By John Helmer in Moscow

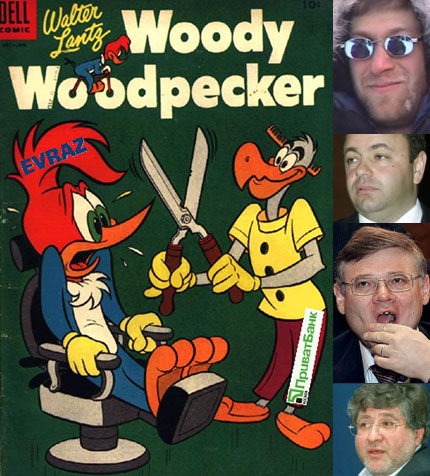

Evraz, Russia’s largest steelmaking and mining group, owned by three Russian oligarchs, continues to wage commercial war against a single Ukrainian oligarch on a Dniepropetrovsk railway track, and through the Evraz group’s Moscow press office. The contest is on home ground for Igor Kolomoisky (bottom image), who went to school in the region; it is going less well for the three Russians – Roman Abramovich and Eugene Shvidler, who live in London, and Alexander Abramov, currently chairman of the Evraz board of directors (top 3 images).

| Although most of the public signals are coming from Evraz public relations chief Alexi Agureyev, the contest is a test for the newly appointed group head of mining at Evraz, Konstantin Lagutin. |  |

Evraz said this week that it may be forced to halt iron-ore production and export shipments from its Ukrainian combine, Sukha Balka, because its access to the railroad, controlled by Kolomoisky’s Privat group, has been halted. The Sukha Balka mine, owned by Evraz since 2007, has come under unusual and personal pressure from Kolomoisky, according to Ukrainian sources — despite the fact that the Privat group earned cash from the two-year old sale of Sukha Balka and other Ukrainian steelmaking assets, plus a seat on the Evraz board and a substantial shareholding in the Evraz group.

When that deal was announced by Evraz in December 2007, in addition to Sukha Balka, the assets included in the takeover were the Dniepropetrovsk Iron and Steel Works, with 1.2 million tonnes of crude steel capacity, and three coking plants. The Evraz announcement at the time claimed the deal “would allow us to increase iron-ore self-sufficiency and …create captive intra-group coke-making demand for the excess production of the company’s coalmines in Siberia.” Counting all forms of iron-ore produced by the group, Sukha Balka contributed 14% in 2008; 10% last year.

No mention was made at the time of the transaction of the transport and logistical lifeline for Sukha Balka. It remains unclear today why Evraz did not make secure provision for access to the existing rail tracks when it bought the mine and processing plant.

Evraz says that peak production at Sukha Balka’s two underground mines was 3.24 million tonnes in 2005, and that most of its deliveries go out by rail; some by sea. Evraz paid $1.06 billion in cash and 4.2 million in Evraz shares to acquire Sukha Balka, according to company releases. Latest reports from the Ukrainian plant indicate that it had to cut its iron-ore output substantially last year. The latest operational report from Evraz indicates that its output of lumping ore from Sukha Balka for 2009 was 1.7 million tonnes, down 38% on 2008, while there was growth in output to 576,000t in the 4th quarter, up 43% on the 3rd quarter.

Much of this iron-ore has gone into inventory, however, and the volume of stocks has swelled, as the rival Krivoi Rog iron-ore plant, owner of the railroad and owned in turn by Kolomoisky’s Privat, stopped Sukha Balka shipments intended for export to European customers.

Exactly what tonnage has been barred from rail shipment since the dispute started is unknown. Alexei Agureyev, Evraz’s vice president for public relations, declines to answer questions about claims he has made to Ukrainian reporters. On February 17, Agureyev was reported as telling Ukrainian media that the rail administration had stopped the shipments “without warning, telephone messages and with letters to the Administration of KZhRK [railroad owned by Privat] demanding resumption of the contractual relationship going unanswered.” Mine and plant production will have to be halted on March 1, Agureyev reportedly threatened in his Ukrainian press statement, and workers put on leave, unless Privat relented.

The published Evraz position is that an unrepaired line break on a rail spur, which has been given as the reason so far for the loading and shipment halt for Sukha Balka cargoes, is a “pretext”, and that Evraz has “tried all possible ways of resolving this conflict.”

Agureyev first went public in Kiev in December with his charges that the Privat group was orchestrating the railroad and other administrative problems for Evraz, which, according to Agureyev, had occurred simultaneously for several branches of Evraz in Ukraine. “Getting control over the iron mines, we do not have access tracks to them, which remained with the previous owner,” Agureyev said in Kiev in December.

At the Krivoy Rog Iron-Ore Combine (KRZhK), a spokesman for the combine’s chief executive Fedor Karamanits told CRU Steel News in December: “The railway by law belongs to KRZhK. We need it for our own ends, and we use it, so we do not recognize the claims by Sukha Balka and we have no obligations in front of them. We own this railway and we need it”. This week, a source at KRZhK added that the obvious solution of the conflict would be for Evraz to build its own rail line. Sukha Balka has tax problems, the source claimed: “they may be attracting attention trying to solve those problems.” The source also said: “Sukha Balka is now building a railroad access of their own”.

A Privat source denies the Evraz allegation that the rail, tax and other problems alleged by Agureyev to be affecting the Evraz group in Ukraine are being orchestrated as part of a hostile move by Privat.

Administration of the region, and of problems affecting industry there, is under the Deputy Governor of Dniepropetrovsk, Victor Sergeyev, and the industrial department of the regional government, headed by Viktor Sergeyev and Andrei Timchuk. They decline to discuss the commercial and other problems Evraz claims it is facing. A report in December by Boris Krasnojenov, steel analyst of Renaissance Capital in Moscow, suggested that the Evraz press tactics were an attempt to diminish the problems by exaggerating the threat.

Today, Krasnojenov reported that now that the Ukrainian presidential election is over, the contest between Evraz’s owners and Kolomoisky may be easier to settle. “The commercial dispute between Evraz and Privat should come as no surprise to the market,” Krasnojenov reports. “We note public statements from both sides that may fuel speculation around the theme. Evraz has a significant footprint in Ukraine but the Ukrainian assets will contribute only 5-6% to Evraz’s consolidated FY10 EBITDA, on our estimates. The commercial disputes between Evraz and Privat may be resolved in the near future, and we think both parties may try to draw the attention of the state authorities to the situation after the presidential election in Ukraine is finalised.”

Leave a Reply