By John Helmer, Moscow

Russia’s misfortunes aren’t exactly sweet for the country’s leading sugar producers, but they can’t complain. On the back of sharply rising sugar prices in January, first-quarter earnings and profits have jumped at the listed sugar producers, and the trend is expected to continue through the second quarter. Prodimex, the leading sugar producer in Russia, isn’t saying so because it’s a private corporation controlled by Igor Khudokormov (lead image, left). He isn’t complaining. In fact, while his sugar business and holdings of farmland grow larger and richer, Russia’s sugar daddy is almost invisible.

In January the deputy director of the Federal Antimonopoly Service (FAS), Andrei Tsyganov (right), called in the sugar bosses, and told them “to act independently on the market and to refrain from coordinating marketing policy, which might lead to a violation of antitrust laws.” Tsyganov’s warning followed reports of regional increases in the sugar price of 30% or more, and a spate of public complaints on the FAS telephone hot-line. A price spike for sugar is normal in January, and the global benchmark rose about 6% in the same period. But the global trend has been sharply downwards since then.

In January the deputy director of the Federal Antimonopoly Service (FAS), Andrei Tsyganov (right), called in the sugar bosses, and told them “to act independently on the market and to refrain from coordinating marketing policy, which might lead to a violation of antitrust laws.” Tsyganov’s warning followed reports of regional increases in the sugar price of 30% or more, and a spate of public complaints on the FAS telephone hot-line. A price spike for sugar is normal in January, and the global benchmark rose about 6% in the same period. But the global trend has been sharply downwards since then.

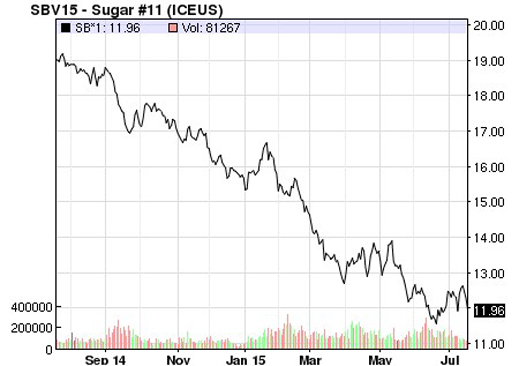

GLOBAL SUGAR PRICE TRAJECTORY, ONE YEAR

(Commodity futures price quote — US cents per pound)

Source: http://www.nasdaq.com

The Russian trajectory for sugar, however, can be seen from the following chart. In January of this year the price was more than double its level in January 2014. Between January and May of this year the price has retreated by 25%, but it is still well above the peaks of the last five years. This is in rouble terms. Because of the sharp devaluation of the rouble last year, however, in US dollar equivalent the price of sugar is growing.

RUSSIAN SUGAR PRICE TRAJECTORY, 2010-2015

(Average price in Rb/kg Moscow)

Source: http://tsenomer.ru/produkti/sahar/

In January the FAS said it was commencing an investigation of four plants and trader distributors in Omsk, Penza, and Kaluga. This week FAS sources said they have completed their investigation of price-rigging. According to Anna Mirochinenko, head of the agriculture sector control department at FAS, the investigation has covered eight cases. Two, in Krasnodar and Penza, have been dropped for lack of evidence. The remaining cases, she said, cover retailers in Altai, Astrakhan, Kemerovo, and Ulyanovsk.

The FAS won’t say if the leading sugar producers and processors are involved in the price rigging. A sugar industry expert in Moscow believes the FAS investigation isn’t serious. He says it is an “imitation of a flurry of activity.”

Khudokormov, 47 — his name in Russian means “bad feed”, “bad fodder” — was educated at the Leningrad School of Railway Troops, and then posted to field units. In 1992, after leaving the service, he and some of his military colleagues established Prodimex. At first they ran simple bartering schemes, exchanging Russian crude oil and petroleum products by the barrel for sacks of Ukrainian white sugar. By 1998 they had established a position as Russia’s leading importer of Ukrainian sugar. They then turned to building up a sugar production position by taking over Russian sugar refineries, then lobbying with other domestic agribusinesses for protection from the low-priced imports which had made them their first fortune.

