By John Helmer, Moscow

Next to prostitution, collecting scrap metal is the oldest trade in the world. Like prostitution, it prefers to do its business in the dark.

Because it’s so easy and cheap to turn sex and stolen goods into cash, the expensive capital requirement for both lines of business is in protection from price competitors and asset raiders. This helps to explain why at least half the Russian ferrous scrap trade is controlled by the seven oligarchs who run the largest steel and pipemaking mills. Of the other half, among the so-called independent scrap traders, the state-owned Russian Railways (RZhD) is dominant. That’s a fact which noone dares to report.

In the old days, a collector of scrap metal was called a tatter in the north of England. In London, he was called a totter. For simplicity sake, the scrap production chain can be illustrated this way.

Because Russia is one of the world’s largest holders of steel scrap reserves, the fifth largest scrap processor, and the fourth largest global exporter, a great deal of tattering goes on. Tottering, though, is what the independent Russian scrap traders have been doing, as the steel and pipemakers have moved to take over their sources of scrap supply, and eliminate profitability for the middlemen. The story of how they have curtailed scrap exports and kept domestic prices low can be read here. Since Russia joined the World Trade Organization (WTO) in 2012, the 15% tax imposed on exports of scrap – an early protection measure thought up by the steelmakers – must be reduced by 2 percentage points per annum. The export duty is now 10%; in two years’ time, 5%.

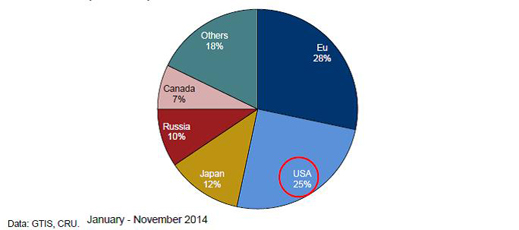

RUSSIA’S SHARE IN THE GLOBAL MARKET OF SCRAP EXPORTS

Source: Dmitry Popov, International scrap market trends and opportunities for exports from the CIS, XI International Forum "Ferrous and non-ferrous metals-2015", February 19, 2015, Moscow. Popov points out that because the US steelmakers have erected protection walls against imported steel products, domestic demand for scrap has grown, and the volume of US exports to the rest of the world is dwindling. As the rouble has fallen, Russian exports of scrap are enjoying a price advantage, replacing US scrap in scrap consuming markets like Turkey and Spain

On monthly scrap shipment data provided by Ruslom.com in Moscow, the largest of the Russian scrap merchants turns out to be Vladimir Lisin’s Novolipetsk Metallurgical Combine (NLMK) group, trailed by the TMK pipemaking group belonging to Dmitry Pumpyansky. Together, their scrap operations are roughly three times the volume of Victor Rashnikov’s Magnitogorsk Metallurgical Combine (MMK). So sensitive was he to his scrap business, he named his scrap company Profit and put his brother Sergei in charge. That story can be read here. When Profit had to be brought on to the audited public accounts of MMK, Sergei Rashnikov moved to Lugano, on the Swiss side of the Italian border, where he runs Starglobe, which tatters on a much larger scale than Profit had done back in Magnitogorsk. In MMK’s audited accounts Profit is listed as a wholly owned subsidiary; there is no trace of Starglobe.

In the domestic scrap market Rashnikov is followed in scrap volumes by Alexei Mordashov’s Severstal group; Roman Abramovich’s Evraz; the United Metallurgical Combine (OMK) headed by Anatoly Sedykh; and the Chelpipe combination of Chelyabinsk and Pervouralsk pipemills controlled by Andrei Komarov.

May 21, 2012: a rare picture at Gazprom headquarters when the pipe procurement contracts were handed out by Alexei Miller (centre). From left, Pumpyansky, Komarov, Miller, Mordashov, and Sedykh.

Source: http://www.gazprom.com

The names of the scrap subsidiaries of these steel groups include Vtorchermet NLMK; Vtorchermet Severstal; Streamcore (a Cyprus entity holding Evraz’s Siberian scrapyards, some of which are owned by an entity called Vtorresource-Pererabotka); TMK’s ChermetServis-Snabzhenie; and Meta, the Chelpipe scrap subsidiary. Sedykh is keeping his scrap supply company secret.

Just how bent, er protective the steelmakers have been towards the scrap suppliers can also be read from the fates of the two largest independents in the Russian scrap business until 2009 – Victor Makushin of MAIR (below, left), and Nikolai Maximov (right) of the Maxi Group. Makushin’s Moscow offices were deep inside a heavily armed encampment. That this didn’t protect him from attack can be read from this story. Maximov’s bankruptcy lasted for longer because he fought back. The fight can be followed here.

