By John Helmer, Moscow

Mother Hubbard, one of the most popular old English nursery rhymes, was a hard-luck case. Her kindliness and generosity were ruthlessly exploited by her conniving dog, who played dead for sympathy and then took her for everything she was worth.

Mother Merrill, 40-year old nickname for the bank now owned by Bank of America, is one of United Company Rusal’s major creditors, having led the syndicate which in early 2008 loaned $4.5 billion which Oleg Deripaska used to pay Mikhail Prokhorov part of the cash requirement for the sale and purchase of a 25% stake in Norilsk Nickel and a 14% stake in RusaL (expanded to 19% before Rusal’s IPO, 17% after).

Mother Merrill is a signatory of the agreement which kept Rusal from insolvency in 2008 and 2009, and a bookrunner for the Rusal share sale a year ago. So, when the old dame issues a series of forecasts for Rusal’s future value, it carries more than the usual amount of weight. What Mother Merrill is now saying is that the dog is about is get much richer – Rusal should, and will, sell its stake in Norilsk Nickel back to the company for a price of at least $15 billion, with the outcome that by the end of next year, a debt-free Rusal may have accumulated a cash surplus of $9.5 billion.

Here’s the report.

“If such a deal materialises,” Merrill’s analysts, Jason Fairclough and Eduard Faritov, argue, “it would instantly deleverage Rusal eliminating net debt ($12bn). This could have important implications in terms of relative rerating towards other aluminium players, potential to reactivate dormant growth projects & restarting dividend payments. For Norilsk, we think shares might appreciate on the reduced number of shares and buying by non-EM funds, who, in our opinion, may have stayed away till now due to the large shareholder conflict.”

The pluses and minues add up this way: Rusal’s return of the shares to Norilsk Nickel at a premium sale price of between $15 billion to $16 billion will add to Norilsk Nickel’s debt, and cut its income. By the end of 2012, net debt may be at $3.8 billion, compared with net cash of $4.5 billion now. But the lifting of Deripaska’s siege would trigger a share price advance. According to the report, the share price target would jump from $304 to $323 – a gain of 7%. That is up 29% on the present share price of $251.

In lockstep, Rusal would suffer a loss of net income, because Norilsk Nickel would no longer be paying dividends and Norilsk Nickel’s share price gain would not be added to Rusal’s asset value. But by the end of 2012, instead of a forecast debt level of $4.3 billion, Rusal would be swimming in cash — $9.5 billion. This, plus the likelihood that Rusal would start paying its shareholders dividends, should trigger a takeoff in Rusal’s share valuation. Merrill’s target price would go to HK14.30 – that is 17% better than the current share price of HK$12.24.

Investment fund managers in the London and Hong Kong markets are being urged to change their minds. Instead of viewing Rusal as a proxy (as well as a hedge) for the value of aluminium – going up and down with the metal price – the idea is that if the Rusal sale goes through, the market demand for both Rusal and Norilsk Nickel shares will jump. The market perception that Deripaska is toxic for corporate accountability and share value , which has so far hobbled Rusal in comparison with its international aluminium producing peers, should evaporate. “We think that removing the perception of “too much” leverage, and corporate governance concerns related to ongoing disputes with Interros & putting growth back into the business could result in a major rerating. Alcoa and Chalco trade on 12.5 and 25x 2011E PER (Bloomberg consensus), while Rusal ex-Norilsk would trade on about 8x.”

According to Mother Merrill, instead of one fearful Russian metals champion and a dog on a crutch, there will be two out-performers.

The evidence that this forecast is shared by others in the market is that Rusal’s share price has recently unlocked from the movement of the price of aluminium metal. Its recent upward momentum suggests the expectation that it will sell the 25% stake to Norilsk Nickel:

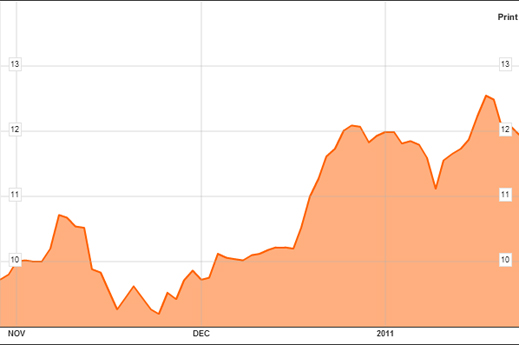

Rusal 3-month share price:

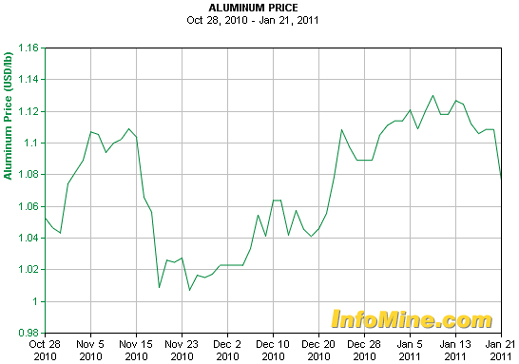

Aluminium 3-month price:

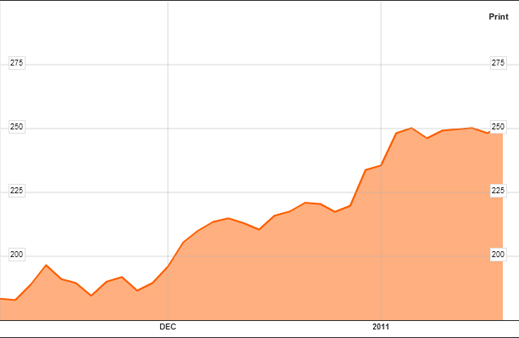

Norilsk Nickel is now at $251, up 34% over the three months:

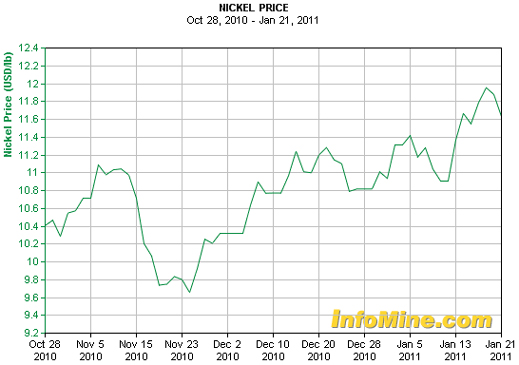

Nickel 3-month price:

The poltics of what is happening are less clear – but not less certain.

In a stratagem to accumulate shares and votes to counter Deripaska’s attempts to knock out board members, Norilsk Nickel has been attempting to buy back its shares from international investors. But they have been decidedly reluctant to sell at the current price, figuring if they are patient, the share price will gain significantly.

Market sources say that the Interros group of Vladimir Potanin has been selling shares to the company, reducing its stake from about 30% to 25%, but accumulating a profit of more than 30% since November, as the price has gone from $181 to $251. The buyback of shares will no longer be necessary, however, if Rusal accepts the new offer for the 25% stake, and sells in advance of the March 11 date scheduled for a new vote on the Norilsk Nickel board of directors.

The Merrill report speculates that if and when the Rusal sale goes through, Norilsk Nickel will decide to cancel the shares. The report calculates that that would enhance the Interros (Potanin) stake in Norilsk Nickel from 25% to as much as 38%. There is no sign, however, that this is what chief executive Vladimir Strzhalkovsky and the Russian government intend. If the 25% is retained in the hands of the company, or a state bank, and not in Potanin’s, the latter’s grip on the company will remain subordinate to the state’s.

That leaves Rusal and its boss with the question Mother Merrill and her dog are also asking – what will happen to Rusal’s $9.5 billion surplus?

This is also the question for Michael Cherney (Mikhail Chernoy). For his case against Deripaska to return his original 13% stake in Rusal continues to accumulate new evidence and expert testimony each month, as the lawyers prepare for trial scheduled in the UK High Court in just over twelve months’ time.

Deripaska has had no cash with which to do what he has always done when he has been confronted by proven claims in international courts – that is, pay up. Naturally, as Rusal grows in market capitalization, Deripaska’s obligation to Cherney grows concomitantly. Starting at $3.1 billion – Cherney’s 13% contract stake in Rusal at current market value – plus dividends owing, share of asset sales, related claims, legal costs, a decade of bank interest, and a control premium. Altogether, they add up to between $5 billion and $6 billion. It’s the price Rusal must pay to preserve Deripaska in his seat. The company did no less to enable Deripaska to buy off his last shareholding challenger – Roman Abramovich in 2000-2002.

That’s roughly half the cash pile Merrill’s calculates will be available. Deripaska will be a rich man again, but no longer at the expense of those who put him in business. Potanin’s riches will be more secure, but his power less; while the Russian state stakeholders will be both richer and more powerful than ever before over the two oligarchs. All the dogs, it seems, will have their day.

Leave a Reply