Two of the original soldier founders, Vitaly Tsando and Vladimir Pchelkin, are on the Prodimex board of directors with Khudokormov. Their shareholdings were reported in 2006 by MDM Bank, manager of a debt issue to Moscow investors, to be 12.5% apiece. Khudokormov’s control stake was reported at 62.5%, and an unidentified shareholder held the remaining 15%. Another report claims that since then Khudokormov’s stake may have risen to 81%.

His growing status in the sugar industry and in domestic agribusiness is signalled by his membership of the presidium of the national lobby organization for agribusiness; last December he ranked 20th in the group of 21. This was a big leap from his standing two years earlier, when he and Pavel Demidov of the Dominant sugar group, were rated in the top-100 for name recognition in the agricultural sector, but below the cutoff line for influence; Khudokormov was placed 62nd; Demidov 74th.

Khudokormov (left) meets Kursk governor Alexander Mikhailov in 2011

Khudokormov isn’t included in the roster of oligarchs who meet President Vladimir Putin from time to time; none of the agribusiness leaders has a net worth to match them. Click. However, on the two occasions the Kremlin has paid explicit attention to sugar, Khudokormov has been called in. In June 2005, Khudokormov told President Vladimir Putin the price of bank loans and farm supplies was going up faster than the price of sugar, and that the state banks should be lending at lower interest and for longer terms.

Putin agreed, and delivered; Khudokormov and Prodimex have yet to say thanks. A joint Czech-Russian academic study of the Russian sugar market between 1992 and 2012 reported last year that Putin has been able to reverse the heavy losses in beet cultivation, harvest, yield, and sugar output, caused by the Yeltsin administration, and “very significantly boosted the production potential and reduced Russia’s dependence on imports of sugar.” The Kremlin methods: “very effective support tools based on grants, subsidies, soft loans, price support for purchases of fuel, fertilizers and energy, including tax breaks such as zero tax income for farmers.”

A study by the UN Food and Agriculture Organization (FAO) of 2013 adds that the domestic stimulus has worked because the government also introduced at the same time “the current system of variable import duties to protect local producers from volatile world market prices starting 2004…The Market Price Support averaged about USD 120/ per 1 tonne above the level of reference international prices since 2004. This level of market protection has already allowed the Russian Federation to approximate the 80 percent self-sufficiency target level.”

According to a presentation in May, rival sugar producer RusAgro reported that 83% of its gross debt is now covered in part by the government, while state interest subsidies currently pay about 19% of the company’s interest expenses. The state savings bank Sberbank holds 60% of RusAgro’s current loan portfolio. RusAgro is listed on the London Stock Exchange in 2011, and is registered in Cyprus. For the story of owner Vadim Moshkovich and RusAgro’s initial public offering in London, read more.

In 2013, when Razgulay was unable to repay its debts, state-owned Vnesheconombank (VEB) agreed to convert Rb1.11 billion (then $36 million) of obligations into a 20% shareholding, and at the same time Moscow investor AVG Capital Partners followed suit. AVG’s presentation of Razgulay’s financials early this year reports that Putin’s subsidized debt financing for the sugar sector “enables to significantly improve equity returns for investors.”

Five companies dominate the Russian sugar market – Prodimex, Dominant, RusAgro (ticker AGRO:LI), Razgulay (GRAZ:RM), and Sucden; the first four are Russian-owned, the fifth is the Russian subsidiary of the French commodity trader, Groupe Sucres et Denrées. Altogether, they account for about two-thirds of the sugar beet harvest, and about 60% of the production of sugar from sugar beet. Since FAO compiled the following chart through 2011, Prodimex has been gaining market share; Razgulay losing it.

Source: http://www.fao.org/docrep/019/i3561e/i3561e.pdf

Currently in Russia sugar extracted from beets has been growing in volume; it accounts for about 54% of supply. Another third comes from raw cane sugar – much of it imported from Brazil – and the remainder in the form of imported white sugar. The sources of supply for this are Belarus, Moldova, Ukraine, and Kazakhstan. But on account of the political conflicts, the sugar trade with Moldova is dwindling; the Ukrainian trade ran out much earlier except for smuggling, when there is an over-production of Ukrainian beets.

