By John Helmer in Moscow

Sovcomflot (SCF), the state oil tanker company and currently the 5th energy shipper in the world, has made its first detailed public disclosure to investment markets in a multi-million dollar debt prospectus. Deutsche Bank, JP Morgan, and VTB are the arrangers.

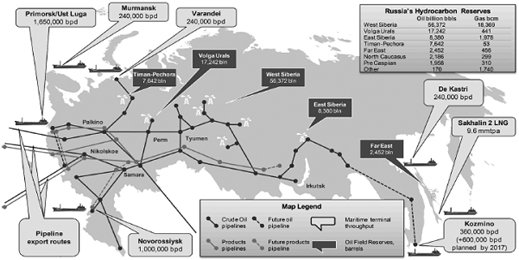

SCF operates a fleet of more than 147 vessels; it reports annual revenues of $1.3 billion and assets approaching $6 billion. It is part of the vast Russian energy production and export concession which is supervised by Deputy Prime Minister Igor Sechin, despatching globally each day these volumes of oil and gas:

The new debt notes, whose total value has yet to be announced, are to be issued by a newly created Ireland subsidiary of Sovcomflot, and they are unsecured. However, default risk is guaranteed by the Russian parent. The company says its total debt is $2.6 billion, almost all of that in the form of secured bank loans. The new debt notes will be sold to substitute unsecured for that secured debt, and cover what the prospectus describes as “general corporate purposes, including the repayment of existing secured indebtedness.”

A disclosure by the ratings agency Moody’s indicates that Sovcomflot’s target is to sell about $500 million of the debt notes. But Moody’s has announced it is downgrading SCF’s issuer rating one notch – from Baa2 to Baa3. This change, according to Moody’s, “reflects the contractual subordination of the proposed bond issuance in the capital structure of the group, which currently includes only senior secured debt (that after the notes issuance will decrease to approximately 80% of the total).” But for this, Sovcomflot enjoys an improved prospect, according to Moody’s, on account of the “expected stabilisation in the company’s operating performance over the near future, which will allow SCF to further strengthen its financial profile.”

Moody’s analyst Marco Vetulli has also told investors to disregard the growing debt burden – debt to earnings ratio — of the company, as it continues to pay out for new vessels, because it is 100% state-owned, and of strategic importance to the Russian state as an oil and gas transporter. Accordingly, reports Vetulli, “the default dependence between the Russian government and the company is low.”

But what if unforeseen circumstances arise in which the government is obliged to put SCF and its current managers at arm’s length — even dissociate government policy from the management’s conduct?

Moody’s says the stand-alone picture for SCF – ignoring the government’s backing – is far riskier as the financial results are “relatively weak in the first half of 2010; and [there is] the expectation that a full recovery of its financial profile will be quite slow and will occur only by the end of 2011.”

SCF, the government ministers on its board, and its chief executive, Sergei Frank, a former federal Transport Minister, have already dissociated the company from the preceding management and operations. What if that happens again, this time as a result of a ruling by the UK High Court which will be issued shortly?

The new prospectus is the first time that Frank has released details to the investment market of the 5-year High Court lawsuit he launched against his predecessor, Dmitry Skarga, and former SCF chartering partner, Yury Nikitin. The SCF prospectus runs to 333 pages. Just one page refers to the litigation, one of the costliest ever waged in an international court by a Russian state company. Lawyers in the case say the trial judge, Justice Andrew Smith, has been reviewing the materials for seven months, and may issue his judgement within days or weeks. There is no mention of the trial or the Smith judgement in Moody’s assessment of the risks currently facing creditors of Sovcomflot

According to the SCF prospectus, “the Proceedings concern allegations that Messrs. Skarga and Nikitin, who were former colleagues, embarked on a course of dishonest conduct following Mr. Skarga’s appointment as CEO of Sovcomflot. This conduct led to certain Sovcomflot subsidiaries entering into transactions, relating to the sale and leaseback of vessels, with companies affiliated with Mr. Nikitin. These transactions were on unfavorable terms for the Group and consequently seriously detrimental to the interests of Sovcomflot and its subsidiaries, and correspondingly for the benefit of Mr. Nikitin and the companies that he owned or controlled. The claimants under the Proceedings also allege that millions of dollars were paid by Mr. Nikitin, with Mr. Skarga’s knowledge, by way of bribes to Mr. Privalov and to Igor Borisenko, who was at the time the Executive Vice President and Chief Financial Officer of Sovcomflot. Mr. Privalov and Mr. Borisenko have both admitted to the receipt of such payments. It is also alleged that bribes or other unlawful benefits were paid to or conferred upon Mr. Skarga.”

