By John Helmer, Moscow

The shrinking violet of English literature, Jane Austen (image top right), said it best: “Nothing is more deceitful than the appearance of humility. It is often only carelessness of opinion, and sometimes an indirect boast.”

Alexei Mordashov (image centre) likes to think of the Business System he has introduced at his steel company Severstal as a sign of genius. He even spells the management method with capital BS, which is also the way managers speak of it.

In Severstal’s annual report for last year, the same thing is headlined “Transformational Thinking” (TT). Far from being transformational, the language in the annual report describing the BS is conventional share-price touting: “Among industry players, our Business System is unrivaled in terms of the extent of its integration and EBITDA contribution potential. The system aims to optimise company-wide operations, unify goals, create a strong corporate culture and improve KPIs ranging from profit to efficiency to health and safety targets.”

This week Mordashov invited steel industry analysts who can be counted on to believe this to listen to his presentation of what the company called “further progress in implementing the Business System of Severstal and continued targeted investment.” The briefings have not been released publicly.

One of the analysts reports that “what management terms the “Severstal Business System” is expected to be the main contributor to EBITDA [earnings] growth through cost optimization, debottlenecking and corporate culture improvements. Management claims the system has already contributed $248m of EBITDA in 2011 and that this amount will increase to $1.3bn by 2015.”

In the annual report for 2011, Mordashov claimed “the Business System has contributed ~ US$130.9 million and US$88.4 million to the Company’s EBITDA to date.” That adds up to $219.3 million, 12% less than claimed earlier; arithmetic is not one of the BS strong points. “By 2015, we expect the total EBITDA contribution to reach [about] US$1–1.2 billion.” That was reported by Severstal on April 17. Less than five months later, the added value from BS has grown by $100 million.

Concretely, what Mordashov and his managers now want to say is that they have abandoned Mordashov’s old strategy of buying steelmills at premium prices, wherever he can find them, and integrate them with new iron-ore and coking coal mines to feed the furnaces and expand global steel capacity – until Mordashov is number-1, 2, 3, 4, or 5 in the steel world by volume of production.

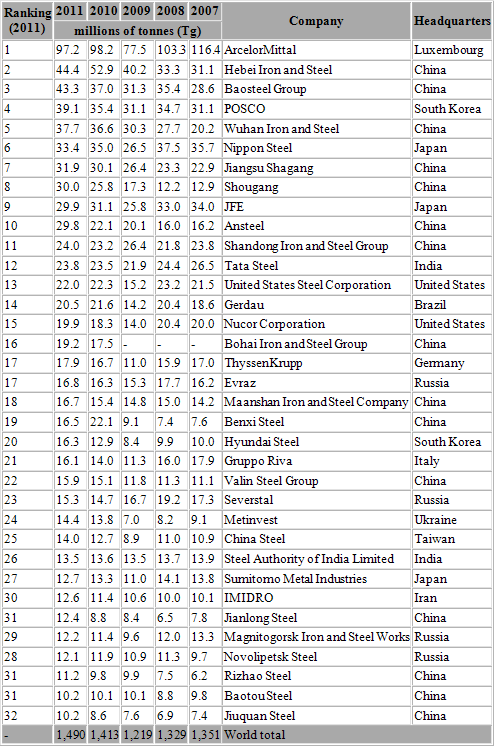

As the table shows, Mordashov doesn’t even rate as no. 1 in Russia. In global terms last year, Severstal ranked no. 23.

Sources: worldsteel.org and wikipedia.org.

For the first time Mordashov is now saying he is no longer aiming to buy or build significantly more steel production capacity than he is already operating. In fact, he is not even saying he aims to recover his peak capacity level of 19.2 million tonnes. That was achieved in 2008, just before Mordashov’s costly US steelmills pitched the entire company to the edge of bankruptcy. Mordashov has never quite acknowledged the genius that got him into that position. Here is a balance-sheet of his losses.

