By John Helmer, Moscow

The Oradea alumina refinery is a property of Oleg Deripaska’s in Romania. Deripaska (centre image) is the chief executive and controlling shareholder of United Company Rusal, the Russian aluminium monopoly. Deripaska bought Oradea in 2000 over the unanimous objections of the senior management of Rusal in Moscow at the time. The company’s experts warned that Oradea would be too costly to operate, and of insufficient benefit to Rusal for its alumina needs to warrant the expense.

Since then the asset has all but disappeared from the balance-sheets of Deripaska’s holdings. His ownership of the plant is almost invisible in Romania itself. But the refinery is still there, shuttered and unsellable.

According to the Central European Aluminium Company (CEAC), which Deripaska owns through his EN+ holding, Oradea still belongs to CEAC, but “the company…is in the process of being divested from the Group.” Deripaska’s spokesman at Basic Element, one of his Moscow holdings, refuses to say whether Deripaska still owns Oradea or what he has done with it. Noone responds for CEAC. At EN+ spokesman Andrei Petrushinin has promised to clarify the position, but he too remains silent.

The fate of the Romanian asset is under scrutiny today as Deripaska’s management of other non-Russian assets is under review by foreign courts in contested compensation claims. In Montenegro, Deripaska’s Podgorica Aluminium Combine (KAP) has been put into bankruptcy by a local court, on application by the Montenegrin government. KAP is also listed as one of CEAC’s assets, along with Oradea. The fight over KAP is now in the courts of Podgorica and Washington, DC; liability and compensation claims from both sides total more than €1 billion. Click here for the full story.

At the same time in Nigeria, Deripaska and Rusal have lost local court actions to retain their ownership of the Aluminium Smelter Company of Nigeria (Alscon), and are now facing fresh proceedings to enforce the transfer of the asset, and decide $2.8 billion in contested compensation. Rusal lawyers are fighting the Nigerian court judgements in London and Los Angeles. For this story, click.

With $3.3 billion in end-of-year losses for Rusal, gross liabilities of $13.9 billion, and net debt of at least $10.1 billion, Deripaska has so far been unable to convince several international lenders that his management of Rusal will protect the value of the asset collateral securing their loans, and generate enough income to service Rusal’s obligations. A tussle over Rusal’s inability to meet its loan covenants with the banks, led by state-owned China Development Bank (CDB), is turning into a test of Kremlin policy for the future of the near-bankrupt aluminium concern, and of Deripaska.

At the time Deripaska took over Oradea, he told his chief executive at the time, Alexander Bulygin (right), their Russian smelters needed a back-up supply of alumina. That was in case Deripaska failed to hang on to the Nikolaev Alumina Refinery in southeastern Ukraine in the face of rivals. The traditional Soviet-era source for the Russian smelters, the Nikolaev refinery was calibrated to process bauxite from Guinea. The Russian smelters were also calibrated to turn the Nikolaev alumina into aluminium.

At the time Deripaska took over Oradea, he told his chief executive at the time, Alexander Bulygin (right), their Russian smelters needed a back-up supply of alumina. That was in case Deripaska failed to hang on to the Nikolaev Alumina Refinery in southeastern Ukraine in the face of rivals. The traditional Soviet-era source for the Russian smelters, the Nikolaev refinery was calibrated to process bauxite from Guinea. The Russian smelters were also calibrated to turn the Nikolaev alumina into aluminium.

For recognizable but different reasons today, the fate of the Nikolaev lifeline for Rusal is once more in the balance. Three months ago, Deripaska said he was relaxed about Nikolaev because it was in “the safe zone in the south”.

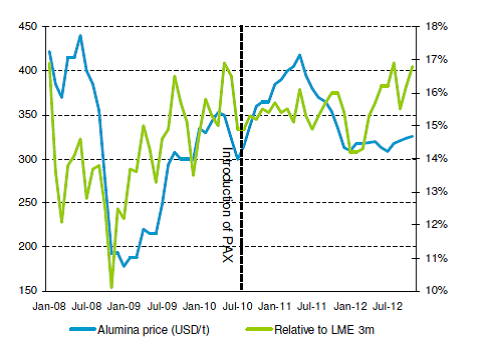

In the period from 1998 to 2000, during the struggle Deripaska was waging to capture the Nikolaev refinery, he also needed Nikolaev to preserve his tenuous hold on the Russian smelters whose operations he shared with partners and rivals including Victor Vekselberg, Mikhail Chernoy, and several others. At that time alumina’s spot price on the global market shot up to between $300 and $400 per tonne.

That was a damagingly high price for a feedstock. For comparison, here is how sharply the spot price for alumina has moved over the past five years:

Source: Hydro Aluminium

At the $400 price level, and given the possibility of a cutoff of supplies from Nikolaev, Rusal scoured the world for alternative sources of alumina. Jamaica was one of the targets. Romania was another. At the time Deripaska made his takeover bid, Oradea had design capacity to produce 400,000 tonnes of alumina per year. At a processing ratio of 4 to 7 tonnes of bauxite to make 1 tonne of alumina, Oradea required at least 1.6 million tonnes of bauxite.

There was an open-cast pit and underground mine for bauxite in the vicinity, producing about 160,000 tonnes per annum. But output there was already declining. Therefore, for the Oradea refinery to meet Rusal’s requirements it required imports of bauxite.