In the courtroom trial, which began on October 1 last, and wound up on March 31, Skarga and Nikitin have counter-charged Frank and his associates, including high Russian government officials, of lying to cover up a corrupt oil shipping scheme of their own. Evidence was presented in court from Moore Stephens, the international marine auditors commissioned by Frank, which dismissed the allegations of wrongdoing in the vessel transactions. Under cross-examination by the lawyers and by Justice Smith, Frank’s chief witnesses, Yury Privalov and Igor Borisenko, admitted that before they testified in court, they had been threatened with prison, and then employed as consultants by Sovcomflot.

During his appearance in the High Court witness box, Frank attacked this correspondent for reporting accurately on the proceedings. The archive of these reports is available here.

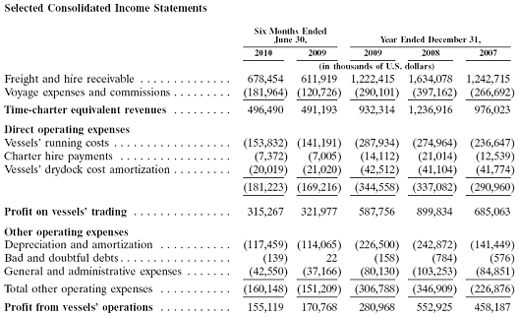

The financial reports detailing SCF’s fleet operating costs and expenditures – the most detailed since testimony was presented in the High Court by former company executives and accountants – indicate that it has been making less money on its tankers than it did in 2007, while its costs and charges have been growing:

The big $61.2 million jump in this year’s item “voyage expenses and commissions” is apparently not a running cost, like vessel fuel, but rather an increase in commissions. The company explains the change this way: “This increase was primarily due to the increase in the Group’s exposure to the spot market, as explained above, and the increase in fuel costs by approximately 60% during the six months ended June 30, 2010 caused by higher global prices for oil and oil products.”

For a behind-the-scenes understanding of how and for what purposes commissions are paid for vessel charters, the High Court proceedings transcript is without precedent in Russian shipping history. According to the allegations of Frank, Skarga had contrived the charter arrangements to feed his own pocket. The evidence admitted by Privalov and Borisenko is that they filled their own pockets.

Privalov and Borisenko told the court that notwithstanding their admissions, and the payback of $3 million between them to the company, they have been employed by Frank as paid consultants, at least through 2009. The prospectus does not go into detail for the item, “general and administrative expenses”, where personnel paid from the company headquarters, and the legal and associated costs of the London trial, would be expected to be included. In 2007, well before the trial began, SCF says the item was running at $84.9 million. In 2008, when lawyers, detectives, and other litigation costs jumped, the item was $103.3 million – up 22%. In 2009, the figure dropped to $80.1 million. In the first half of this year, the figure was $42.6 million, up $5.5 million (15%) over the same period of last year.

However, lawyers close to the High Court action say the combined legal costs of Sovcomflot and their targets come to about $100 million.

Sovcomflot has told its creditors in the prospectus: “As of June 30, 2010, the Group had recovered greater than US$ 80 million by way of settlements, and the balance of the claims under the Proceedings was in the region of between US$ 810 million and US$ 880 million. The judgment is expected before the end of 2010. The Group has obtained security and freezing injunctions covering assets belonging to the defendants in the Proceedings with an aggregate value of US$ 602 million to secure the payment of any award of damages under the Proceedings.”

Although not itemized in the prospectus, the recovery estimate of $80 million is probably from an out of court settlement in June 2008 by the London broker Clarksons (₤27 million, $54 million), and the return of money by Borisenko and Privalov.

It is customary in prospectus reports of such high-stakes, high-cost litigation to estimate and provision for the liability that may be owed by the plaintiff – in this case, the debt note issuer — in the event that the court rules against it. Sovcomflot’s prospectus says only: “In connection with the freezing injunctions, the Group was required to pay a total of US$ 7 million into court by way of undertakings in damages. Having taken legal advice, however, management of the Group does not believe it likely that these undertakings in damages will be called upon.”

It’s common in Russia for influential businessmen or state officials to enjoy a high degree of confidence in the rulings of Russian courts, in advance. President Dmitry Medvedev has publicly called this by its popular name – “telephone justice”. It is not common for plaintiffs before the UK High Court to inform their shareholders and creditors that there is no prospect of their losing the judgement. If the legal defence by Skarga and Nikitin is vindicated by the ruling of the court, they are bound to counter-claim against Frank and Sovcomflot for at least $50 million in costs, plus dozens of millions of dollars of financial losses caused by the asset freeze, plus damages.

The seven million dollar set-aside will be recovered by Frank and his board if Justice Smith rules in their favour. But if he favours the defendants, Sovcomflot faces a much bigger liability. The detail of the ruling will also provide the first exhaustive independent assessment of how Sovcomflot is run.

Leave a Reply