By John Helmer, Moscow

@bears_with

If you want to understand who is winning the American war against Russia on the Ukrainian battlefield, and also in the world’s commodity trade markets, you can start by calculating the life expectancy of a NATO-trained Ukrainian soldier on the front line, or of a NATO staff officer in a command bunker he thought was secret. Then you can check the life expectancy of a Russian pig.

The losses of the former are Russia’s tactical gains; they aren’t yet victory in the war.

But it’s the latter, the Russian pig who, upon turning into pork, is breaking through the enemy’s defences towards strategic victory of Russian economic power to capture a world market. This means defeat – unrecoverable loss of market share – for the hostile states led by the once powerful pork exporters, Germany, Spain, Denmark, Canada, and the US. As the most recent European Union pig and pork slaughter data show, the war is pushing up the energy and feed costs of pig farming, and drastically cutting European exports of pork to the Asian consumer market, the biggest in the world. Also now, the Chinese government is on the point of deciding who to favour if Beijing allows a limited lifting of the African Swine Fever (ASF) ban — the Russian pig or European and American pigs.

Behind the Ukraine front, the test of who is winning the war against Russia is also who puts their money and their meat where their mouth is. In Russia, meat consumption is rising per capita to a level never recorded before in Russian history. At the same time, the country has become the world’s fifth largest pork producer.

“Practically speaking,” says Yury Kovalev, “we no longer have imports, but not because this is closed, but because over the past fifteen years an entire industry has been created, production has grown every year, and we have almost completely abandoned import dependence.” Kovalev is general director of Russia’s National Union of Pig Breeders.

“For us, export is now the main direction for growth. Back in 2019-2020, Russia reached about 200,000 tonnes of exports, which is about 5% of our total production. In 2023, the export of pig products can reach 220,000 to 230,000 tonnes. The main strategic challenge of the Russian pig industry in the next ten years is to enter the top-5 of world pork exporters. To [achieve that] it is necessary to double exports to at least 350,000 to 400,000 tonnes; that’s up to 10% of domestic production.”

On current projections, Russia’s pork exporters expect that by the end of 2025 – one year beyond the battlefield defeat of the Ukro-NATO forces – the profitability of Russia’s pig exporting companies will depend on rising export demand, especially in China, Vietnam, the Philippines, and Thailand. This, the exporters say, will require accelerated growth in grain output to feed the pigs, which in turn depends on low to stable fertilizer, fuel, other energy and grain prices.

These are Russia’s strategic advantages in the present war. They are killing the profit margins and competitive advantages of the US-NATO side, and forcing the allied states to trade between themselves. This is the thin end of the NATO sausage.

