By John Helmer, Moscow

Rusal announced on March 9 that its earnings for 2015 were up, and its profit too. But Rusal’s share price, listed on the Hong Kong Stock Exchange, shot downwards by one of the largest one-day falls in months.

Hong Kong Exchange sources say the Rusal share is so illiquid, there is no real market demand, and so there is no response to good news – or to bad. Rusal insiders say the reason for this month’s share price collapse is that Moscow took a two-day holiday on March 7 and 8, and the company’s share operators were still asleep when the price in Hong Kong began to fall. They didn’t wake up in time to stop the decline, as they usually do in the Hong Kong afternoon, Moscow morning. If that sounds like stock price manipulation in violation of the exchange rules, the insider says it is.

Rusal first listed its shares on the Hong Kong Stock Exchange (HKEx) in January of 2010. The starting share price was HK$10.80. The story of the listing can be read here. After arranging a share-support operation with the Russian state banks, and with three pre-selected investors agreeing to lock in their stakes, less than 10% of the public issue was free-floating. After the initial public offering Rusal shares numbered 15.2 billion. The share price peaked at HK$13.38 in March of 2011. It has dropped steadily through several defended price thresholds. It hit its first low of $2.19 in November 2013, and its second low at $2.13 in January of this year. The current share price is 2.79.

SHARE PRICE TRAJECTORY FOR RUSAL SINCE IPO

Source: https://uk.finance.yahoo.com/echarts?s=0486.HK#symbol=0486.HK;range=my

On most days, according to the HKEx data, the volume of shares traded is less than 2 million (0.001%). Since the start of this year, as the bar chart illustrates there have been just four big-volume days. These were January 14 (15.4 million shares traded); January 29 (7.2 million); February 29 (5.8 million); and March 9 (3.7 million):

RUSAL SHARE TURNOVER, DAILY VOLUME SINCE THE START OF THIS YEAR

Source: https://uk.finance.yahoo.com/echarts?s=0486.HK#symbol=0486.HK;range=my

The first of the four trading days caused the price to slide sharply; the second made almost difference to the downward trend; the third triggered a sharp rise; and the fourth had little impact. Over Rusal’s short share history, the big turnover trading days (5-10 million shares) were concentrated in the first two and half years. Since April of 2012 there has been very little buying demand.

According to a company insider, however, there is a pattern to the daily turnover. He says it is share purchase demand created with Rusal company funds and with the intrention to stop the share price falling below targets set by the chief executive and control shareholder, Oleg Deripaska (below).

The source says he follows Rusal shares on a daily basis. “I did notice the unusually

flat activity on those two Russian vacation days [March 7-8]. At normal daily trading the trend is exactly the same every day. When Moscow sleeps the share price goes down, then always goes up between 14:00 and 15:00 in Hong Kong; that’s when it’s 9:00 and 10:00 in Moscow.” The source believes there is proof “the shares are being manipulated from Moscow.”

“Suppose the usual trading volume is about 2 million shares. At the price of HK$ 2.72 per share this volume is equal to HK$ 5.44 million, or US$701,000. That’s not a big volume to manipulate, keeping in mind that only 25% of the volume or less is usually sufficient for this purpose. It must be specifically noted that Rusal’s shares fluctuate mainly against the changes in the aluminium [commodity] market, but also against CHALCO and ALCOA shares. The main question is who exactly is the buyer, or are the buyers, between 14:00 and 18:00 Hong Kong time.”

ONE-YEAR SHARE PRICE TRAJECTORY – RUSAL, CHALCO, AND ALCOA

Yellow=Aluminium Co of China (Chalco); blue=Alcoa; pink=Rusal;

Source: http://www.bloomberg.com/quote/2600:HK

The HKEx says it does not keep an archive of intra-day price share movements for its listed stocks. When each new trading day dawns, the previous day’s graph is erased from the accessible computer records. To track Rusal and the Hong Kong lunchtime-Moscow breakfast effect, it is necessary to make a manual copy of each day’s HKEx graph. This is what it looks like:

RUSAL SHARE PRICE, INTRA-DAY PRICE GRAPH FOR MARCH 10, 2016

Source: https://www.hkex.com.hk/eng/invest/company/intradaychart_page_e.asp?WidCoID=&WidCoAbbName=rusal&Month=1&langcode=e

The Rusal share price is the blue line; the line above is the HKEx index. Watch as the exchange returns from its lunch hour, and Rusal’s Moscow office opens for morning business. A handful of orders totalling less than 300,000 shares arrested the morning decline below $2.67, and revived the price by 3%.

The next day, March 11, follow the blue line against the clock. As Rusal was asleep, someone in Hong Kong executed a relatively large sell order, which cut the price sharply. Once Rusal had woken up to what had happened, in Moscow several much smaller buy orders were placed until the morning commencement price was recovered, and the intra-day losses salvaged.

RUSAL SHARE PRICE, INTRA-DAY PRICE GRAPH FOR MARCH 11, 2016

On Monday of this week, March 14, coffee in Moscow generated a caffeine high in Hong Kong.

RUSAL SHARE PRICE, INTRA-DAY PRICE GRAPH FOR MARCH 14, 2016

Instead of dropping below the $2.68 mark on tiny turnover, several large orders, placed in the 30 minutes between 15:30 and 16:00, gave the share price a kick of almost 5% on the day.

Have others in the market noticed what is happening? Alexei Kalachev, an analyst at Finam in Moscow, says: “Regarding the trading of Rusal shares in Hong Kong, nothing definite can be said. I can only assume that the quotes are supported by one of the market-makers of securities on the stock exchange. This is possible if a corresponding agreement has been concluded with them. However, to find evidence of this in the public domain is impossible.”

