By John Helmer, Moscow

In the memoirs of the great courtesans, much fondness is expressed toward the size of their patrons’ pockets, but never the size (or lack of it) of their male members. Morgan Stanley lacks that kind of discretion.

If you read the report issued on February 17 by the investment bank’s Moscow and London branches on Alexei Mordashov’s Nord Gold, the place to start is below the waist, as it were. “In the next 3 months,” runs the small print of the required US regulatory disclosures, “Morgan Stanley expects to receive or intends to seek compensation for investment banking services from…Nordgold…Within the last 12 months, Morgan Stanley has provided or is providing investment banking services to, or has an investment banking client relationship with …Nordgold…Within the last 12 months, Morgan Stanley has either provided or is providing non-investment banking, securities-related services to and/or in the past has entered into an agreement to provide services or has a client relationship with… Nordgold.”

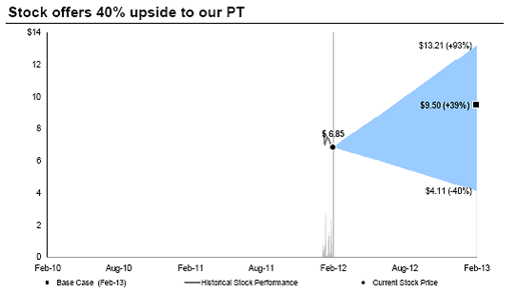

In short, Morgan Stanley is being paid by Nord Gold and its 89.4% owner Mordashov to blow hot and hard on Nord Gold’s asset value and inflate Mordashov’s share price, in order to make him, according to the report, at least 39% richer. Translating Nord Gold’s current share price of $6.85 and market capitalization of $2.46 billion into the Morgan Stanley targets of $9.50 and $3.41 billion, respectively, would fatten Mordashov’s pockets by $857 million.

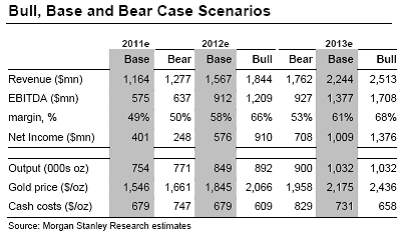

And that’s what the Morgan Stanley analysts, who have signed their names to this exercise – Dmitry Kolomytsyn and Kirill Prudnikov – call their conservative projection (“base case”) between an even higher value forecast (“bull case”) and a much worse one (“bear case”). As can be seen from the tabulations and charts of the eager suitors, everything depends on three variables – the amount of extra gold Nordgold can produce from its mines; the cost increase (or decrease) with which it manages to achieve this; and the price of gold in the market place. At the high point of this exercise (“bull case”), Morgan Stanley gives Mordashov an extra $1.8 billion.

At the low point, his wealth deflates and he will be less loveable by $879million.

Since there is nothing Mordashov and Morgan Stanley can do about the price of gold, this lovers’ tryst depends for its believability on two things – how much gold Nord Gold can claim to lift to the minehead, and how far it can press the costs of mining the gold downwards.

And there, the professional lady of the evening might point out, is the rub.

Nord Gold’s Russian goldmines are mostly owned by the Canadian-listed subsidiary High River Gold (HRG:CN), which Mordashov has spent three years devaluing, as he attempts, unsuccessfully to date, to persuade the minority Canadian shareholders to sell out. That story has been told in titillating detail already. Unconsummated in this tale are Canadian court and regulator rulings on the application of Norwegian minority shareholders in Crew Gold, who charge Mordashov with under-pricing their shares when he acquired them; and an application by HRG minorities to the Yukon Securities Office to investigate a form of insider trading in which allegedly Mordashov is borrowing funds from HRG to give to Nord Gold to finance the purchase of HRG shares. What both shareholder groups are saying is that Mordashov is not believed in the marketplace.

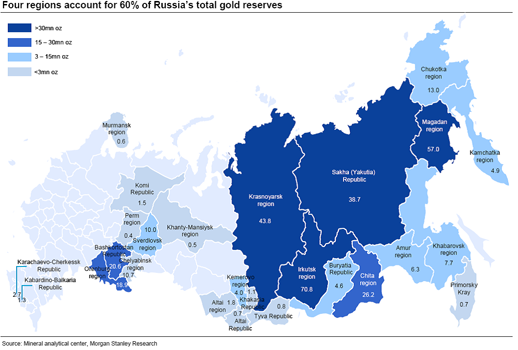

How sensitive is the Morgan Stanley report to that? Start with Morgan Stanley’s handy map of Russia’s gold reserves:

Another way of looking at the map is distinguishing the big unmined reserves from the small producing ones. But that’s where Mordashov’s size disappoints. Not only does the Morgan Stanley report concede that Mordashov doesn’t own anything approaching big in the future of Russian goldmining. But also his current deposits are running swiftly out of gold. Here’s what the report admits: “Based on the most recent reserves audit, Buryatzoloto mines (Irokinda and Zun-Holba) have sufficient resources for only two more years of production.”

Lift the skirt a little, and Morgan Stanley tries to fantasize that “Nordgold plans to convert 7-8mn oz of inferred gold resources to resources in the near term.” The way this will be done may also require a sleight of hand: “Nordgold has hired a special consultant who will transfer non-compliant Buryatzoloto resource base to JORC standards in 2012.”