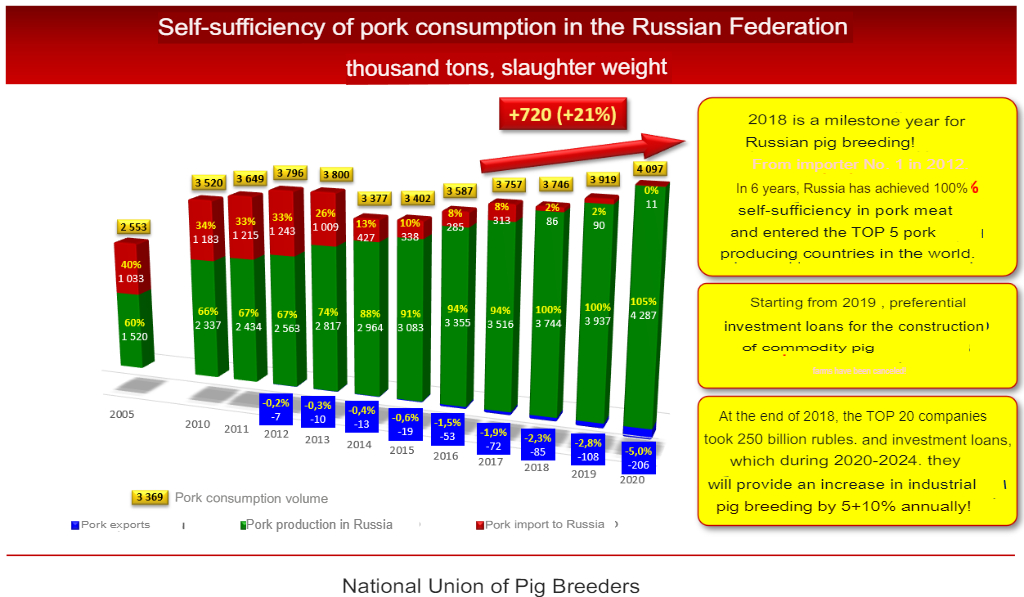

By 2018 Russia was able to achieve full self-sufficiency in pork. This came after twenty years in which pork imports began by gobbling half of the Russian consumption market. US exporters understood that while the loss of the Russian export market was bad enough, war sanctions would benefit Russian pork exports and damage the US pork rival in the rest of the world.

“Awhile back, Russia was a major buyer of proteins in the world market. We still remember when prices for chicken leg quarters in the US, or the price of beef in Brazil, would be greatly affected by events in Russia. That is no longer the case,” a US consultancy reported to the agro-industry market last year. “High feed and energy costs are negative for US livestock producers, and they will negatively impact their ability to bring more product to market. Ultimately this is bad news for US meat protein consumers.”

By the end of March of this year, Rosstat, the state statistical agency, reported the number of pigs on the farms of all agricultural producers across Russia had increased by 5.7% compared to the figures at the end of March last year to reach 28.3 million head.

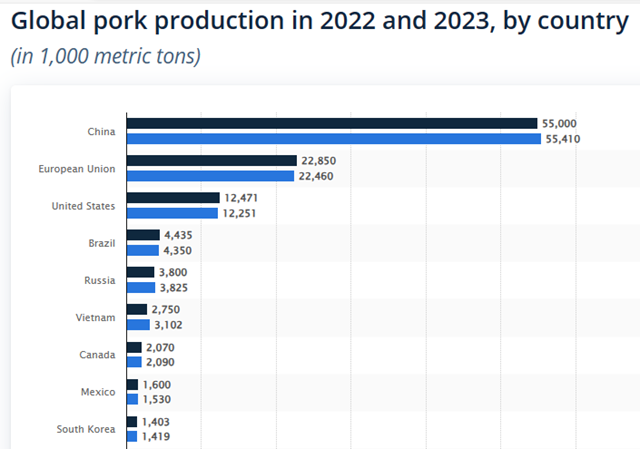

Source: https://www.statista.com/

In 2018, when self-sufficiency in pork was first reached, the volume of Russian consumption was 3.74 million tonnes. In 2022, the consumption figure was up to 4.37 million tonnes. At the same time, production of pork was rising faster than consumer demand. In 2022 production was 5.28 million tonnes in live weight; it is projected by the pig breeders’ union to hit 6.03 million tonnes in 2025.

The domestic production is accelerating into market surplus, so the wholesale prices of live pigs and slaughtered meat have been declining. The average price for 2019 was 9% lower than for 2018; in 2020 prices dropped another 5%. The price decline is continuing. It was down 6% in 2022, and down another 7.5% in the first quarter of this year.

This trend, combined with the dropping rouble rate of exchange, has boosted the competitiveness of Russian pork in global trade. Until the war began, the Ukraine was a major market for Russian pork exporters, trailing behind Vietnam and Hong Kong, but ahead of Belarus, Kazakhstan and Mongolia. Replacing the Ukraine with other countries of the CIS and southeast Asia has already been achieved, according to the June 2023 trade reports.

“Russia has decided to become the world's largest pork exporter”.

In a report published last week in Moscow by Vzglyad, the leading source for Russian political and economic analysis, Russian strategy for replacing the Ukraine and boosting exports to the Asian market was described as “an ambitious but realistic task, but on condition that Russia manages to discover new markets in southeast Asia.”

