By John Helmer, Moscow

The Pelaco shirt company was a feature of my childhood for an advertising slogan that was so original, it hardly made sense. The idea was that if a native Australian, speaking pidgin English, recommended a Pelaco shirt because it fitted him so well, his recommendation would be credible to white shirt-wearers – even if the aboriginal didn’t wear trousers, and was therefore unlikely to acquire a Pelaco shirt in the first place, let alone a pair of Pelaco pyjamas. In short, the selling-point was preposterous. But fifty years later, the ad slogan is still memorable.

Oleg Tinkov, 45 years old, has the name and the style of advertising which have made him memorable, briefly, on the London roadshow circuit. His idea was that in a market which deeply devalues Russian banks, especially the state-owned ones; and suspects the short-term prospects of the commercial ones are getting poorer by the day, Tinkov would disguise his bank as if it were a credit card payment system, and promote his shares to the market fad for internet payment system companies like Luxoft and Qiwi. The stories of the latter share listings in the New York market can be read here and here. They aren’t banks at all, though in due course they may be threatened by Russian raiders who are banks. Since their initial public offerings (IPO) in June and September, Luxoft is up 71% and now has a market capitalization of $966 million; Qiwi is up 32%, with a market cap of $2.2 billion.

The Tinkoff underwriters – Goldman Sachs, Morgan Stanley, JP Morgan, Renaissance Capital, and Sberbank – went along with the bank-in-disguise scheme. Together, they withheld from public review two versions of the TCS Group Holding Plc (Tinkoff Credit Systems) prospectus – the first was dated October 14, the second October 22. In London Tinkov made a display of waving his arms as he dismissed questions from sceptical fund analysts. The outcome was the appearance of high demand for the TCS share at the top of the target range, $17.50, followed by a collapse of the share price since the IPO commenced on October 21. From $17.50 it went to $19, and it is now $17. Market cap started at $3.2 billion; it is now $3.08 billion, with shorters now speculating on a continuing decline.

Goldman Sachs demonstrated it wasn’t fooled by the prospects of the bank-in-disguise. One in five of the 62 million shares disposed of in the initial public offering was sold by Goldman Sachs, as it reduced its 12.3% stake down to 4.5%, collecting $226 million. Tinkov himself , who started with a 60.5% shareholding divided between five offshore front companies, sold almost as many shares as Goldman, ending up with 50.9%. His take was just over $200 million. The other stakeholders who bailed out were Vostok Nafta (Sweden), down from 13.2% to 4.8%; Baring Vostok (Russia, Guernsey), down from 7.9% to 2.9%, and Horizon Capital (US, Ukraine), down from 4% to 1.5%.

But you must hit the magnifying button on the chart that follows in order to understand Tinkov’s clever scheme to fit – er, himself.

But you must hit the magnifying button on the chart that follows in order to understand Tinkov’s clever scheme to fit – er, himself.

According to the prospectus, Tinkov has created a dual shareholding scheme, according to which Class A shares carry one vote at shareholder meetings, and Class B shares carry 10 votes. The shares sold to the London market were all of Class A; after the IPO Tinkov held on to all – repeat all – of the Class B shares.

The tabulation of who was selling out and of the shareholding distribution after the IPO are blanked out on page 140 of the October 14 version of the Tinkoff prospectus, although the information the table contains had been decided long beforehand. If you relied on Tinkov’s early-bird version, you might think he held just 60.5% of the shareholding control. Here is the table, according to the prospectus of October 22.

HOW OLEG TINKOV, GOLDMAN SACHS ET AL. ARRANGED A SHARE SALE TO TAKE CASH FROM THE MARKET AND INCREASE TINKOV’S CONTROL OF THE ER, BANK – click to enlarge

Source: Prospectus of October 22, 2013, page 140

Tinkov thus started with 60.5% of the share capital of TCS; put cash in his pocket of $200,025,000, and ended up with 91.2% of the shareholder votes. Tinkov’s voting-share control stake in TCS is the largest and most concentrated among Russian companies listed on the London and New York stock exchanges.

The free-floating shareholders who have just bought into TCS control just 7.1% of the votes. Promotional media reports in Bloomberg and and other media, which missed the small print of the second prospectus, also missed the risk on page 20: “The Issuer’s dual share capital structure, combined with the concentration of voting rights, will result in the control of the Issuer by Mr Tinkov, whose interests may conflict with those of holders of GDRs. The Issuer’s Class A Shares represented by GDRs are each entitled to one vote per share at shareholders’ meeting, whereas the Issuer’s Class B Shares ultimately controlled by Mr Tinkov are entitled to 10 votes per share at shareholders’ meetings. Accordingly, Mr Tinkov, will control the Issuer for the foreseeable future… The voting power of Mr Tinkov will be substantially greater than his economic interest in the Issuer, and the ability of GDR holders to influence the conduct of the Issuer will be limited.”

