By John Helmer, Moscow

Alrosa, Russia’s state diamond monopoly, will be ready to hold an initial public offering (IPO) by late 2011 for a 20% stake in the company, Alrosa’s chief executive Fyodor Andreyev said cryptically on the sidelines of a Moscow investor conference on Wednesday. But will international investors be ready to buy shares of Alrosa by then, and at what discount to the share value of Alrosa’s global mining peers?

If there are hesitations on the part of the underwriters and the regulators in London, can Alrosa pass muster on the Hong Kong Stock Exchange without undergoing the heavy discounting and disclaimer process which curtailed the IPO performance in Hong Kong last year of aluminium monopoly Rusal and junior iron-ore miner, IRC?

Andreyev, according to his spokesman, schedules just one press interview a year, and he has not made up his mind when this year’s one will take place. The Alrosa board chairman is Finance Minister Alexei Kudrin, who is much too busy to speak in detail on Alrosa’s business.

The 15-man company board has no non-Russians, and not a single figure with career experience in mining, or in running a public shareholding company. Three seats are occupied by Russian creditor banks – state banks VTB and VEB, and the Moscow commercial bank Nomos, controlled by Alexander Nesis. The only Alrosa board member with experience in the diamond business lacks international experience — Vladimir Rybkin, head of the state stockpile agency, Gokhran.

Andreyev was asked today whether changes to the Alrosa board are being considered as part of the company’s preparation for its IPO. In particular, he was asked, is Alrosa planning to follow Nord Gold and other Russian companies to select an international figure well-known in the mining investment markets to pilot the company through its stock exchange tests? Nord Gold’s IPO, currently under way in London, is led by a South African, the former Anglo American executive, Philip Baum.

He replied through a spokesman with a hint that consideration has started, but he won’t be the decision-maker: “It’s the shareholders who appoint the supervisory board members, not the company itself.” As for an international appointment, “same thing here, it’s up to the shareholders and the board itself, not to the company.” And he added: “There has been no decision on the IPO yet. We said that the company opening would give us a potential opportunity to hold an IPO, and we gave our forecast for the share listing — about 20%, which can bring the company about $2 billion. That’s all. The banks and the auditors will be appointed after there is a final decision.”

Even if the Russian state banks agree to anchor the share sale – as VEB, VTB and Sberbank agreed to do for Rusal in Hong Kong a year ago — navigating the company through the regulatory shoals is a tall order. For the time being, the company’s releases on its diamond reserves; mine output; inventories and stockpiles; underground mining costs; marketing schemes; the sale prices it realizes for its goods; and internal management all lag behind the disclosure standard which is followed by Russian companies issuing share sale prospectuses in the international markets. Even for some of the world’s largest Indian, Israeli and American diamantaires, who buy diamonds regularly from Alrosa for cutting and polishing, they concede the process is notoriously slow, complicated, tricky — anything but transparent.

The latest Alrosa presentation to the financial markets was in October, when JP Morgan, UBS and VTB arranged a 10-year bond issue for $1 billion. That document raised a number of questions about the company’s cashflows, obligations, and costs which have yet to be answered. On November 3, the company announced the placement had been successfully completed, paying a coupon rate of 7.75%.

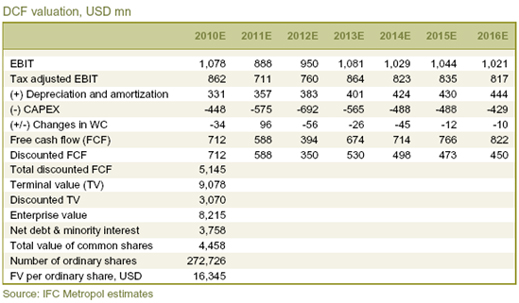

A semi-authorized promotion the previous month by the Metropol brokerage of Moscow set a target valuation of the company’s shares at $16,345 per share, equivalent to almost $5 billion in market capitalization. Metropol’s valuation analysis, written by Andrey Lobazov, set an enterprise value (EV) for Alrosa at $8.2 billion, and after subtracting net debt and minority interests amounting to $3.8 billion, arrived at the notional market capitalization, before privatization and IPO, of $4.5 billion.