The one impact of US and European Union sanctions on the Russian sugar business was the decision last August by the European Bank for Reconstruction and Development (EBRD) to stop a $78 million loan agreed the year before for modernization of sugar refineries by Dominant. This hands an advantage to the French-funded Sucden.

According to the FAO report, Russian beet and sugar producers face relatively higher risks compared to other agribusinesses in the country. This is because of sharp changes in weather from severe cold to drought; availability of machines and fertilizers; and competition from more profitable crops. To sustain the profitability of the sugar business, the FAO experts recommend more state financing. “If the country is to achieve self-sufficiency, the industry must have adequate access to finance to be able to carry the large stocks necessary to ensure that sugar is marketed throughout the year without depressing prices during and shortly after the beet-processing season.”

Prodimex doesn’t release trading reports or audited financial results; its last website production report was for 2009. Its press announcements page is blank. When asked for current production and financial results the company spokesman said they are available on the website, and cut the telephone line.

The only available record is a report from Nikolai Bogaty and Tigran Hovhannisyan of MDM Bank, dated September 2006. They reveal that in 2004 revenues came to $490.7 million, earnings (Ebitda) $30 million, net profit $11.2 million. In 2005 revenues had dropped to $456.1 million, but earnings were up to $40.4 million; profit remained flat at $11.7 million. MDM was projecting a steady 7% annual increase in revenues to $792.4 million in 2011. At that point, the bank calculated that Ebitda would be $123.1 million, and profit $41.9 million. Press reports suggest the projection for 2011 was achieved.

Following RusAgro’s public accounts between 2011 and 2014, and allowing for the impact of the crop-destroying drought of 2010, Prodimex is likely to have enjoyed revenue growth of at least 12% per annum; earnings may have more than tripled. RusAgro reports its earnings margin jumped from 13% in 2011 to 31% in 2014. Then this year’s bonanza started.

RusAgro’s first-quarter results, issued on May 25, reveal “sugar sales increased by RR 301 million (+7%) due to sale prices increase that was nearly offset by a decrease in sales volume.” RusAgro’s total earnings more than doubled, and of that gain, increased earnings from sugar contributed a third. Sugar earnings grew by 112%, and the profit margin jumped from 20% a year ago to 39%.

ONE-YEAR SHARE PRICE TRAJECTORY FOR RUSAGRO

Source: http://www.bloomberg.com/quote/AGRO:LI

Razgulay (listed on the Moscow Stock Exchange with this spelling; in Russian, Разгуляй — also reported as Razgulyai, Razguliay) doesn’t issue regular audited financial results, and it has yet to report its first-quarter performance for 2015. Its last financial summary was for 2014, and indicated that sales were down 6% from the previous year to Rb14.2 billion, while Ebitda jumped 93% to Rb2 billion. Profit figures weren’t released.

ONE-YEAR SHARE PRICE TRAJECTORY FOR RAZGULAY

Source: http://www.bloomberg.com/quote/GRAZ:RM

Compared to these two competitors, Prodimex’s growth can be accounted for by its more effective tactics in expanding beet acreage and more refineries to process the output into sugar. But Khudokormov’s record for refinery and farmland acquisition includes allegations of raider tactics, intimidation, administrative measures, and manipulation of bankruptcy in local courts. “Prodimex is famous for such antics,” according to a reporter of a 2009 fight over assets in Voronezh which turned violent. For more, read this.

The latest of Khudokormov’s asset deals is the November 2014 takeover of Agrokultura, a Sweden-based farmland investment group with a public share listing. Khudokormov is behind the Cyprus-registered Magna Investments Ltd, which now appears to control the Agrokultura board.

With the takeover of Agrokultura, Khudokormov’s land holdings surpassed the total of I-Volga, and he is now the largest land owner in Russia.

LEADING OWNERS OF AGRICULTURAL LAND IN RUSSIA, 2014

Source: http://daily.rbc.ru

For more on the contest to consolidate Russian farmland into feed and food oligopolies, read this.

How much of Prodimex’s asset growth has been financed by cash reserves, how much by debt isn’t clear. In 2003 Prodimex issued Rb500 million in domestic bonds; in 2011 $150 million in credit-linked notes (CLNs). At the time Khudokormov claimed the note issue was a “reconnaissance in force”; that’s to say a marketing ploy to gauge demand for an initial public offering which Prodimex had been talking up since 2007. Both bonds have been redeemed; the IPO has failed to materialize. According to MDM, Prodimex’s gross debt was estimated at $303.4 million in 2006, with a projection of $244 million in 2011.

