per year on call after 2020. That’s almost 21 million tonnes for Uralkali. Add Belaruskali’s capacity to lift from 6 to 10 million tonnes on to the market (in 2012 output was 7.9 million tonnes). Was Melnichenko really thinking of topping them both?

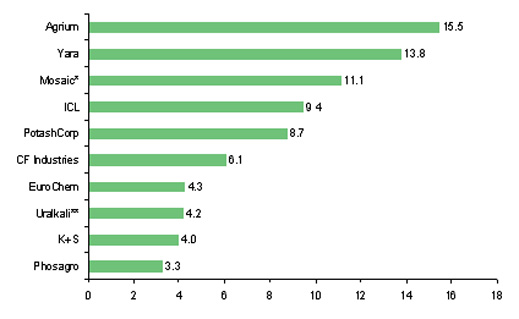

According to the Big-Fert revenue table in the prospectus, Eurochem saw itself with its nitrogen and phosphate sales as already running ahead of Uralkali. The purpose of the $750 million bond issue, Melnichenko implied, was to match Uralkali’s 2012 potash output, and more than double Uralkali’s sales revenues. He didn’t exactly say so, but the implication was clear – Melnichenko was telling Kerimov, до свидания.

GLOBAL FERTILISER COMPANY COMPARISON BY 2011 REVENUES

Source: Eurochem prospectus, page 52

In the risks section, the prospectus acknowledges that “the global and domestic fertiliser industries are highly competitive and the Group may not be able to compete successfully.” That’s obvious now, in retrospect. But last December, this is how Eurochem reported the market competition. “Fertilisers are global commodities, with little or no product differentiation, and customers make their purchasing decisions principally on the basis of delivered price and, to a lesser extent, on customer service and product quality. The Group competes with a number of domestic and foreign producers, including state-owned and government-subsidised entities. Some of these competitors have greater resources and are less dependent on earnings from fertiliser sales, which makes them less vulnerable to industry downturns and better positioned to pursue new expansion and development opportunities. Some of the Group’s traditional competitors (in the global markets, Yara (Norway), PotashCorp (Canada) and The Mosaic Company (USA), as well as other producers in North America, North Africa, the Middle East and Asia, and, in the Russian and the CIS markets, PhosAgro, Acron, Uralchem, Sibur and Mineralnye Udobreniya) also benefit from control over or access to raw material reserves, functional locations near major suppliers or consumers, market reputation and long-standing trade relationships with global market participants.”

Not a word about the potash market there — the Russian mentions are nitrogen and phosphate producers. There is no mention at all in the prospectus of Belaruskali.

Melnichenko was born in Belarus, so he knows where it is; who’s in charge; and how important potash revenues are to the state budget, and to Lukashenko personally. The prospectus reports as its second category of risks that “changes in government policies could have a material adverse effect on demand for and prices of the Group’s products.” But Belarus is ignored, and there is no reference to what Lukashenko was about to decree. This is despite the fact that it was well-known in the potash market that Belarus’s strategy has been to stabilize income from potash sales by selling larger volumes, and for several years it has been exporting potash cargoes outside the BPC cartel limits.

So too, on a smaller scale, was K+S, the European fertilizer producer in which Melnichenko is the largest shareholder. Melnichenko’s nominee on the K+S board, George Cardona, also sits on the boards of the Cyprus companies through which Melnichenko owns Eurochem. Cardona also sits on the board of the Isle of Man company which owns the art works in Melnichenko’s house and garden; and the companies which own Melnichenko’s airplane, boat, and other assets.

The records of a recent federal US court lawsuit over the disputed price of a sculpture for Melnichenko’s garden reveal how closely Melnichenko and Cardona watch the prices of the art market. So if Cardona had been doing his job, he would have been telling Melnichenko how threatening Lukashenko and Belaruskali were to the potash price and the break-even price for Eurochem’s potash mines long before the December 2012 decree. So why was the Eurochem prospectus silent?

Buyers of Eurochem’s bonds were told “the Group faces risks related to the development of its potash deposit license areas”. But this was an acknowledgement of technical and contract problems at the Gremyachinskoye mine in Volgograd region, not the cost and profitability of potash at the minehead, if global prices fell sharply. The Volgograd story was told here.