But Metropol’s enthusiasm was tempered. Its projection of Alrosa’s earnings shows declines for 2011 and 2012, and no improvement above the 2010 level before 2017 at the earliest. When the company’s capital spending requirements for its costly, risky underground mines are added to the calculation, this table looks tilted negatively for the post-IPO share price:

According to Andreyev’s only public remark on valuation, “the company was valued at between $8 billion-$10 billion.”

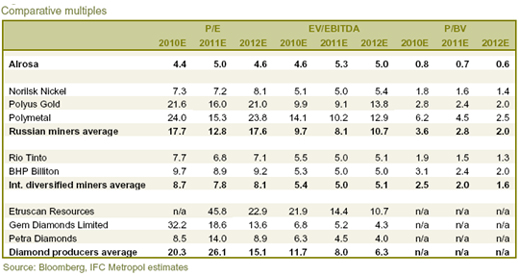

Metropol was cautious, but hopeful that the company’s disclosures will improve this year. “Alrosa trades at a significant discount to small diamond producers and to Russian and international diversified miners. Alrosa is an unlisted private company with low trading liquidity, low transparency and weak corporate governance, so this discount is not a surprise.

However, this underlines the share price growth potential as the company moves towards an IPO. It is reasonable to expect that transparency and corporate governance will improve, narrowing the current discount to peers.”

This is how Metropol ranked Alrosa against its peers on three standard valuation metrics:

Metropol also recommended the sale of a stake in Alrosa’s subsidiary Severalmaz to reduce the financial drag the diamond-mining project in the northwestern Arkhangelsk region is having on the parent company. “If a stake can be sold in Severalmaz,” Lobazov of Metropol reported on September 8, “ we believe the news could cause Alrosa’s shares to appreciate. The sale would simultaneously provide financing for factory construction and the future development of Severalmaz, while demonstrating that major players are confident in the successful implementation of Alrosa’s long-term plans for its subsidiary.”

That was a hint at the negotiations between Alrosa and Rio Tinto for the latter to take operational control of Severalmaz and its Lomonosov diamond field, and to invest the capital required to start a new mine. These talks are continuing, as Rio Tinto tries to address the licensing and cost problems, as well as other risks which bedevilled the ill-fated joint venture of 2008 between De Beers and LUKoil for a mine at the nearby Grib diamond deposit.

For prospective Alrosa shareholders to gather reassurance from a Rio Tinto deal would, however, require more disclosure from Alrosa than it has ever provided about one of its diamond mines. The standard in this case was set by Archangel Diamond Corporation’s 155-page NI-43-101 report on the Grib project, issued in April of 2008. Alrosa has not demonstrated its readiness to go so far.

The next meeting of the Alrosa board is scheduled for February 22. That is expected to fix the a date for a meeting of the federal and Sakha government shareholders to approve amendments to the company’s charter which will clear the way to an IPO. While that meeting is a formality, it will take time first for Kudrin and the President of the Sakha Republic, Yegor Borisov, to agree on the small print. The deadline is mid-April. After that, according to another of Andreyev’s hints, a tender may be launched by Alrosa for mandates to underwrite the IPO. The only certainty about the outcome of that is that VTB, the state bank to which Alrosa is most beholden, will be included.

| For the record, according to the latest public release by the company on January 17: “In 2010 ALROSA sold a total of over USD 3.483 billion worth of rough and polished diamonds. Based on the world diamond market outlook for 2011, ALROSA plans to sell USD 3.5 billion this year. The key objectives for the Company in 2011 have been set out as follows: full-scale implementation of the underground mine construction program in order to enable the already in operation underground mines of Mir and Aikhal to reach design capacity; approving the Company’s development strategy for the period until 2018, adjusted for the implementation of the Timir iron ore project and major development guidelines up to 2030 providing for introducing into industrial production mines with a lower diamond grade; finalizing work to comply with the resolution of the shareholders of ALROSA on its conversion into an open joint-stock company.” |  |

Leave a Reply