In 2010 the Russian business press carried promotional claims from bankers associated with the proposed Prodimex IPO in London. Their target valuation for the company was $1. 2 billion to $2 billion. Note that after Bloomberg contrived speculation of market capitalization for RusAgro above the $1.2 billion level, its cap dropped from a 2011 peak of $1.9 billion to a 2014 low of $543 million. It has recovered to $1 billion today. Its price/earnings ratio (PE) is currently a modest 2.8. Razgulay’s market cap has gone from a peak of Rb15.2 billion (then equivalent to $490 million) at the start of 2013 to a low of Rb518 million in January of this year, and Rb2.5 billion ($50 million) at the moment. Razgulay’s PE is 24.2.

Prodimex justifies its non-transparency by remaining privately incorporated. But with all the state bank finance and taxpayer-funded subsidies supporting its revenue, earnings and profit lines, how does Khudokormov repay the favours he is drawing from the public purse?

Prodimex has acknowledged using onshore tax reduction schemes in the past, but details are scanty. The MDM Bank report of 2006 illustrates this production cycle and cashflow scheme:

CLICK TO ENLARGE

Source: http://st.finam.ru/ipo/analitics%5C2383_Prodimex_rus_final_18Sep06.pdf

Terra Trade appears to have been registered in Altai for domestic tax optimization, and to have operated a tolling scheme for supplying sugar beets to the refineries, then taking out sugar to trade. The legal requirement for the domestic tax cut was investment of at least half the tax savings in the region where the scheme was registered. If investment fell short, the scheme became tax evasion. A profile of Khudokormov in Forbes Russia, dated October 2012, noticed the Altai scheme, but omitted to check its legality with the regional authorities. The Forbes report is notable too for Khudokormov’s refusal to be interviewed himself, or to allow photographs. His commercial rivals at RusAgro and Razgulay do all the talking.

The reputation for unscrupulous raiding and trading intimated by the Forbes report may have put Khudokormov off from talking to the press. It may also have encouraged an effort at compliance with Russian law. In the Prodimex corporate chart of 2006, Terra Trade was a 100% subsidiary of Meadway Holding Ltd., registered in Cyprus. Meadway in turn was wholly owned by KMI Holding Ltd., also Cyprus registered. Russian company records show that Terra Trade was liquidated in 2010 – two years before Forbes reported the Altai cutout as a company called Aquilon. Current Cyprus company records show Meadway too has been dissolved. There appears to be an pending application to strike KMI off the Cyprus register, dated June 2015:

This may signal an attempt by Prodimex to comply with current Kremlin policy on deoffshorization. But the company won’t explain.

As for tolling schemes, these were used in the Russian aluminium industry, initially when traders helped to finance cash-short refineries and production plants. They reduced tax by removing most of the profit from production plant to offshore holdings. When combined with export, as in the aluminium business, they eliminated value-added tax. Such schemes required mills to accept extortionate trading terms – higher than market input prices, lower than market output prices – often accompanied by threats to obtain local management consent. When the tollor entity was part of the same, if hidden corporate structure as the tollees, the tolling scheme was illegal tax evasion in Russian law.

Has Khudokormov been receiving state funds to acquire his sugar refineries, paying them a processing fee, and exporting the profit to his offshore entities, and then bringing a portion of the funds back to Russia to invest in beet-growing farmland? Prodimex refuses to say if it uses tolling. According to the MDM report, tolling accounted for 9.2% of beet sales in 2005, and this was expected to be reduced to 3.6% by 2011. MDM reported that tolling produced a 19.6% profit margin overall in 2005, but in some areas twice as much.

The leading source of expert analysis of the Russian sugar industry is the Institute for Agricultural Market Studies (IKAR), based in Moscow. Its director, Dmitry Rylko (below), was one of the authors of the FAO report of 2013.

IKAR’s chief expert for sugar is Evgeniy Ivanov. About Prodimex he says “their effectiveness is difficult to judge.” Sugar industry analysts in Moscow add they know nothing about Khudokormov.

Leave a Reply