A similar dual-share scheme has been tried by the two US-listed Russian payment system companies, Luxoft and Qiwi.

If Tinkov was as confident in his self-promotion as the prospectus claims, he might have felt just as secure with a larger free-float and a smaller control stake than 91.2%. According to the prospectus, “TCS’s brand recognition is very strong due to the high profile persona of its founding shareholder Mr Tinkov, from whose last name the brand originates. The name ‘Tinkoff’ is associated with Mr Tinkov’s well-known entrepreneurial activity that has given birth to a number of successful businesses and brands in Russia, including beer, restaurants and frozen foods. TCS’s marketing and public relations divisions are highly attuned to the latest consumer and online trends and use new communication channels, including its website (www.tcsbank.ru) and social networks (Livejournal.com, Twitter.com, Facebook.com, Odnoklassniki.ru and Vkontakte.ru) to further enhance TCS’s brand recognition. According to Livejournal.com, Mr Tinkov’s personal blog is one of the most read Russian blogs, which provides TCS with another popular channel to promote itself.”

In short, Tinkov is a merchant to the twenty-one somethings — that large demographic segment of the credit card market with relatively low income, short credit record, and little security. The prospectus claims that so far this year TCS has approved 33% of the credit card applications it has received; last year the approval rate was 37%. The data released by TCS don’t exactly reveal the distribution of cards by age or by age and gender brackets. Instead, the prospectus lumps all card holders together to produce an average age of “customers” – this seems to mean approved card applicants – of 37 among those who got their cards from internet or telephone platforms; 40 among those who applied by mail or through agents.

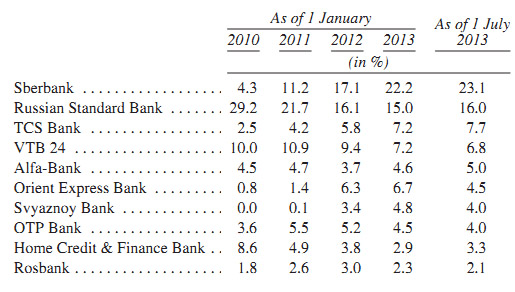

Not counting delinquent credit card debtors, TCS appears to be holding third place in the Russian credit card market with a 7.7% market share. As the tabulation shows, TCS has been growing much faster than most of its rivals, except for Sberbank, which dominates the market with a 23.1% share. Russian Standard Bank and VTB have both been losing ground.

RUSSIAN MARKET SHARES FOR MAJOR CREDIT CARD ISSUERS

TCS counts a total of Rb49 ($1.5 billion) billion in current credit loans, just ahead of VTB 24 and Alfa Bank, but far behind Sberbank’s credit card loan total of Rb149 billion ($4.7 billion), and Russian Standard Bank with Rb101 billion ($3.2 billion).

The financial reports in the prospectus also reveal that it is getting much more costly for TCS to acquire new customers. In the first six months of 2012, this expense item came to $46.8 million. In the comparable period of this year, it had jumped 47% to $68.9 million. Compared to what it cost TCS to find new credit card customers in 2010, the cost has grown fourfold – and it is the single largest cost item on TCS’s operating balance sheet. The company reverses the meaning of this number, claiming that because TCS doesn’t need a conventional bank branch network, and because a growing proportion of customers interact with TCS online, the customer acquisition costs are falling “as a proportion of net interest income due to the economy of scale effects arising from the rapid growth in the size of TCS’s credit card loan portfolio.”

If the concentration of control in a figure like Tinkov hasn’t proved to be a debating point so far in the marketplace, the risk that TCS would begin suffering from the growing inability of its cardholders to pay their unsecured debts has been recognized.

Natalia Berezina, the banking sector analyst at Uralsib Bank, started immediately after TCS’s IPO intention was announced by pointing out that as the third largest credit-card issuer in the Russian market, TCS is vulnerable to the deterioration of general economic conditions in Russia and the likelihood of rising loan loss and credit card debt defaults by Russian consumers.

“The bank notably differs from existing public stories which are all universal banks with a dominant share of corporate business and little or no 2013E earnings growth (apart from Bank St Petersburg). TCS, in contrast, is an exclusively retail bank, with 97% of its loan portfolio in credit cards. The bank’s net income rose 78% YoY in 2012 and 52% YoY in 1H13, while ROAE [Return on Average Equity] stood at 59% and 49%.”