First of all, Kovalev of the Union of Pig Breeders told Vzglyad: “we are talking about opening China as the largest consumer and importer of pork, as well as entering the markets of the Philippines and Thailand, with which there are no geopolitical contradictions. This year China will import 2.1 million tonnes of pork, the Philippines 600,000 tonnes. The list of the largest importers [worldwide] also includes Japan, the United Kingdom, and South Korea, but they are impossible for war reasons.”

“Unfortunately, China is still closed for Russian pork due to the presence of the African Swine Fever virus (ASF). China has closed imports from all countries, including European ones, where this virus was detected and which is spreading rapidly around the world. For example, in 2019, the virus reached Germany, and China stopped the import of German pork. China is really afraid of this plague — there are no geopolitical problems here. But China understands that sooner or later it will still have to open its market, even as this virus continues to spread. It is already in most of Europe, although it is not yet in Brazil and the United States. But many people have already realised that even with this virus, you can trade.”

“You don’t have to close an entire country if the virus is present in part of it. There is such a thing as regionalisation. This means that pork can be allowed to be imported from regions of countries where this virus does not exist. We [Russia] have totally ASF-free regions. Vietnam and Hong Kong have already recognised our regionalisation. The Vietnamese market opened for us in 2019. Today we are already one of the main suppliers of pork there. In two years we have taken almost 40% of all imports of pig products into the country. We have won our place from our main competitors – Brazil, the US and the European Union (EU). This proves that we can supply to the Asian market, that we have absolutely competitive products both in quality and cost.”

“China itself produces 55 million tonnes of pork. They have the most modern production, but they lack land and fodder. They are now building 26-storey pig complexes in the mountains and buying huge amounts of soybeans, including in the US, to feed their pigs. With the production of 55 million tonnes, which the Chinese themselves consume, they lack another 2-3 million tonnes per year, which they buy. It’s not much, and it’s hard to call that import dependency. Rather, they need imports simply to balance their internal market, to buy more when there is not enough to go round. Therefore, China will always import 2-3 million tonnes.”

“In practice, we do not want to get half of that but only 5% to 10% of this import pie.”

At the moment there are high-level negotiations between Russia and China to break through the swine fever ban. As Kovalev says, the Russians are trying to achieve a phytosanitary agreement from Beijing to allow pork from the ASF-free regions of the country. But the French and Germans are competing to persuade Beijing to agree to open for their pork also.

The immediate impact of war sanctions in 2022 cut the flow of Russian pork exports, not so much because of US and European Union meat bans – Russian pork was not being sold in those markets at the time. Instead, the problem was the disruption of Russian logistics chains for the export trade, including the withdrawal of western refrigerated containers for shipping, as well as the international payment system through western banks. “But already in the second half of last year, these problems were solved and exports were restored,” Kovalev told Vzglyad. “Therefore, the year–on-year drop was relatively small — by 10% to 170,000 tonnes. Last year, exports to Ukraine fell sharply by 80%. Exports to Vietnam have doubled, and this is the main buyer of our pork. On the other hand, part of the [Ukraine] losses was compensated due to the growth of exports to Belarus, which tripled in volume to 80,300 tonnes.”

Left: Yury Kovalev; right, Nikolai Birulin.

In direct interview, Nikolai Birulin, the chief market analyst for the Union of Pig Breeders, said he is confident Russia can overcome the ASF problem and persuade China to open up.

“For fifteen years swine fever has been present on the territory of Russia, so the government and business have gained vast experience in ensuring biosafety. Thus, the Rosselkhoznadzor [Federal Service for Veterinary and Phytosanitary Surveillance ] has created and implemented systems of compartmentalisation and regionalisation for the ASF virus. Businesses invest huge amounts of money to maintain and develop a biosafety system at their enterprises. Together, these efforts make it possible to keep the situation with ASF at a controlled level and ensure an annual increase in pork production of 5% to 10%.”

