By John Helmer in Moscow

There are some memorable accounts of returns and arrivals in Russia. Vladimir Nabokov in Speak, Memory (1951), for example, remembers his return from university in England, when, as he wrote, the sound of the snow and ice crystals crackled under his feet as he stepped off the train at St. Petersburg.

For Nathaniel Rothschild, also an Oxbridge man if not so well versed, the crunch sounds he may hear when he returns, or when he imagines his arrival in Russia, aren’t so literary or so figurative. By all accounts, the sounds that concern him are those of sensitive, small bones breaking. You see, Rothschild is believed in the market to owe money to a determined Russian creditor.

According to a source close to the flotation of Rothschild’s newest venture on the London stock exchange, that debt, and the consequences attached by the creditor to repaying it, help to pinpoint what Russian business Rothschild plans his new venture to undertake. Since public shareholders have been invited to subscribe for 687 million shares, at ₤10 apiece, paying a total of ₤687 million, there is that much public interest in trying to understand what Russian opportunities may be opening, what Russian risks may be lurking.

| The good news for the market is that according to the Vallar prospectus, Rothschild is a financial wizard. The key to Rothschild’s value, claims the company report, is that between 1996 and 2009 he turned $50 million into $700 million in 13 lucky years. By coincidence, the growth in value is a multiple of 13. In other words, Rothschild is claiming the track record of doubling his (or your) money every year. |  |

There may be a problem of accounting, though. Rothschild declines the opportunity to say anything at all about his debts, formal and informal covenants, obligations, liabilities, or losses that he may be carrying forward into this year, next, and 2012. These are the three years in which Vallar says it will buy assets of between $3 billion and $7.5 billion in value; or else wind itself up, and return its money to shareholders. Rothschild’s track record, as the Vallar prospectus terms it, is rich on the positive side of the ledger. There is simply no sign of the rest of his balance-sheet.

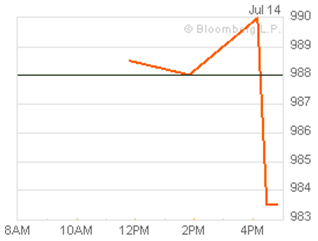

Rothschild is the principal owner of Vallar, as the new company has been called. Although Rothschild’s spokesman declined to make a copy of the prospectus available by internet, on the ground that it wasn’t available in pdf-file form, a copy of the 139-page prospectus has been obtained for study and corroboration. Vallar (ticker, VAA:LN) began open share trading on July 14, and this is what happened on the first day.

The Company, it has announced, “intends to raise gross proceeds of £687,182,290 through the Placing (subject to the effect of any exercise of the Repurchase Option) and to acquire a company or business with an Enterprise Value of between £2 billion and £5 billion (although a business with a smaller or larger Enterprise Value may be considered).” After adding £20 million in additional shares and securities subscribed by the founders, and subtracting placement fees and bank charges of about ₤25 million, Vallar is holding the equivalent of just over $1 billion in cash. If it is to make purchases on target, it will have to borrow and leverage both its own capital, and that of its acquisition targets, by a multiple of 3 to 8.

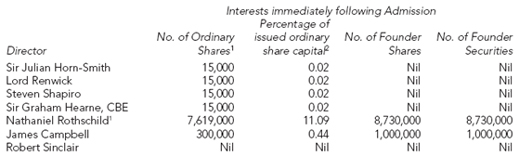

Before start-up, between April and May, Rothschild loaned the new company ₤10 million, which has been repaid. Then he led the founders of the company in paying £20 million for founder’s securities. The prospectus also reports the commitment of Rothschild and his fellow founders to buy 8 million of the ordinary shares at the placement price. Altogether then, as the prospectus notes, “the Founders and other members of the Vallar Team (through investment vehicles) have committed £100 million of capital to the Company and the Subsidiary.”

In the small print of the prospectus, it appears that the Founders have also written for themselves a handy escalator down the road, compared to ordinary shareholders. “If the gross proceeds of the Placing equal £680 million and if the Founder Incentive Subscription equals £20 million,” the document says, “the Founder Shares would be exchangeable on completion of the Acquisition for 6.67 per cent.of the then issued fully diluted Ordinary Share capital of the Company”. That suggests the founders, with an initial contribution amounting to 2.9% of the subscribed capital, intend to convert their shares into ordinary ones with a multiple of 2.3.