Because the independents depend on upstream sources of supply, and don’t own the downstream smelters which convert their scrap to steel, they cannot predict, let alone control their profit margin. In consequence, they are always tottering. Makushin attempted a horizontal diversification strategy of buying scrap businesses outside Russia – in Ukraine, Bulgaria, Poland, Italy, the US. Maximov tried vertical diversification by building steelmills in western Russia. Both failed.

By contrast, RZhD can always consign its own supplies of rails and locomotives to scrap at a discount price – steal from itself – in order to enlarge its margin at the point of scrap sale. The volume is big in scrap market terms, but a sideline for RZhD. Sometimes the profit from scrap is biggest in the domestic Russian market; that’s when the construction industry is booming, and the long steel products required for buildings and bridges are in hot demand from the electric arc furnaces (EAF) which the steelmakers use. EAF technology is supplied by scrap (below, left) ; iron-ore and coke feed basic oxygen smelting technology (BOS, right).

Click to enlarge. For more on steel smelting technologies click here.

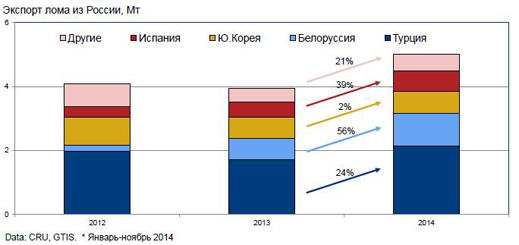

Sometimes, the biggest profit from Russian scrap is to be earned from exporting to Turkey, Spain, South Korea, and Belarus, the markets which consume about four-fifths of Russia’s scrap exports. Scratch a South Korean importer of Russian rail scrap, and you will find a crook suffering from shyness and a constant change of name; the exporters also.

DESTINATION, DYNAMICS OF RUSSIAN SCRAP EXPORTS, 2012-2014

Source: Popov, XI International Forum "Ferrous and non-ferrous metals-2015"

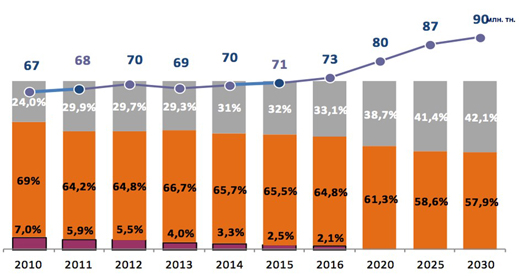

At present, Russia ranks fifth or sixth in the world table of steel producers roughly equal in output to South Korea at about 70 million tonnes per annum. China leads the table with more than 800 million tonnes, followed by Japan (110 million tonnes), the US (89 million tonnes), and India (83 million tonnes). Forecasters of the growth of the Russian steel industry over the next fifteen years indicate that most, if not all of the growth will come from demand for long steel from the construction and infrastructure sectors of the economy. Demand for flat steel for use in cars, ships and pipes may grow, but not as fast as the rate of growth for long steel.

Source: Rusmet. The grey bands represent EAF-produced long steel; the orange bands represent the BOS-produced flat steel.

The current crisis in the Russian economy is slowing down the overall rate of growth. A report by Dmitry Popov of CRU London predicts a 3% cutback in Russian steel production this year, and a 7% drop in consumption of steel. But growth will resume in 2016, and accelerate to the 4%-5% range in 2017. Popov’s forecast for Russian scrap over the same period is more dire – collection or production of scrap, which was growing at 7% in 2014, will be flat this year and next, and maybe 2017 too.

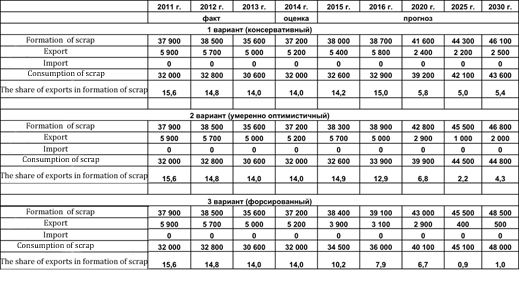

What this means is that as the trend towards more EAF or electric steel continues, the recovery of Russian steel production will require more scrap supplies, but they must be obtained from a static volume of scrap output. Result – exports of Russian scrap will fall 8% in 2016, 13% in 2017, according to Popov.

According to these three forecasts by Rusmet, exports will almost dry up.

Rusmet is a brave Moscow consultancy, established by Victor Kovshevny, for the analysis of all aspects of the Russian metallurgical industries, including steel, pipes, and scrap, ferrous and nonferrous. Its scrap division, Ruslom.com, produces a website called by the same name. Its annual industry convention was held in Moscow in February.