“The bank notably differs from existing public stories which are all universal banks with a dominant share of corporate business and little or no 2013E earnings growth (apart from Bank St Petersburg). TCS, in contrast, is an exclusively retail bank, with 97% of its loan portfolio in credit cards. The bank’s net income rose 78% YoY in 2012 and 52% YoY in 1H13, while ROAE [Return on Average Equity] stood at 59% and 49%.”

Berezina noted that the price/earnings ratio and other measures of Russian bank value appeared to be giving Tinkov a better rating than sovereign-backed state-owned banks like Sberbank and VTB. “The high-growth profile justifies different multiples compared to the 0.4-1.1 2013E P/BV range that Russian banks are currently trading in, but we do not see levels above a 2013E P/BV of 2.5-2.6 (pre-money) as fair for TCS, assuming the 2013E ROAE stays slightly short of 50%. But pricing may be much more ambitious. Vedomosti reported today that the bank is valued at $2.5-3 bln for the deal, or at 9.6-11.5 on 2014E P/E. This is probably a post-money assessment, which we estimate equals a post-money 2014E P/BV of 2.6-3.3 or a 2013E P/BV of 3.6-4.6…We see such levels as slightly stretched despite the bank’s notable business and earnings growth, as they seem to underestimate the underlying risks of an undiversified product mix.”

In a full report issued on October 8, Berezina and Uralsib Bank warned that a fair valuation of TCS should be $1.3 billion. The top-of-the-range IPO target, and also the price at which TCS began selling its shares, put TCS’s market capitalization over $3 billion. The IPO valued TCS at 4 to 5 times book value, while Sberbank trades at about 1.3 times book value.

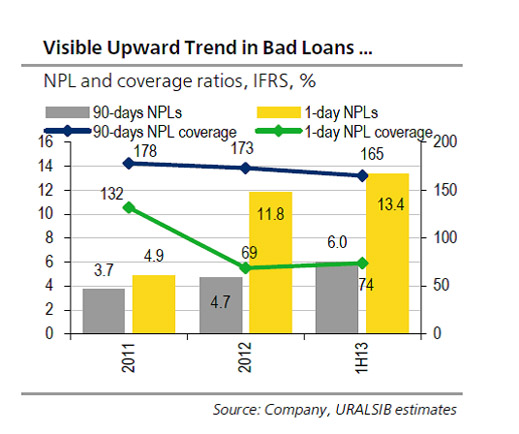

This can’t last. Indeed, according to the Uralsib Bank report, the question has to be asked — how was it possible that the first and second-day share-buyers of TCS failed to appreciate what was already obvious – rising Russian consumer debt, weakening income growth, growing non-performing loan (NPL) aggregates, and dwindling bank funds available to cover them. “The absence of diversification in TCS’s business speaks for the fact that it should be among the ones most sensitive to these trends. 90-day NPLs rose from 3.7% in 2011 to 4.7% in 2012 and to 6% in 1H13, while in one-day NPLs the trend is even more pronounced (from 4.9% in 2011 to 11.8% in 2012 and to 13.4% in 1H13). The ratios could have been even higher if the bank [TCS] had not sold some bad debt (2% of its portfolio) in 1H13.”

The conclusion, according to Berezina and other analysts, is that TCS is no punt on Tinkov’s entrepreneurial skill at selling beer, ravioli, pop music, bicycle racing, or advertising. Rather, it’s an experiment in how the market judges the growth of the Russian economy over the next year or two. In this calculation, the “high profile persona”, as Tinkov refers to himself, is irrelevant. Tinkov has said as much himself. Asked what is the most common mistake entrepreneurs make, he told Venture Village: “Overestimating the market and underestimating costs.”

Berezina again: “So far the equity market has not had a chance to judge the pure unsecured lending story; at the first glance 165% coverage of 90-days NPLs (as of 1H13) looks safe enough but 74% coverage of 1-day NPLs can raise concerns if the economy does not show a pronounced recovery. Sberbank has 1-day consumer NPLs covered by just 47% but this is hardly a good reference point, given the high share of payroll clients; Vozrozhdenie and Bank St Petersburg are not much engaged in consumer lending so far and VTB doesn’t disclose its numbers. So, for now, we treat TCS’s coverage as comfortable, assuming no nasty surprises in macro stats on the retail side going forward.”

As TCS’s share price falls, the nasty surprise is that Tinkov has managed to pass Russian economic risk to a group of public shareholders who can have no say whatever in how TCS is run.

Leave a Reply