By John Helmer, Moscow

In countries where sugar is grown as a consumer staple or for export, the stuff is proverbially blamed for the temptation to exaggerate and to steal. In Madagascar, they say “truth is like sugar cane. Even if you chew it for a long time, it is still sweet.” But in Malawi, they say: “ants die in sugar”. If this means you can chew too much on a good thing, that isn’t so in India. According to the Indian maxim, “stolen sugar is the sweetest.”

In the villages of western Russia – one of the world’s largest producers of beets — the proverbial wisdom doesn’t even recognize the sugar content of the crop. In fact, the villagers warn: “Shut up, you beets! Remember shchi is cooked with cabbage.”

On April 29, Ros Agro (ticker AGRO:LI), one of Russia’s largest sugar producers and one of the London market’s sweetest Russian stocks, suddenly went sour. Almost 5 million shares, a record number for a day’s trading in Ros Agro, were sold, causing a price collapse. Was Vadim Moshkovich, the control shareholder, selling? Moshkovich is not explaining. So which is it – a case of the stolen sugar of the Indian proverb, or a case of the familiar Russian soup?

Ros Agro is the name of the London-listed stock. It is a holding, registered in Cyprus in 2009, which owns 100% of the Rusagro Group. This entity was registered in Russia in 2010 to hold more than 600,000 hectares of farm land; crops of beets, grains, soy beans and sunflowers; sugar and seed-oil refineries; manufactories of mayonnaise and margarine; pig and beef lots; abattoirs and greenhouses.

CLICK TO ENLARGE

Source:http://www.rusagrogroup.ru

The history of Rusagro goes back to 1994, when according to the company’s documents Moshkovich, then 28 and a fresh Moscow university graduate in applied mathematics and electronics, started a business of importing “Ukrainian white sugar to [supply] major Russian confectioneries.” He then moved upstream, first to acquire sugar refineries; then the farms to supply the beets for processing. From sugar, Moskovich diversified into the other crops and meat. The map shows how the company’s farm production is concentrated in the far west and in the far east, with refining and processing plants in the central Ural and Volga areas.

A map of the company’s corporate structure reveals that the listed Cyprus holding owns the Russian registered holding, which owns in turn nine regional production companies. But the Cyprus holding also owns a British Virgin Islands (BVI) entity, Limeniko Trade and Invest. The function of Limeniko reported in Rusagro’s most recent stock exchange prospectus is “commodities acquisition and hedging operations”. In other words, the cashflow of the group’s sales is managed offshore in Cyprus and BVI, while payments of Moshkovich’s dividend share of the profits earned on the trading operations run from Cyprus to his shareholding entity in BVI, called Shiny Property.

CLICK TO ENLARGE

Source: page 111 of http://www.rusagrogroup.ru/fileadmin/files/prospectus/IM_final.PDF

The scheme handily minimizes Russian taxes on transfer pricing and sales within the group, as well as Russian and Cyprus taxes on the lion’s share of the dividends going to Moshkovich. This is acknowledged in the prospectus as a risk for other shareholders tempted to buy into the company. “The Company and its foreign subsidiaries intend to conduct their affairs so that they are not treated as having a permanent establishment in Russia, no assurance can be given that they will not be treated as having such a permanent establishment. If the Company and its foreign subsidiaries are treated as having a permanent establishment in Russia, they would be subject to Russian taxation in a manner broadly similar to the taxation of a Russian legal entity.”

According to a well-known British commodity broker, the Russian sugar trade is “exceptionally murky”.

For background on Moskovich, and the company’s initial public offering (IPO) in London in April 2011, read this. For more on his principal rivals in beet cropping and sugar production in Russia, Prodimex and Dominant, read this.

It is unclear what help Moskovich (below, left) received, and how silent his partners have been in his asset acquisition history. His best-known business partners in the public record are his wife Natalia Bykovskaya (centre), and friend from student days, Sergei Kirilenko (right). An account of their story together can be found in this Wikileaks file.