Kovshevny is trying to persuade the independents, as well as the big steel group scrap processors, to agree on new legislation to modernize the government’s cumbersome licensing and regulatory schemes, and reduce the administrative costs and corruption. It is understandable that the small-margin independents want to reduce the cost to them of licensing, red tape, and the bribery required to keep inspectors away from the scrap yards, rail sidings, and port terminals. The totters say they are happy to lobby for government relief through a collective organization. They are not so happy to see that organization turn into the industry regulator. For the time being, the scrap businesses prefer the government devil they know to the business competitors they don’t trust.

According to a leading western expert on the Russian scrap sector, “one thing is clear. Russia is not collecting enough scrap (or producing enough scrap substitutes) in the right geographical regions to support all the new domestic EAFs; the increased scrap demands presented by Russia’s integrated steel groups; and the demands of the regional export markets which Russia has supplied until now.”

What happens in a market when volumes are falling, prices are falling, export markets are contracting, domestic markets are more competitive, and payback on investment requires more than 24 to 36 months to return? The answer is usually consolidation by the more powerful players of the weaker ones.

In this scheme of things, discovering where the real power lies in the sector depends on data about volumes of scrap, sales revenues, and ownership of company names. Historically, Russia’s ferrous scrap industry has been one of the most competitive, and also one of the most secretive, least transparent segments of the steel sector. From the prospectuses and corporate reports of the listed steelmaking companies, it is possible to gauge that they have gradually consolidated control of their scrap supplies, increasing the proportion they sourced from themselves from about 30% in the year 2000 to almost 70% today. But when the CRU consultancy in London was asked what that proportion is, Popov replied: “we don’t have the data on the scrap collectors in Russia and therefore I’m not really in the position to make a guess, not even an educated one because I really don’t know the scrap collection by company.”

When RZhD is asked to estimate the volume of the scrap it sells each year – so that its share of the Russian scrap market can be figured out – RZhD refuses to say. It also is impossible to identify the names of the RZhD subsidiaries which conduct this business, let alone the names of the managers in charge. This is a state company, bear in mind, run by Vladimir Yakunin (right). Long before the US sanctioned him for his patriotism, domestic investigation of Yakunin suggested that there was something er, bent about the railways’ accounting. For the Yakunin archive, click.

When RZhD is asked to estimate the volume of the scrap it sells each year – so that its share of the Russian scrap market can be figured out – RZhD refuses to say. It also is impossible to identify the names of the RZhD subsidiaries which conduct this business, let alone the names of the managers in charge. This is a state company, bear in mind, run by Vladimir Yakunin (right). Long before the US sanctioned him for his patriotism, domestic investigation of Yakunin suggested that there was something er, bent about the railways’ accounting. For the Yakunin archive, click.

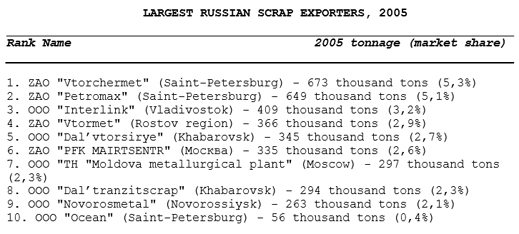

Apart from RZhD, none of the independent scrap processors, exporters, or traders appears to hold a market share of more than 5 percent. None appears financially, logistically, or managerially strong enough to absorb competitors, at least at the national level. A decade ago, the top-10 scrap names were:

A year later, in 2006, sector sources claimed that MAIR and Maxi were in the top-5, along with Vtorchermet, Uraltvorchermet, and Meta of the Chelpipe group. Today the big steel and pipemakers have absorbed these names; those which remain are confined to regional catchment areas with an overall market share of 2% or less. Together, Ruslom.com and other industry experts believe they generate annual revenues of more than $900 million in export sales alone; the latter comprise about 10% of total Russian scrap sales by tonnage. There is no reliable estimate for the revenues of the domestic scrap market.

Istok Corporation has published its top-10 of domestic scrap suppliers for the three quarters of last year, but tonnage and market share are missing:

Source: https://twitter.com/ruslom

Who then are the top-5 independent scrap producers and traders in Russia with a chance of surviving? Popov of CRU says he doesn’t know. “At the moment it is hard to analyse these data,” Ruslom.com acknowledges. “The large companies work through operating companies which often change their names because of taxes.” In practice, the experts concede they don’t know the names of the companies which operate in the sector; the magnitude of their capacities, production, sales, or exports; the market shares of the main players; the proportion of the market controlled by the oligarch-owned steel groups, by the independents, or finally, by RZhD. Flying by night, tottering in the dark.

Leave a Reply