By John Helmer, Moscow

Alrosa has announced new strategic targets until the end of 2021, following this week’s meeting of the Supervisory Board, as Alrosa’s board of directors is known. How much of the projected growth will depend on Alrosa getting the Kremlin to persuade Vagit Alekperov of LUKoil to do what he doesn’t want to do is the big question for them all — especially for Deputy Prime Minister Igor Shuvalov, who has been demonstrating sharp interest recently in the price he can arrange for an Alrosa asset sale.

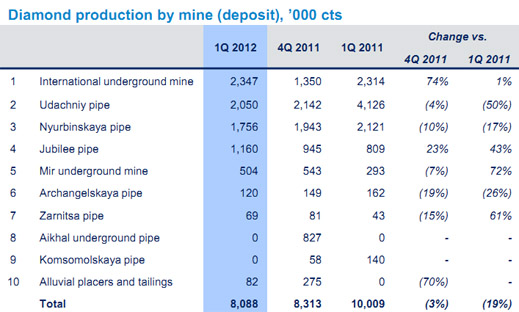

An Alrosa statement says its current diamond production level of about 34 million carats per annum will be lifted to between 38 and 40 million carats, a cumulative growth rate of 6%, by increasing production at the new underground mines in Yakutia, and expanding open-pit production at mines in the Arkhangelsk region of northwest Russia. At the same time, the company’s diamond reserves are to be lifted to 1.19 billion carats, a 61% increase over their present level.

To fulfil these targets and retain over De Beers what Alrosa refers to as “leadership on the world market”, the company says it is counting on a smooth and successful transition to underground mining in Yakutia (Sakha Republic). But it is dark five hundred metres underground, and the geological risks and costs of mining diamonds at that level are notoriously uncertain, as Alrosa acknowledges. “The share of rough diamonds from open-pit mines will be systematically reduced from 72.8% in 2011 down to 40% in 2021, and the volume of rough diamonds from underground mines will grow from 27.2 up to over 60%, respectively. However, there are objective risks of production reduction, which are conditioned by geological features of the deposits and some possible changes in mining conditions at the mines under construction.”

As a hedge against these risks, Alrosa says it aims to expand output at Severalmaz, which is developing an open-pit mine at the Lomonosov diamond field in Arkhangelsk. In its latest annual report for the year 2011, Severalmaz reports it produced 556,800 carats. This appears to be the design capacity of the mine.

According to Alrosa’s new plan, by 2021 it hopes to lift its diamond sale revenues to about $12 billion, an almost threefold jump compared to last year. This is achievable, the company is claiming, if diamond demand grows by 38% to 2021, according to the Alrosa forecast, and if it can capitalize on higher grades and qualities from the underground sources. Investment to get at the underground stones is estimated to total Rb234.6 billion ($7 billion). Additional reserves, Alrosa says, will come from “the possibility of purchasing diamond-mining assets, first of all, on the territory of the Russian Federation.”

This statement appears to be a discreet but categorical rejection of reports over several months that Suleiman Kerimov, a Moscow businessman who represents the interests of government officials, is proposing that Alrosa attempt to acquire BHP Billiton’s Canadian mines. Independent sources say BHP has closed the bid book for the assets, and Alrosa is not participating.

Another source of potential production and reserve growth is the Grib pipe, or the Verkohtina project, which had been developed by Archangel Diamond Corporation (ADC) until it was seized by LUKoil, the owner of Arkhangelshgeoldobycha (AGD), a regional diamond explorer. The Grib site is less than 50 kilometres from the Lomonosov field. Reserves were estimated by De Beers, when it owned ADC, at 98 million tonnes of kimberlite to a depth of 500 metres, containing an estimated 67 million recoverable carats. The grade was estimated by De Beers from 69 to 82 carats per 100 tonnes.

According to the mine plan of LUKoil and AGD, it aims at excavation of 4.5 million tonnes of ore in the first year of operation; 58 million carats over the first sixteen years; 3.6 million carats output per annum; and a mine life of up to 35 years, depending on the underground conditions, waterlogging, and costs. Adding the Grib pipe to Alrosa’s reserves would make about 15% of this week’s Alrosa estimate of its aggregate increase in reserves.

LUKoil has been advertising its desire to sell off the Verkhotina project since 2009; the offer was renewed publicly in February of this year. In a newspaper report this week in Moscow, Alrosa appears to be offering to swap gas fields it owns in the Russian fareast for the Grib pipe. According to a report by Maria Yegikyan, an Alfa Bank analyst, “Alrosa’s gas assets include Geotransgaz and Urengoy Gas Company, with a reserve base of 187bcm of natural gas and 26.4mt of gas condensate in the YANAO region. The gas assets are expected to start production toward the end of 2012, with output expected to reach 1.8bcm of natural gas and 250kt of condensate pa. The company’s investments in the respective assets seem to be equal at around $800m…LUKoil has not expressed interest in Alrosa’s gas assets, leaving room to question whether LUKoil is interested in the transaction.”

Spokesman Vladimir Semakov said LUKoil is not commenting on any contact it may have with Alrosa on this issue. This week, following the signing of an agreement with the Arkhangeslk region governor, Alekperov announced that the Grib mine will be commissioned in 2013, and that LUKoil is planning to invest more than $850 million in the project.

Alrosa has also been reported to be in negotiations to trade the gas assets to the state-owned oil company Zarubezhneft, which may in turn be absorbed by Rosneft. The cash valuation which has been reported for the Zarubezhneft deal is between $609 million, which Alrosa paid for Geotransgaz and Urengoy in 2009, and $1.1 billion, the price required for its buy-back agreement with VTB Bank in 2011. The pricing of these transactions has apparently allowed an exceptional amount of socialist sharing on the part of the leading liberal reformer in the Russian government, former Finance Minister and Alrosa board chairman, Alexei Kudrin.

If the diamonds are part of a larger deal between the state oil companies and LUKoil, Alekperov may be obliged to take a lower price than he wants to let Alrosa have for the Grib pipe.

Diamond industry sources in Moscow don’t believe Alrosa has much leverage against LUKoil. “Alrosa doesn’t have administrative resources in a contest with Lukoil. Regarding the administrative resources, these are limited to Yakutia and the diamond-consuming public. Other administrative resources they do not have.”

Another source close to Alrosa says: “Alrosa is unlikely to be able to use their administrative resources to exchange assets. [About alternative buyers LUKoil can approach for selling Grib] that is a question. Really, except for Alrosa, it is unlikely anyone will be able to engage this asset. On the one hand, this asset is hardly of interest to someone else, as far as I know of the condition of this asset, as it requires astronomical investment. An economy of costs and investments there can only be realized [at Grib] when applied in connection with Severalmaz. On the other hand, as far as I know, all these [legal] proceedings, in which Lukoil is involved with the Canadian side [ADC], are not over yet; there is an opposition war and the conflict has not yet been settled. So it is not quite understandable how the [swap] transaction can be completed, if the proceedings have not yet ended.”

The source also believes that if Alrosa has the means, it can develop new diamond mines in Yakutia. “There are potential resources which need to be explored and put on the balance sheet. With appropriate investments Alrosa could find assets in Yakutia. The only problem is that during the entire existence of Alrosa [since 1993], investment in the exploration of potential new fields has been limited. What was exploited was left over from Soviet times.”

Leave a Reply