Rothschild is the single largest subscriber, the dominant founder, and arguably the controlling shareholder. His shareholding, according to the prospectus, amounts to 11%;much more when his founder stakes are converted. Compared to everyone else on the board, he’s top dog. Compared to the listed co-founder, James Campbell, a former executive of Anglo American, Rothschild is clearly primus inter pares:

This is worth bearing in mind when Campbell makes announcements. For example, when Campbell told the Financial Times earlier this month that he may favour buying Anglo American disposals in Brazil and South Africa, such as Copebras, the phosphates supplier, Catalão, a Brazilian maker of iron alloys, and Scaw Metals, a South African steel manufacturer, he was expressing a personal predilection, not a Vallar policy. “We could well be interested in them,” Campbell was reported as saying. “But it depends on what strategy you build around for the future.” For you, read Rothschild.

Looking at the geography of the prospectus, China dominates the outline of the company’s risk and opportunity. Russia dominates the founder’s track record. The connection between the two, and between Rothschild’s track record and what Vallar will decide to buy, is crucial to the market value of the company, because once shareholders have subscribed their money, and Vallar starts operating, the shareholders will have no direct say in the acquisition of assets.

“No Shareholder approval will be sought to make the Acquisition,” the prospectus says. “Shareholder approval is not required in order for the Company to complete the Acquisition. The Company will, however, be required to obtain the approval of the Board of Directors, including a majority of the Independent Non-Executive Directors, before it may complete the Acquisition.”

The emphasis on bulk commodity, mineral or metal producing assets naturally arouses the risk that if China stops or slows buying, the commodity price will fall, and the value of the target asset concomitantly. China, says the risk section of the prospectus, “is an important source of demand for several of the commodities targeted by the Acquisition and a reduction in the imports of such products by Chinese customers may have a material adverse effect on the Company’s prospects.

As a result of the increasing importance of China as a source of demand for products, in particular iron ore, the Company, following the Acquisition, may be adversely affected by a reduction in the imports by Chinese customers.”

Iron-ore mines appear to be one of Vallar’s favoured targets, even though the company has told sharebuyers this month that “currently, there are no plans, arrangements or understandings with any prospective target business or company regarding such an acquisition.”

“The Company will not generate any revenues from operations until after completing the Acquisition. Following the Acquisition, the Company may have operations in jurisdictions with varying degrees of political, legal and commercial stability. These jurisdictions may include, but are not limited to, the Americas, Russia and Eastern Europe.” In his remarks to the Financial Times, Campbell repeated that iron ore and coal are favoured targets.

If Vallar is in the market for iron-ore assets in Russia, the only likely seller is the heavily indebted Metalloinvest group, owned by Alisher Usmanov, Andrei Skoch, and Vasily Anisimov. Most of Russia’s remaining iron-ore assets are either required by their owners, vertically integrated steel groups, or are in the early stages of proving and development. If Vallar is after coal, then a natural target would be the coal and iron-ore mining division of Igor Zyuzin’s heavily indebted Mechel group. Both Usmanov and Zyuzin had been talking up IPO plans before the crash of 2008. Their ambitions have been delayed, and their valuations hurt by their debts. For these oligarchs, the option to swap their shares into an offshore registered, London-listed Rothschild vehicle may be alluring.

In theory, the Usmanov group, or the Zyuzin assets, would qualify according to this criterion of Vallar’s targeting: “The Directors believe that there are a number of mid-sized developing producers and emerging market based-owners, which are looking to secure alternative sources of finance and enter into partnerships.”

A source in the London investment community, which has nurtured the Vallar flotation to date, claims that Rothschild has a substantial obligation to a major Russian asset-holder of oligarch dimension. The source does not know the identity of this creditor, but claims it is not the obvious one. The source also claims that another Russian oligarch is helping Rothschild to secure the terms of his repayment undertakings. The undertaking affecting Vallar, according to the source, is that one or more of its targets may be assets held by the creditor, which he is looking to sell or swap.

For the time being, there is no corroboration that this is so. Rothschild and his spokesmen have said before that the aluminium oligarch Oleg Deripaska was not an investor in Rothschild’s Atticus funds. Sources close to Rothschild say it is nonsense to suggest that there are money or payment claims between him and Deripaska.

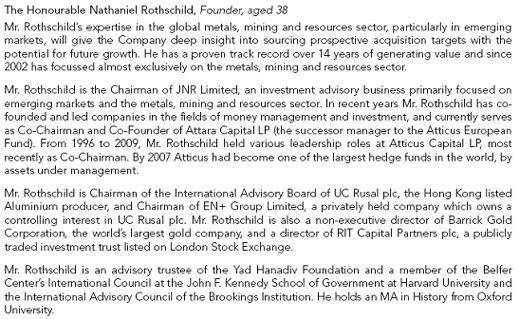

Rothschild’s disclosures in the Vallar prospectus are limited to his business resume and his track record:

The track record’s bottom-line is this: “Mr. Rothschild’s hedge fund investment and advisory activities, and business interests…on which he spent the majority of his time between 1996 and 2009, have generated in excess of $700 million from initial capital put at risk of approximately $50 million.”