Less silent have been the asset shareholders who claim to have been targeted by Moshkovich for hostile takeovers. Their claims can be followed in this compilation of the Russian press reports over the past decade. Moshkovich also has substantial urban real estate investments, and a stake in Sobinbank, where he was board chairman for a while, and Kirilenko chief executive.

RusAgro’s latest share-sale prospectus, was issued in April for a secondary public offering (SPO) arranged by JP Morgan, UBS and VTB. About Moshkovich’s history, the document says: , “in the past, mass media in Russia, including those that are established and well-known, published information regarding alleged criminal charges against Mr. Vadim Moshkovich, our controlling beneficial shareholder. According to Mr. Moshkovich, information on any criminal prosecution and charges against him which appeared in the mass media is false. The Group has not conducted any independent investigation regarding such allegations and does not have a view regarding the veracity of such allegations.”

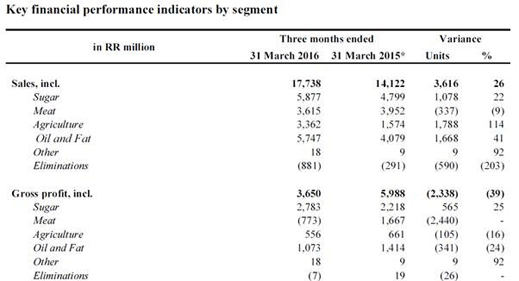

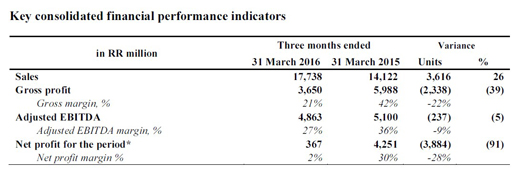

These days, according to the company’s first-quarter 2016 report, sugar is Rusagro’s leading profit-maker, but the company’s financial indicators show considerable diversification into other farm products. In the aggregate of the group’s revenues, sugar comprises 33%, meat 20%, oil and fat 32%; and grains 19%. However, for profit, sugar makes up 76% of the group total. Sugar comprises 48% of earnings (Ebitda).

Key: Sugar: branded in the Russian market as Chaikofsky, Russkii Sakhar and Brauni

Meat: pork with beef production planned

Agriculture: sugar beet, grains (wheat, barley, corn, peas), soybeans and sunflowers

Oil: sunflower oil

Fat: margarine, branded as Provansal and Schedroe Leto; mayonnaise brand ed as Mechta Khozyayki.

Source: http://www.rusagrogroup.ru/fileadmin/files/reports/en/pdf/Press_release_-_03M_2016.pdf

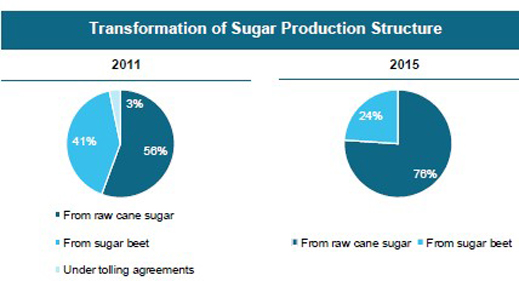

According to a company presentation given in London early this month, domestically grown beets are giving way to imported sugar cane in Rusagro’s sugar production chain:

Source: http://www.rusagrogroup.ru

This is despite the priority being given by the government to import substitution and increasing self-sufficiency from domestic output. The current state food security plan aims at domestic sourcing by the year 2020 for 90% of the sugar in the market. Russian customs figures show that the principal source of imported sugarcane for Russia is Brazil. Thailand used to come second, but has been overtaken by Cuba. According to state policy, beet-supplied sugar for Russian consumers should be tipping over the 5 million tonne mark per year, while the volume of cane-supplied sugar and imported refined sugar should be dwindling. This is not quite what is happening, as can be read in reports by Evgeny Ivanov, the expert on sugar at Moscow’s Institute for Agricultural and Market Studies ( IKAR).

