By John Helmer, Moscow

The comic book character known as the Gambit was kidnapped from the hospital where he was born and raised by a gang of thieves. He got his way with unusual powers, like kinetic energy and hypnosis. He was also famous for his skill at card-throwing and combat with a long stick. He was distrusted by his peers, but loved by the ladies. He ranks 65th on the Top 100 Comic Book Heroes of All Time.

Alexei Mordashov ranks No. 70 on the Top World Billionaires, but he is nothing like Gambit. He does make a specialty, though, of throwing cards, asset cards, in and out of stock exchanges. After making a notable failure of his Nord Gold scrip-tossing trick on the London stock market in February, Mordashov now appears to be trying the same gambit with a different set of cards. Not goldmining companies this time, but iron-ore mining companies.

The tale of Mordashov’s goldmining gambit has been told in great detail before; it ended in February, when the Nord Gold prospectus was withdrawn from the London Stock Exchange before listing. Mordashov’s tactics in assembling his portfolio of gold assets make a longer, lurid tale, ending in a bitter and unsuccessful attempt to force Canadian minority shareholders in the High River Gold company to sell out at a low share price; and a costly contest against a North American rival for the Crew Gold Company, which obliged Mordashov to pay an $81 million takeover premium.

Salutary though the lessons of this goldmining portfolio may be for Mordashov and the Severstal management, as well as for the share markets, the only acknowledgement Severstal Resources, Mordashov’s mining division, has demonstrated so far is that it refuses to answer questions from this reporter, whatever may be asked.

Before the goldmining gambit came to its conclusion, Mordashov has attracted much criticism from his peers and the Moscow investment institutions for his gambits in coalmining assets (borrowing from the company to finance personal asset purchases and then reselling the assets back to the company at a profit), and in paying peak prices for North American steelmills which almost triggered the entire group’s bankruptcy with $8.3 billion in debt at the end of 2008. All but two of the US steel assets have now been sold off – at considerable losses.

Now for the latest in the iron-ore gambit. Severstal announced this week that it is acquiring a 25% stake in a Brazilian iron-ore exploration project in the northern Amapa region. The investment, estimated to cost $49 million over several stages, is in a Brazilian company, SPG Mineracao. A call option has also been agreed, allowing Mordashov to buy another 50% of SPG if the exploration results prove a mine is feasible. Severstal Resources claims the Amapa project has estimated resources of up to 1.5 billion tonnes of iron ore at an Fe (iron) grade of up to 45%. Iron-ore concentrate potential is estimated at 10 to 20 million tonnes per annum.

What Severstal would want or need a an iron-ore mine in Brazil for, now that its North American steelmill empire, a shadow of its former self, needs far less iron-ore to feed its furnaces, is uncertain. But before the question can be answered, here’s what Mordashov has already put into his offshore iron-ore portfolio. Amapa is the third in the sequence.

In December 2008, through a Netherlands-affiliated company called Lybica, he bought 65.5% of African Iron Ore Ltd, which holds mining rights for the Putu project in Liberia. The initial down-payment was reported to be $8.3 million; a second payment of $4.2 million followed in October of 2010. Drilling at Putu had just begun in 2008, and reserves were initially reported at the 500 million-tonne mark. This was upgraded by an expert study in February of this year to 2.4 billion tonnes.

Alexander Soloviev, the Putu project leader, is reported in company documents as saying that at present, “further extensive drilling is underway as part of the Bankable Feasibility Study, scheduled for completion in 2014, with interim Pre-Feasibility study being completed by 2012…We expect to start production at the end of 2017, with potential output of at least 20 million tonnes of concentrate. This project will allow us to become a significant player in the iron ore seaborne market.”

Seaborne market does not mean that Putu’s iron-ore production is meant for delivery to Severstal steelmills in North America.

The second in the acquisition portfolio landed in May of 2010, when Severstal bought a 16.5% stake in Core Mining, a British Virgin Islands company, which holds licences to explore for iron-ore in the Avima iron-ore deposit in the Republic of Congo (Brazzaville) and the Kango iron-ore deposit in Gabon. Both projects are at the early exploration stage. Avima reportedly holds 500 million tonnes of reserves with mineralization of up to 69.75% Fe. In its May 13, 2010, announcement, Core Mining said Severstal would spent $55 million for its stake and to finance exploration over two years through 2012.