The claim carries warnings and disclaimers: “The track record does not reflect all investments made by Mr. Rothschild during the calculation period, as described in “Part II – The Founders, the Vallar Team, the Adviser and the Sub-Adviser”, nor does it reflect due diligence and legal costs incurred on potential investments that were not subsequently consummated.”

In addition, the “track record of Mr. Rothschild contains certain disclosures and assumptions regarding his investment income and returns, which may not be indicative of the performance of an investment in the Company.”

The track record calculations, according to even smaller print than the rest of the prospectus, were not undertaken at arm’s length from Rothschild’s businesses, nor by an independent auditor. The prospectus discloses that “the track record is based on financial and accounting records provided by Artemis Trustees Limited (which provides administrative and bookkeeping services for most of Mr. Rothschild’s activities and investments) on behalf of Mr. Rothschild and the relevant entities through which he made such investments, including information received from third party service providers to such investment entities, but the track record has not been derived wholly from financial statements subject to an audit or accounting review. Furthermore, because such investment entities largely operated independently of each other, the financial and accounting records were not subject to a single internal control system encompassing all of the investment entities such as those which are present when audited financial statements are produced. Accordingly, there is an inherent possibility that such data, which in addition covers a substantial period of time and involves multiple independent investment entities, may not be complete in all respects.”

Artemis is registered to do business in Guernsey. It identifies Robert Sinclair as its managing director. Sinclair is also a director of Vallar. When Artemis has vouchsafed, and Vallar has accepted, Sinclair has been the trusted go-between.

“The Company believes,” concludes the prospectus, “that the track record for Mr. Rothschild covers his most significant investment and advisory activities for the period from January 1996 to 31 March 2010, and gives an estimate of Mr. Rothschild’s personal wealth created from those principal investment and advisory activities. The track record excludes both passive investments (where Mr. Rothschild did not actively participate in the initiation of the opportunity or exercise discretionary decision-making authority in relation to the underlying business or investment) and personal interest investments (which individually involved capital at risk of less than $20 million) during such period. Further, the track record principally includes items (such as advisory fees and returns on hedge fund investments) which are not contemplated to be included in any potential return for Investors in the Company and also includes Mr. Rothschild’s income and returns from investments outside the metals, mining and resources sector. Mr. Rothschild’s track record, as so calculated for the period ended 31 March 2010, has been presented to illustrate Mr. Rothschild’s ability to create personal wealth and investors should note that his historical 25 results may not be indicative of the performance of an investment in the Company. In addition, the track record presents the estimated aggregate personal wealth generated over the period from 1996 to 2010, which aggregate wealth does not reflect any substantial variations in income and returns generated within the period from year to year. The track record is principally based on realised investments but also includes approximately $162 million of unrealised investments, which until realised remain subject to losses or gains and, accordingly, could decrease or increase Mr. Rothschild’s overall aggregate personal wealth generated for the period presented in this Prospectus.”

“As a result of the above, Investors are cautioned that the track record for Mr. Rothschild may be greater or lesser than his actual total income and returns during the period. The track record is presented for illustrative purposes only and Investors are cautioned that such historical results for Mr. Rothschild may not be indicative of the performance of an investment in the Company.”

One element of Rothschild’s track record isn’t fully counted, and that has been the value of his involvement in Oleg Deripaska’s flotation of United Company Rusal. Listed in Rothschild’s bio as one of his principal sources of business experience in the mining and metals sector, the Rusal stock has lost 33% of its value since Rothschild helped launch the share in its Hong Kong Stock Exchange debut on January 27. EN+, the second Deripaska company with which Rothschild is associated, is planned for a Hong Kong flotation later this year.

Rothschild’s spokesman in London was asked to clarify the track record claims, specifically to indicate whether the wealth generation number of $700 million was or is net of losses incurred since July 1, 2008, and net of debt and other obligations? In addition, Rothschild was asked to clarify his claim to have generated “a positive financial return” for two real estate vehicles, BR Properties and TriGranit. The question asked was: “since the return on the Rusal investment is currently negative by 33%, and there were substantial losses in the Atticus funds, is the wording of the prospectus meant to convey that the only investment vehicles identified for track record disclosure purposes, which have produced a positive return, are BRP and TG?”

The answer is: “no comment – the prospectus is pretty clear as far as I’m concerned.”

Regarding debt, Vallar states: “as at the date of this document [July 9] , the Company has no guaranteed, secured, unguaranteed or unsecured debt and no indirect or contingent indebtedness.”

Note: readers who wish to form their own assessment, or who disagree, will receive a copy of the Vallar prospectus in pdf format by applying in writing to the Webmaster.

Leave a Reply