On Monday Mordashov announced that when construction now under way of the Balakovo mini-mill is completed at the end of 2013, that will be the company’s last steel expansion project. The construction steel producer in Saratov region is planned to have an annual capacity of 1 million tonnes. Added to this year’s estimated output of around 15.6 million tonnes, Mordashov seems to be disclaiming an output target by 2014 of greater than 17 million tonnes.

As for mining, Mordashov said he is postponing his group’s large-scale iron-ore projects, such as Putu in Liberia. That is something of a fudge. Several weeks ago in London, Mordashov was telling investment institutions he was looking to sell down his stake in the project if he could find a partner to fund the development costs; these are estimated by sources in Liberia to run as high as $2 billion. For the time being, Mordashov has found no takers. He has already promised the Kremlin, according to his associates, that he will not attempt to spend this money out of Severstal’s resources or borrowing capacity.

Mordashov is also acknowledging now that he is ready to cut the capital expenditure planned for this year of $1.6 billion to about $1 billion, if global steel market conditions continue to deteriorate. But Severstal said it isn’t expecting that to happen. The company said it is forecasting global steel consumption to grow by 4% per annum over the next five years, driven still by Chinese growth. The company says it sees potential in the short term for a steel price rebound on production cuts and cyclically low inventories in some regions. The company vice president for strategy, Thomas Veraszto, said at Monday’s briefing that mining costs are rising by about 10% per annum in US dollar terms, and postponement of new iron-ore mines will support current iron-ore prices. Demand for imported coking coal will continue sustain price growth for coal, he added. According to Veraszto, forecasts of zero or negative growth for Chinese steel production are unlikely.

“We have a great potential for growth, but it is not associated with an aggressive acquisition of assets for cash”, Mordashov announced.

What is unstated in this comedown is the impact Kremlin pressure has been having since January in dissuading the Russian steel oligarchs from repeating their offshore asset-buying folly of 2007-2008. The story of how Evraz’s owners Roman Abramovich and Alexander Abramov dropped their half-billion dollar bid for South African steelmaker, Scaw Metals, was told in April and at the start of May. In parallel, but much better known, Victor Rashnikov, owner of Magnitogorsk Metallurgical Combine (MMK), was persuaded to drop his half-billion dollar takeover of the Australian iron-ore miner, Flinders Mines.

The writing may have been on the wall for the steel oligarchs last January. they then appeared to have congratulated themselves on their success in talking President Vladimir Putin out of doing anything heavy-handed after the election. Still, the red-light warning from the Scaw Metals and Flinders Mines deals is still having to be flashed in Abramovich’s face to oblige him to comply.

A sign of this is the signature this week of First Deputy Prime Minister Igor Shuvalov on a government directive imposing investment outlay targets on Evraz as a condition for it to acquire control of the new Timir iron-ore project in fareastern Sakha.

Alrosa agreed to sell 51% of the undeveloped project to Evraz in September 2011 for about Rb4.95 billion ($154 million). But only yesterday the federal government issued its authorization for the deal to proceed and Evraz to take operational control of the mine, but requiring both Evraz and Alrosa to meet investment targets. These set milestones and deadlines for exploration, mine and mill construction, and production levels at the mine and the processing mill. To insure that neither Evraz nor Alrosa can sell their stakes before the milestones are reached, the government has ordered the state-owned Vnesheconombank (VEB) to take a special share of the Timir project company. This will come with the preemptive right to buy out the Evraz 51% or the Alrosa 49%, or veto their sale to anyone else.

The vesting of this special investment planning right in the state bank is fresh evidence that the Kremlin is still aiming to oblige steelmakers like Evraz to invest in domestic raw material mining and in domestic steelmaking capacity, in preference to the offshore ventures the oligarchs have typically preferred in the past.

Alfa Bank steel analyst Barry Ehrlich reported to clients today that the new order from the government is “negative for Evraz because it reduces the company’s ability to sell at a profit prior to the completion of milestones. On the other hand, VEB’s involvement in the transaction suggests to us that the bank would provide much-needed (and possibly off-balance sheet) project financing. State financial involvement is crucial to the project’s success.”

Leave a Reply