Newspaper reports claim that these projects may require up to $4 billion in capital spending to start shipping iron-ore. That’s not money Mordashov can afford to spend, and may be less than effective in borrowing. Last month Core Mining added a potentially more bankable investor, Glencore. The company announcement of April 18 says: “Glencore International AG has made an investment in the Company. In conjunction, Glencore will act as marketing agent for supply to Core Mining’s customers for initial volumes of iron ore produced by the company’s projects. Both Core Mining and Glencore have agreed to pursue future co-operation in a number of areas relating to the development of the Kango and Avima iron ore projects.” No money figure has been disclosed.

Industry analysts in Moscow express doubt that Severstal has the technical ability to advance these projects to the operational mine stage. “They don’t have an iron-ore team,” one source added, noting this is of less importance now during low-cost exploration than it will be later, when high-capital cost mines come on stream.

Mordashov has told his mining managers they are to aim at accumulating a portfolio of iron-ore projects with a target production capacity of up to 50 million tonnes of iron-ore per annum. But what is the point? Is Mordashov aiming to supply his Russian and North American steelmills with this extra ore, or is he aiming at spinning off the iron-ore mines outside Russia into a stock exchange vehicle for the killing he hoped but failed to achieve with Nord Gold?

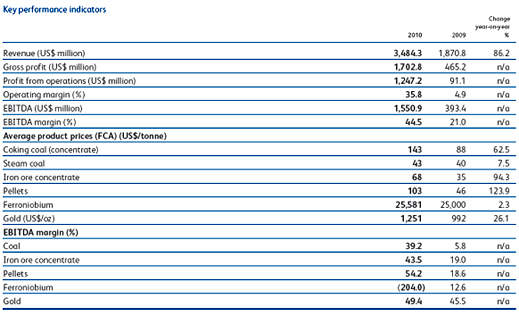

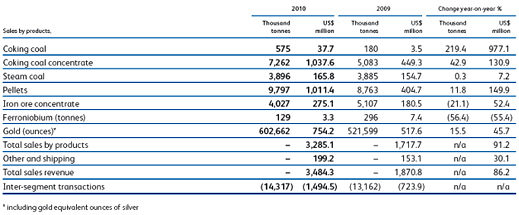

Here is how Severstal reports the recent performance of its mining assets worldwide, from the 2010 Annual Report:

Determining the iron-ore volume required to supply Mordashov’s steel production and expansion programme isn’t easy. According to Severstal’s annual report for 2010, just out, there is no anticipated need for iron-ore supplies from outside Russia to feed the projected demand of Severstal’s Russian steelmaking operations. That’s because “we are fully self-sufficient in primary steel-related raw materials in Russia, and in the US our local coking coal capacities are more than sufficient to provide full economic integration for our steel plants in North America. We target at least 80% global economic self-sufficiency in both iron ore and coking coal, to secure cost competitiveness, improve total margins, and smooth our performance over the cycle. We build and develop steel assets only in those regions where it’s possible to get access to competitive raw materials at a price below global benchmarks. We will continue to prioritise investments in raw materials to achieve this self sufficiency goal, so that our steel production is fully balanced by own iron ore and coking coal.”

Mordashov already operates two iron-ore mining complexes in Russia. They are known as Karelsky Okatysh and Olkon. Karelsky Okatysh is in Kostomuksha, in the Karelia Republic of northwestern Russia. It produces iron ore pellets with an iron concentration between 63% and 65%. Company documents say Karelsky Okatysh operates two major deposits “with an estimated life of 34 years, based on our estimates of JORC reserves plus expected reserves extension.” Olkon is in the Murmansk region of north-western Russia, and is an open-pit miner, with deposits that have an estimated life of 19 years, “based on our estimates of JORC reserves plus reserves extension.”

The company annual report says the investment budget for Karelskiy Okatysh and Olkon aims at preserving the current level of iron-ore production, without a big increase anticipated. “We plan to spend around US$47.9 million on projects at Olkon. These include the renovation of production facilities (US$12.4 million), investments in long-term development projects and new technology (US$15.7 million), safety measures (US$1.9 million) and maintaining the current level of production (US$17.8 million). Through our investment programme at Karelsky Okatysh, we aim to maintain 2010 production volumes. This includes renovating production facilities (US$16.8 million), maintaining the existing level of extraction (US$57.4 million), investing in long-term development projects and new technology (US$10.5 million), and safety measures (US$1.0 million).”