According to Rusagro, it is receiving substantial state budget support for import substitution. Subsidies covering part of the interest owed on bank loans are part of this support; so are subsidies, as well as outright grants for purchase of fertilizers and farm equipment. Tax relief includes zero income tax for crop and meat producers, and a 10% value-added tax (VAT) rate instead of the standard 18%. Sugar production is backed by a market price support scheme and import duties. Pork production is supported by import quotas, penalty import duties, and a counter-sanctions ban on European, US and Canadian exports. In 2014 the company says it received interest subsidy payments of Rb2.1 billion ($55 million); in 2015 Rb1.8 billion ($30 million).

The company doesn’t estimate the revenue value of these state financial supports, counted altogether. According to a report of tax for the Russian domiciled production companies, for the past three years between 60% and 100% of these units’ profits paid zero tax. Bottom-line profit for the Rusagro group in 2014 was Rb20.2 billion ($523 million); Rb23.7 billion ($386 million). At least one profit dollar, maybe two in five originated from the state budget.

The war in Ukraine, sanctions and counter-sanctions have been both good and bad for RusAgro’s business, the April prospectus acknowledges. On the one hand, “we also benefit from an annual import quota of pork (of 430 thousand tons of pork) and high import duties for out of quota imports as well as a ban on import of live pigs from the EU and meat from the US due to veterinary rulings and as counter sanctions measures. Any modification or failure by the Russian Government to continue its policy of regulating the domestic sugar market or meat market through the existing import tariffs system or failure to extend it in the future may open our markets to increased foreign competition and may have a material adverse effect on our business, results of operations and financial condition.”

On the other hand, sanctions against Bank Rossiya, Sberbank, and Gazprombank, the biggest lenders to Rusagro, “ have increased the cost of capital in Russia and have contributed to the rise of interest rates in Russia over the past year.”

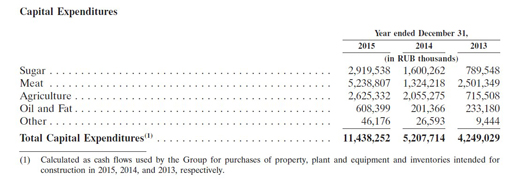

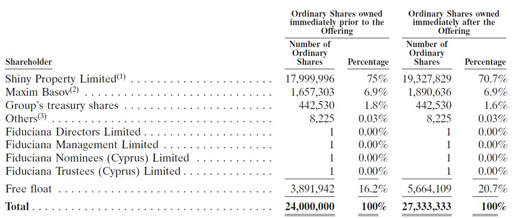

The SPO and share sale in April was intended to raise $245 million, net of bank fees and placement charges. Of this sum, the company says Moshkovich subscribed $99.6 million, and his chief executive, Maxim Basov (right), $17.5 million. The money was reportedly targeted to be spent on starting up meat and greenhouse vegetable production; purchase of more farm land; and unidentied asset acquisitions. Moshkovoich reportedly retains “significant discretion over the use of net proceeds.” Sugar trails other product lines in the capital spending of the group in recent years.

The SPO and share sale in April was intended to raise $245 million, net of bank fees and placement charges. Of this sum, the company says Moshkovich subscribed $99.6 million, and his chief executive, Maxim Basov (right), $17.5 million. The money was reportedly targeted to be spent on starting up meat and greenhouse vegetable production; purchase of more farm land; and unidentied asset acquisitions. Moshkovoich reportedly retains “significant discretion over the use of net proceeds.” Sugar trails other product lines in the capital spending of the group in recent years.

Source: prospectus, page 58: http://www.rusagrogroup.ru/fileadmin/files/prospectus/IM_final.PDF

Rusagro’s move away from sugar has meant there is a progressively weaker correlation between the company’s share price and the international price of sugar.

ONE-YEAR TRAJECTORY OF THE RUSAGRO SHARE PRICE COMPARED TO SUGAR

Key: yellow=share price, blue=sugar

Source: http://www.bloomberg.com/quote/AGRO:LI

What took place on April 29 was not triggered by bad news from the sugar sector. On that day the share price went from above $15 to $14.33, and kept going down to $12.32 on May 25. It has since pulled back up to $15. This is still well below the March peak of $17.99. That is also the historical peak for Rusagro since the IPO in April 2011. Current market capitalization of the company at $15 per share is just over $2 billion.