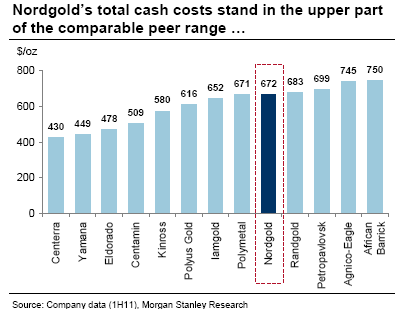

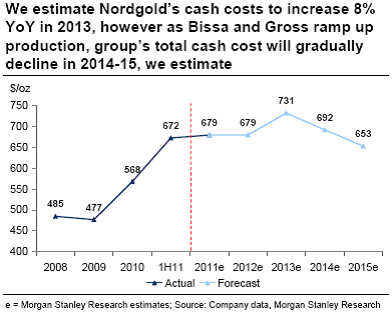

As for costs, the pleasure-seekers at Morgan Stanley admit that at Nord Gold’s recent cost calculation of $672 per ounce, Mordashov’s company is already on the high side of the global goldminer table.

The lads also concede that these costs will continue to grow:

So a different calculation, plus a wait for at least two, possibly three years, is required to make the cost forecast look more attractive, and the upside for the share price more believable:

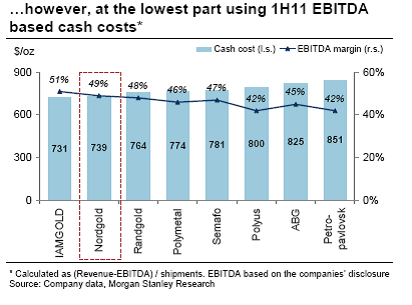

The explanation of this three-variable accounting calculation leaves plenty to be desired: “given the fact that each company in the sector has its specific and unique approach to calculate cash costs, we believe, it is better to compare EBITDA based cash costs… Using this approach Nordgold’s cash costs are the lowest in the sector.”

In other words, potential investors in Nord Gold are invited to place a bet on Mordashov’s managers reversing the 41% increase in costs which they have supervised over the past two years. One of the cost-push factors in the Morgan Stanley forecast is the decline that has been reported in the amount of gold extracted from each tonne of ore mined, or grade. So this warning is far from encouraging: “Investors need to consider the extent to which this cost advantage will diminish as grades decrease and the company depletes reserves and resources, as well as the time period over which this will occur.”

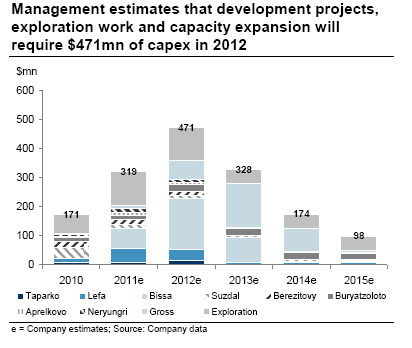

There is one other qualifier the Morgan Stanley report mentions: in order to unlock the target value, an estimated $475 million in new investment must be made in two projects in the next two years. In the aggregate, capital expenditure must more than double this year, and then jump by another 48% the following year.

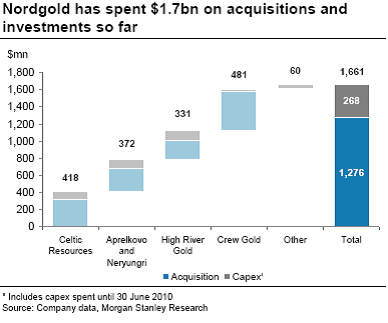

So far Mordashov’s history of investment shows he prefers to overpay for asset acquisitions, and then starve operations for money. According to this chart in the report covering the past five years, Mordashov has spent $1.3 billion on acquisitions, but just $268 million on capital expenditure (capex). That is a record of investing in the stock exchange price of his shares, not a record of investment in goldmining.

According to Chris Charlwood, one of Mordashov’s critics in the Canadian stock market, the real value in Nord Gold is already in HRG, where Mordashov has tried keeping it to himself. “The Morgan Stanley report on Nord Gold indirectly shows that in 2013 HRG will make up approx. 51% of EBITDA, and 48% of production at a cash cost of $646/oz. Compare that with Nord Gold’s cost at its other properties of $816/oz. This will put HRG’s profit and cash flow at significantly higher than 50% of Nord Gold’s total.”

What of the political risks above ground in Africa, where most of Morgan Stanley’s optimism for Nord Gold is located? By all accounts from parallel operations in Mordashov’s iron-ore projects in West Africa, his management troubles have been legion. Accordingly, to one West African miner, he lacks the command and control to assure that mine plan and production targets can be delivered on time and within budget.

What of the risks in Guinea (Conakry), where most of Nord Gold’s current and future gold production is located at the LEFA concession? For the Morgan Stanley projections of increased output, increased reserves, stable grades, and falling costs to come true, Mordashov has to make a political and financial settlement with the embattled president of Guinea, Alpha Conde, and unpopular government ministers facing rising domestic opposition. About that the infatuated Morgan Stanley admits not a word. The only risk the bank detects in Guinea is the weather:

“Rainy season in Guinea. Nordgold failed to achieve its 2011 output guidance at LEFA caused by the heavy rainy season in Guinea. This year Nordgold has optimized the logistics in

Guinea as well as acquired additional pump capacity, grades and dozers.”

One of the Canadian minority shareholders waging the campaign for revaluation of HRG points out that if the Morgan Stanley arithmetic is to be believed, Nord Gold’s share price is trading at a discount of 49% to its peers, but warrants an increase in share price of 39%. “So obviously there is still something wrong, and it can’t be share liquidity because that’s fully under Mordashov’s control. Maybe that’s what is wrong.”

Leave a Reply