OPEN IN A NEW PAGE TO ENLARGE

OPEN IN A NEW PAGE TO ENLARGE

Birulin explains the impact of the US-NATO war on Russian exports. “Of course, sanctions make it difficult for companies to work for export. After their introduction, most logistics companies left the Russian market, which is why the cost of logistics to the non-CIS countries increased by a multiple, and that reduced the competitiveness of Russian companies in export markets. Also, there have been problems with payments. But business always finds a way out. All these issues have been partially or completely resolved. In addition, our target markets for pork exports are the CIS countries and the friendly countries of southeast Asia. The political influence of our competitors in these directions is limited.”

With Russia’s production and export growth there has been a steady increase in the concentration of the pig farms and processing plants into large conglomerates – this is the oligarch trend.

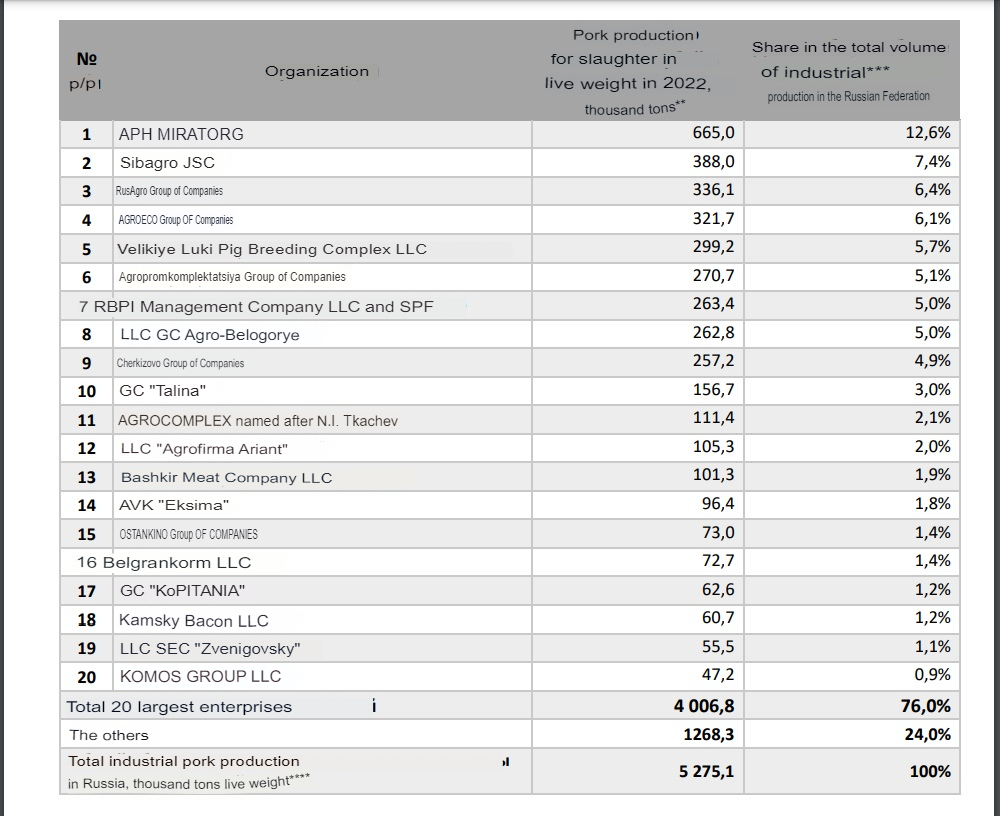

According to Birulin, “the development of the pig industry will take place according to this classical scheme — industry leaders are being formed. Thus, the share of the top-20 pig farming companies is constantly increasing: in 2022 it has reached 76% of the industrial pork production. Still, for the time being, the concentration of production at the very top is at a comparatively low level; for example, the share of the top-3 companies last year was slightly over 26%, while in other developed markets their share exceeds 50%. The consolidation of the industry will continue. The companies in the top-10 are likely to increase their market share.”