Deripaska was long on bauxite, short on alumina. In the due diligence that was done at the time, Bulygin was advised by his staff that the cost of producing a tonne of alumina at Oradea was above $200. This meant that the viability of the asset in the planned chain of delivering bauxite to Oradea, and taking out alumina for Russia, was dependent on keeping electricity costs in Romania down; and hoping the global price of alternative alumina did not drop below a range of $250 to $300. Bulygin’s staff advised against acquiring Oradea, but Deripaska insisted.

Unluckily for him, the spot price for alumina drifted down over the next several years to $140 for spot, $170-$180 for long-term contracts.

Today a Rusal insider remembers: “It was Deripaska’s own idea to grab as many cheap assets as possible, when everybody in Rusal was against it. Besides, he acquired Oradea on [Mikhail] Chernoy’s money. They were good friends and partners at that time. Deripaska tried many times to revive Oradea. He sent his best staff there, but all in vain — even when the market [price for aluminium] was high before 2008.”

Rusal consolidated its control shareholding of Oradea in May 2000 following privatization of the Romanian state shares. By September of that year, the deal was completed. Cemtrade was the name of the company controlling the refinery and trading its output. First built in 1976, the plant was operating unstably; on occasion barely above care and maintenance. So the takeover price was a song, but the privatization conditions required clearance of plant debts; a $5 million upgrade investment for the plant; job protection for 800 workers; and production targets.

Rusal’s business plan was to deliver imported bauxite to Oradea from the Romanian port of Constanta on the Black Sea, and take out a target volume of 180,000 to 260,000 tonnes of alumina per annum. River transport was to be used between Oradea in the northwest corner of the country, and Constanta in the southeast.

It was planned that vessels carrying the processed alumina would sail east to Russia across the Black Sea; then move north up the Azov Sea and the Volga-Don Canal to the Kama River, and from there to inland Russian smelters. The plan commenced in September 2000. Within twelve months, however, Oradea was losing money.

By then, Rusal had consolidated its hold on Nikolaev in Ukraine, and the threat of a blockade of that source had receded. Global prices for alumina began to fall, as production elsewhere revived. In October 2001, Rusal publicly announced it was halting production at Oradea. At first, this was announced as a temporary measure, intended to strengthen Rusal’s bargaining hand with the Romanian government, which had lifted tariffs for heat, electricity, and local rail transport. Rusal asked the government in Bucharest for tariff cuts and tax relief. Data available from company records show that at the time Cemtrade was paying $2.40 per KWt/hour of electric energy; this compared to $1.08 paid by Rusal’s Achinsk alumina refinery in the Krasnoyarsk region. Before the mid-2001 Romanian tariff hikes, Cemtrade’s monthly costs were accounted by Rusal at $400,000 for heat, and $900,000 for electricity. After the new tariffs took effect, costs jumped 23% to $1.9 million per month.

There was also another cost problem: Oradea’s equipment was so obsolete, its yield of alumina was so low as to require 10% more bauxite input per tonne of output, compared with Rusal’s norm. Rusal found itself paying $100 per tonne more for Oradea input than it could pay for globally sourced supply.

We told you so — the Rusal technicians and middle management told Bulygin. He and Deripaska then thought of retaining Oradea, but consolidating it with other aluminium smelter assets in Romania. That is when Rusal ran into competition from Marco Industries (later renamed Vimetco), and Deripaska into a combination of Marc Rich, Alan Kestenbaum and Vitaly Mashitsky (right). That trio and Marco proved stronger with the Romanian government, which decided to privatize the country’s aluminium smelter company Alro, at Slatina, in their favour. They then picked up Alprom, Romania’s second aluminium smelter, and for the necessary alumina supply they bought out the Turkish owner of Alum Tulcea.

We told you so — the Rusal technicians and middle management told Bulygin. He and Deripaska then thought of retaining Oradea, but consolidating it with other aluminium smelter assets in Romania. That is when Rusal ran into competition from Marco Industries (later renamed Vimetco), and Deripaska into a combination of Marc Rich, Alan Kestenbaum and Vitaly Mashitsky (right). That trio and Marco proved stronger with the Romanian government, which decided to privatize the country’s aluminium smelter company Alro, at Slatina, in their favour. They then picked up Alprom, Romania’s second aluminium smelter, and for the necessary alumina supply they bought out the Turkish owner of Alum Tulcea.

The record of Rusal’s negotiations with the Romanian government in 2001 indicate that it was unable to add assets and build a vertically integrated aluminium business in Romania. Subsequently Mashitsky and Kestenbaum fell out with one another, but not to Deripaska’s advantage. The threat to close Oradea temporarily became a fait accompli – the plant remained closed; and imports of bauxite were halted. By December 2001, the stocks of refined alumina for shipment from the Oradea plant were exhausted. The entire operation was then mothballed.

In August 2007 Mashitsky took the remaining Romanian assets into a London Stock Exchange listing as Vimetco. It peaked in market value at $878 million in 2011, when the Romanian assets turned a profit of about $80 million. They have been loss-making since then. Vimetco’s current market cap is $66 million.

Oradea isn’t mentioned in any Rusal document, not even the initial public offering (IPO) prospectus. That refers to CEAC as “operating an aluminium smelter and bauxite mine in Montenegro”. At that time CEAC was quite clear itself that it owned Oradea in Romania even though it was trying to “divest”. In the Rusal prospectus it is claimed that CEAC was “a geographically isolated producer of aluminium and would not be of interest to the Group due to its high cost structure and certain privatization obligations” — page 303.

The annual reports on the state of the Romanian economy in 2012 and 2013 by the International Monetary Fund (IMF) assemble a catalogue of “missed performance criteria”, debt arrears, insolvency, and unfulfilled promises, but there is no reference to the aluminium sector, dead or alive.

Leave a Reply