FIVE-YEAR TRAJECTORY FOR THE RUSAGRO SHARE PRICE, SHOWING TRADING PEAKS

Source: http://www.bloomberg.com/quote/AGRO:LI

Market sources in Moscow report there was anticipation from the start of this April that, as a result of pork, grain and seed-oil price movements on the Russian market, the company’s profit and earnings results for the first quarter were going to be relatively weak, though the sugar result was expected to be strong.

This is how the results turned out, according to the company release on May 20: “Ros Agro Q1 2016 performance was mixed. Sugar and agricultural businesses continued to work at high margin increasing revenue and EBITDA. Meat business results have suffered from lower meat price, higher grain prices and launch costs of slaughterhouse. Oil and fat business suffered from rouble appreciation, difficulties at major export markets and deficit of raw material.”

Source: http://www.rusagrogroup.ru/fileadmin/files/reports/en/pdf/Press_release_-_03M_2016.pdf

But look what had happened three weeks earlier, on April 29. The chart shows on that day almost 5 million shares were sold, causing the share price trajectory to continue downwards, making the trend more pronounced. That volume of selling was the single largest on record for the past five years of Rusagro’s London listing. Only twice before was the volume of selling just above 2 million shares for the day – September 2012 and April 2015. This year’s selloff, however, was more than double the previous records. Assuming an average sale price of $14.50, the share dump realized proceeds of about $71 million.

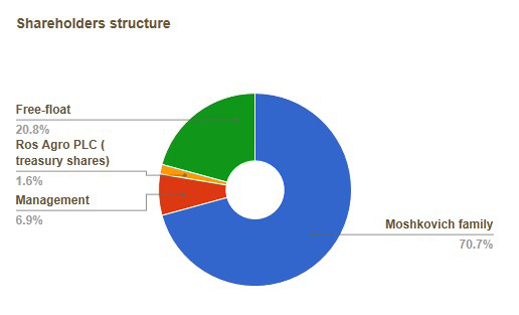

According to the company it has 137 million shares in circulation. This is how Rusagro reports its shareholdings today:

Source: http://www.rusagrogroup.ru/investors/shares/

Before the SPO in the middle of April, the stake of Moshkovich had been larger. The outcome of the SPO was that Moshkovich’s stake was reduced by 4.3 percentage points, and the company’s treasury stake by 0.2 points. Correspondingly, the free float expanded by 4.5 points. The company’s subsequent presentation to the market indicates that institutions took just over half the new issue; one-third of the issue, hedge funds looking for short-term gains.

Source: page 142 -- http://www.rusagrogroup.ru/fileadmin/files/prospectus/IM_final.PDF

Was someone with inside knowledge of the company’s first-quarter financials selling before the bad news became public? Was Moshkovich selling shares for $71 million in order to recoup most of his $99.6 million outlay in the SPO? Were there other sellers whose identities are masked behind the Moshkovich name and the BVI entity called Shiny?

RusAgro’s investment director and spokesman, Sergei Tribunsky, says “interpreting the indicators in such a short period of time is like reading tea leaves.” He cannot explain why the share price fell sharply in April, or who was selling. Moshkovich was asked whether an entity associated with him or his family members or business associates, or a company, agent or trust receiving his direction and in which he has a beneficial interest, was a seller of Ros Agro shares on April 29? He has not replied.

Anastasia Tikhonova is the sugar sector analyst at Renaissance Capital in Moscow. “The falling share price,” she says, is “associated with a number of factors — first of all, the recent SPO. This saw the announcement of an increase of the investment program to begin the development of new businesses, such as greenhouses, and potential M & A transactions. Companies do not always disclose these things in the early stages, as this may cause uncertainty among investors, and some overreaction. Also, the first-quarter results showed complications in the meat business due to a significant fall in pork prices, as well as increased costs from the launch of beef production.” Regarding the question of insider dealing, Tikhonova and other analysts say they cannot comment.

Leave a Reply