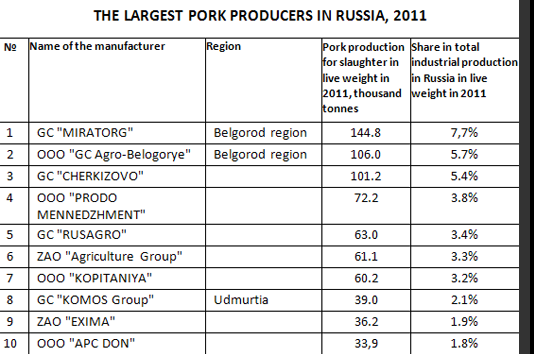

A decade ago, this is how the story was reported of the Russian pork oligarchy in the making.

The top-10 Russian pork producers were ranked in production and market share at that time:

Source: https://johnhelmer.net/?s=pork

By the end of 2022, this is now the ranking of the top-10 pork producers:

Source: https://vetandlife.ru/ (February 2023).

Miratorg not only keeps its first place, but it has more than tripled its production in slaughter weight; gained overall market share; and stretched the gap between itself and the next ranked producer Sibagro, which was not on the list in 2011. Rusagro ranked number 5 in 2011 with 63,000 tonnes of production; it is now number 3 with 336,100 tonnes of output. Cherkizovo has fallen behind, comparatively speaking. It ranked number 3 in 2011 with production of 101,200 tonnes; it is now number 9, with 257,200 tonnes.

Miratorg is owned by the brothers, Alexander and Victor Linnik; follow their business story here. Rusagro is owned by Vadim Moshkovich; click to read the archive on his operations. Cherkizovo was founded by Igor Babaev and continues in the control of his sons, Sergei and Yevgeny Mikhailov, and other family members; here is the Babaev archive and the Cherkizovo backfile. The sanctions list of the US Treasury’s Office of Foreign Assets Control does not name any of them.

Left to right: Victor Linnik, Vadim Moshkovich, and Igor Babaev.

The key to future profitability for the pork oligarchs, and for Russia’s pork production and export trade over the next five years — Russian analysts and company executives acknowledge — is to hold livestock numbers level and cut the price of fodder, which takes the largest share of the cost of pork production; and also to take over the abattoirs and integrate live pig farming with delivery of packaged pork products to the retail shops.

Rusagro has told Vedomosti, the Moscow business newspaper, that it intends to increase production for another one or two years, and will then stop.

In order to maintain profitability, pig farmers will have to engage in self-sufficiency in feed grain, Kristina Romanovskaya, owner of the small producer Lazarevskoye, told Vedomosti. About 60% of the companies from the top-20 pork producers in the Russian Federation are already supplying their own grain by more than 50%, Kovalev told the newspaper. But for climatic reasons, this is difficult to achieve for pig farmers in the northern regions of the country. It can also be cheaper for the pig farmers to buy feed grain in the spot market than to invest in land and grain cultivation.

For more on the feed market in Russia, click to read.

The pig breeders’ union believes that if grain harvests stay up and grain prices come down, the top-20 producers will become self-sufficient in fodder supply by 2025. By then too, according to Kovalev of the union, the slaughter and processing capacities will reach 100% at the major producers. Rusagro says it has already reached this point.

Sergei Yushin (right), executive director of Russia’s National Meat Association, said in direct interview: “Russia is now fully provided for in forage crops. Moreover, we ship compound feeds to the EU and a total of 59 countries around the world. The leaders in procurement are China, Denmark, Lithuania and Germany. In 2021-22 the volume of Russian shipments increased by 14%. There are no sanctions on these products, but there are some difficulties with the logistics.”

“In 2005 70% of our pork production came from private domestic household producers. Now the top-25 companies have taken over this share. Consolidation isn’t finished and the export trade is a good opportunity for development. Most of the companies now have the full production cycle — farms, grain production, slaughterhouses, warehouses, logistics, selling points, etc. Nowadays Russia completely sustains itself with pork. The increase of export won’t have influence on the domestic market. Our main directions for export are southeastern Asia and Africa. We work directly with those countries. The North American countries have never been our target of interest, because they have their own production. So the sanctions have no impact on Russian exports of pork.”

Leave a Reply