Special Russian risks were acknowledged in the prospectus because “emerging economies, such as Russia, are subject to rapid change and that the information set forth herein may become outdated relatively quickly.” Commentary from Belarus on the potash market always assumes that Uralkali and its shareholders act in concert with Kremlin policy. By contrast, the Eurochem prospectus told bondholders it couldn’t predict what might happen. “State authorities have a high degree of discretion in Russia and at times exercise their discretion arbitrarily, without conducting a hearing or giving prior notice, and sometimes illegally.” Was this a hint from Melnichenko that he wasn’t confident where his proposed new potash business stood with the Kremlin?

For a fund-raising intended for Melnichenko’s potash strategy, the prospectus is puzzling because it makes minimal reference to the Russian potash market. There are just these three lines on page 135: “In the potash segment of the mineral fertiliser market, Uralkali is the largest Russian producer. In 2008, the Acron Group obtained a license to develop the Talitsky area of the Verkhnekamskoe potassium deposit.”

Omitted from disclosure was the likelihood that the combination of potash expansion plans from these two would dwarf Eurochem’s strategy; potentially doom it. In November 2012, the month before Eurochem finalized the prospectus with its bankers – Barclays, Citi, BNP Paribas, and Sberbank’s CIB subsidiary in Cyprus – Acron reported that it had raised $400 million from two Russian state banks, VEB and Eurasian Development Bank, plus Raffeisen. This was for Acron’s new Talitsky potash mine; its target production capacity of 2 million tonnes is planned to come on stream between 2016 and 2018. To make this possible Acron has given up shares in the new mine for the cash, ceding the Kremlin 29% equity in the project. Melnichenko has ceded no shares at all.

There are 162 pages of audited financial reports in the Eurochem prospectus, and they carefully omit identification of Eurochem’s bank lenders. “A leading Russian bank” was reported to have loaned Rb20 billion (now $606 million) for a 5-year term (September 2016), but the other lenders of about Rb64 billion ($2 billion) in Eurochem debt appear to be non-Russian. The only mention of Sberbank in the prospectus is its involvement in the sale of K+S shares held as collateral. A recent report suggests that the non-Russian banks have grown much more reluctant to lend to Eurochem after the breakup of the potash cartel became public.

Sberbank appears to be Melnichenko’s only state banking sponsor. Country risk, as the Eurochem prospectus acknowledges about Russia, includes unpredictability of state policy. Search the prospectus for the term “arbitrary”, and you will find four references, each identifying the possibility of a Russian government or state action “which could have a material adverse effect on the Group’s business.” Mitigating that risk is elementary practice for Russians, even Belarusians like Melnichenko, by sharing the risk exposure with the state banks; their risk and credit committees, and boards of directors, make sure of Kremlin approval at the highest level required for the amount of risk involved. This is why the volume of credit and share collateral securing state bank loans to potash mining projects is a telltale measure of Kremlin underwriting. The special relationship of Acron’s control shareholder, Vyacheslav Kantor, with President Vladimir Putin has also been reported before.

So what would Eurochem’s bond buyers have understood about Melnichenko’s potash prospects had they known last December what is obvious now? Uralkali and Acron far outweigh Eurochem in state bank underwriting; Sberbank’s commitment appears to be to Eurochem’s nitrogen business, not to potash.

Eurochem has issued a single comment on the potash market since the July revolution began. In its second-quarter financial release, issued on August 14, the company said: “Following the announced withdrawal of Uralkali from BPC, the probability of a migration of the potash market toward a more commodity type structure where prices are based on marginal producer cost levels has increased. This has no bearing today on our investments and commitment to potash. Given the fairly advanced development stages of both of our two greenfield potash projects and their projected position on the global cost curve, the break-even potash price necessary to justify future investments is meaningfully below today’s marginal producer level.”

There has been no specification of that price threshold, not in the bond prospectus, nor since. Melnichenko’s spokesmen in Moscow and London refuse to respond to requests for clarifying their chief executive’s earlier suggestion that break-even was around $400. If Melnichenko was tiptoeing, tripping, or bluffing towards an exit when he posted the December 2012 prospectus, the writing was on the wall. It just doesn’t appear to be inside the advertisement.

Coming soon: Vladislav Baumgertner’s writing on the wall of his prison in Minsk.

Coming soon: Vladislav Baumgertner’s writing on the wall of his prison in Minsk.

Leave a Reply