“In 2010 when the Rusal paper was first issued in Hong Kong,” Kalachev adds, “the global coordinators of the Rusal issue were BNP Paribas and Credit Suisse. The joint bookrunners were Bank of America-Merrill Lynch, Bank of China International, Nomura, Renaissance Capital, Sberbank, and VTB Capital. In parallel on the MICEX, now the Moscow Exchange, trading in Russian depositary receipts was launched for the shares of Rusal, whose quotes were tied to the price in Hong Kong. Sberbank is the issuer of these depositary receipts. Sberbank has appointed as market-makers to maintain the liquidity of the new instrument, VTB Capital, Renaissance, and Troika Dialog [Sberbank]. Perhaps you can look for someone in these banks who is involved in the share price support.”

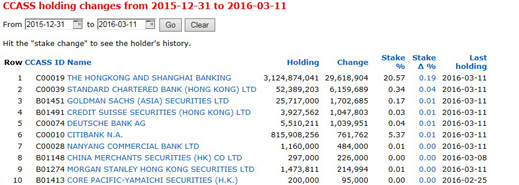

It is possible to take a closer look at who is moving the market in Rusal shares by checking the HKEx data at the market’s Central Clearing and Settlement System (CCASS).

HONG KONG CENTRAL CLEARING & SETTLEMENT SYSTEM – RUSAL SHARE HOLDINGS, JANUARY 1-MARCH 11, 2016

Source: https://webb-site.com/ccass/chldchg.asp?sort=chngdn&issue=5578&d1=2016-01-01&d=2016-03-11

The tabulation indicates that HSBC and Citibank are responsible for most of the share movement changes since the start of this year; HSBC with a holding of 3.1 billion shares and Citi with 815.9 million.

But is Rusal, a Deripaska company or a related entity the beneficial owner giving the banks their buy and sell instructions? Has anyone complained that they may be engaged in share price rigging?

According to a spokesman for Charles Li (below, left), the chief executive of the HKEx, share price manipulation may be happening on the exchange, but it isn’t up to the exchange to record it or investigate. “Hong Kong’s Securities and Futures Ordinance, including its insider dealing sections, are administered by Hong Kong’s Securities and Futures Commission [SFC] rather than the Stock Exchange, which has no access to information about individual investors.” He omitted to mention that the HKEx had exercised regulatory oversight of Rusal until November 2013. It then announced it was transferring the job to the SFC to avoid a conflict of interest when Rusal opened a lawsuit in the UK High Court against the London Metal Exchange, a wholly owned subsidiary of the HKEx. According to the HKEx announcement, “the transfer of regulatory oversight of RUSAL will remain in place while the judicial review is underway.” That case ended more than a year ago; it can be followed here. The disclaimer from Li means the Exchange is reluctant to take back its regulatory power to investigate Rusal.

The head of the SFC, Ashley Alder (right), was asked whether the SFC has received complaints of share-price rigging or SFO Section 296 violations involving the HKEx listed Rusal share; if so, what was the outcome of the complaint or complaints? “We are not in a position to disclose information as to whether any complaints have been made to the SFC,” he replied, “or whether we are investigating any matter.”

Section 296 of the SFC’s rulebook provides: “a person shall not, in Hong Kong or elsewhere-… enter into or carry out, directly or indirectly, any transaction of sale or purchase of securities that does not involve a change in the beneficial ownership of those securities, which has the effect of maintaining, increasing, reducing, stabilizing, or causing fluctuations in, the price of securities traded on a relevant recognized market or by means of authorized automated trading services.”

The Hong Kong market regulator does pursue offences like this from time to time. If found guilty, the culprits usually get off with forfeit of their profits, a fine, and a number of hours of serving soup to the poor of Hong Kong. For the archive of decided cases, read this.

In the rare instance when a Hong Kong company executive has been convicted of manipulating the price of his own stock, he goes to jail. The last of those was Li Jialin, whose company VST Holdings announced he was resigning his post “ due to his personal reasons and unavailability for serving the Company for a period of time.” In fact, he was in jail for six months. He retained his 37.7% of the company shares.

Rusal may be too big in HKEx terms to qualify for investigation or prosecution, according to Howard Winn (right), a well-known Hong Kong journalist. “There have been cases. It happens mostly among the small cap stocks on the exchange. A lot of it goes on among the smaller stocks where certain ‘groups’ own numerous listed companies and they all own shares in each other, usually below the 5% disclosure threshold.”

Rusal may be too big in HKEx terms to qualify for investigation or prosecution, according to Howard Winn (right), a well-known Hong Kong journalist. “There have been cases. It happens mostly among the small cap stocks on the exchange. A lot of it goes on among the smaller stocks where certain ‘groups’ own numerous listed companies and they all own shares in each other, usually below the 5% disclosure threshold.”

The clear implication of the SFC’s prohibition of a retail offer in the IPO,” says David Webb, a leading investigative reporter of the Hong Kong market, “was that it did not consider Rusal as safe enough for retail investors.” Read his report of December 2009 here. Webb recommends caution in assessing the share trading evidence today: “your pattern would also be consistent with a keen Russia-based investor who prefers to buy when he is awake.”

Rusal spokesman Vera Kurochkina refuses to answer questions from this correspondent. Oleg Mukhamedshin, the company’s director for Strategy, Business Development and Financial Markets, declined to comment on the share market evidence. Elsie Leung Oi-Se, a lawyer and non-executive director on the Rusal board, was asked if the board has examined the intra-day trading price movements or other signs of possible price manipulation of Rusal shares. She refused to say.

Leave a Reply