Current iron-ore pellet sales volume at Karelsky Okatysh complex were reported for the first quarter of this year at 897,724 tonnes, down 28% on the last quarter of 2010. Full-year output capacity for Karelsky Okaytsh and Olkon is between 9 million and 12 million tonnes. In 2010, the company reports sales volume of 9.8 million tonnes of iron-ore pellets, 4 million tonnes of concentrate.

The bottom-line then is that as far as Mordashov’s strategy for Russian steel operations, he doesn’t need the offshore iron-ore projects at all. Corollary – he isn’t likely to borrow the billions of dollars likely to be required for bringing those mines on stream.

The rationale then for the West African and Brazil projects is ambiguous. In Severstal’s annual report, the offshore iron-ore projects are called “growth options” – that may refer to growth in demand from Mordashov’s US steelmills; or it may mean growth in demand from the global commodity markets; or it may mean growth in the stock market valuation for iron-ore mine shares. According to the Severstal Resources section of the annual report for 2010, “we continued to develop a portfolio of growth options in steel related mining by investing in acquisitions and developing early-stage mining projects internationally.

In North America, there is no sign of a Severstal plan to expand steel production so much as to require freshly mined supplies from Africa or South America. If anything, Mordashov has ordered his managers to cut back on costs, stabilize output, reduce loss-making. Thus, the annual report says: “In North America, where we operate as Severstal North America (SNA) [the aim is] to focus on our core steel-making strategy, in May 2010, the Group sold Northern Steel Group, engaged in the processing and distribution of steel products in North America… The sale of the above North American assets is a key component of our strategic refocusing, which centres on the development of our Dearborn and Columbus facilities. These are two of the most technologically advanced plants in North America, with partial upstream integration into coking coal through PBS Coals (Severstal Resource), also a member of the Severstal Group.”

The Dearborn, Michigan, mill (formerly known as Rouge Steel) turns out steel sheet for US automobile builders. Together with the Columbus, Mississippi, mill, company documents claim that total output capacity in plan is 5.5 million tonnes per annum. But Dearborn already is at target capacity of 2.3 million tonnes. So, it seems the capacity growth is intended at Columbus – from 1.6 million tonnes at present to 3.1 million tonnes. But Columbus operates electric-arc furnaces (one already in operation and another intended for the capacity expansion), and they use steel scrap, not iron-ore, for feed.

To be sure of this, Severstal’s spokesman in Moscow, Natalya Ivanova, was asked to say what volumes of iron-ore products are currently required for Dearborn and Columbus, and how are they sourced. The spokesman has not responded.

A clearer statement of Mordashov’s intent comes from Boris Granovsky, director of strategy and corporate development at Severstal Resources., He is quoted as telling a Moscow business newspaper this morning that Severstal intends to expand its presence in the market of iron-ore outside Russia. “Now most of the raw materials the company produces for its own needs, but thanks to new projects, it could become a significant player in this market.”

Despite the sizeable $6 billion debt the Severstal group still owes, and covenants which its bankers have imposed on its asset purchase plans, Granovsky is quoted as claiming that in the next five years Mordashov wants to spend $1.1 billion for fresh mining assets, of which $547 million will be in gold, and the remainder divvied up between iron-ore and coal. To clarify what kind of advertisement Granovsky is placing for Mordashov on the equity and debt markets of the world, Granovsky was asked to say how big an iron-ore player Severstal aims to become. He did not reply.

An international expert on Severstal’s mining strategy says that adding iron-ore supplies from Africa and Brazil would have made sense when Mordashov was the owner of an American steel empire. But after losing his shirt on that gambit, iron-ore projects make sense as a stock market or international commodity play. “It would be rather hard for iron-re imported from Brazil to compete on a delivered cost basis with pellets from US and Canadian iron-ore producers like Cliffs and IOC, especially given Dearborn’s interior US location.”

“I think the original rationale for Severstal acquiring international iron-ore assets changed, as a result of the decision to divest most of the North American steel assets (liabilities). Originally, self sufficiency in iron-ore supply was the driving motive. But now, after the divestment, the strategy is probably more driven by a simple desire to build an international iron-ore producing business, maybe 30-50 million tonnes per annum in production, which may or may not generate opportunities for iron ore ‘swaps’ to improve supply to Severstal’s steel mills.”

Leave a Reply