By John Helmer, Moscow

Oligarch ownership hasn’t given Russian goldmines a good name, or at least not a stable one. So if you take the 5-year view and judge that the gold price has peaked, while the cost of developing new mines is going up, the grades going down, you don’t need to be an oligarch with a short attention span like Mikhail Prokhorov, to figure out that the prudent investment direction is the exit.

When Prokhorov sold his 37.78% stake in Polyus Gold last month for $3.6 billion, his Onexim holding announced: “in light of …our view of the balance between the company’s achievements and its potential, we made the decision that the time had come for Onexim Group to sell and realize its profit.” On the 5-year view there have value peaks on paper, but ultimately no profit. Prokhorov has also failed to find an international goldminer willing to buy the assets. As Russian dealmaking goes, selling to Suleiman Kerimov, or to his stand-ins, as Prokhorov has announced, is a nothing more than a state bank bailout.

According to Onexim, that’s almost the end for Prokhorov’s interest in Russian mining. Except that the Onexim website claims that “Russia is home to vast deposits of still unexplored natural resources, which makes investments in their development very attractive for investors.” The only mining asset recorded still in the holding’s portfolio is Intergeo. But this is what happens when you click on this — http://www.mmcintergeo.ru/. Moribund.

Intergeo has been run by Prokhorov’s old school chum and alter ego, Maxim Finsky (right image). It was built by a process of accumulating mine prospect licences inside Norilsk Nickel, and then spinning them off into a separate entity. That was similar to the process which Prokhorov and Vladimir Potanin had agreed on together for the creation of Polyus Gold. In the case of Intergeo, however, Potanin charged Prokhorov and Finsky with nicking the assets.

The modus operandi didn’t work twice, however, because unlike Polyus Gold, which actually mined ore, produced and sold gold, Intergeo was only a prospector; it had shovels and paper plans to sell to the market, but no cashflow. The paper proved unconvincing, and the attempt which Prokhorov and Finsky made in May 2012 to sell Intergeo shares on the Toronto Stock Exchange (TSX) failed miserably.

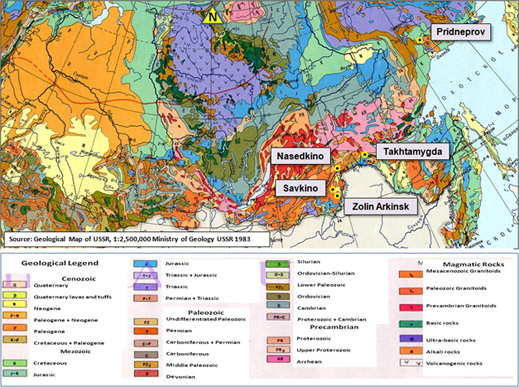

That failure left Finsky with White Tiger Gold (WTG), a small producing goldmine called Savkino in the Chita region (Transbaikal krai), and several other prospecting licences. Here is a map of where they are:

The WTG story began with a share price of C$6.87 on January 6, 2011; it is now 5 Canadian cents. Its market capitalization on the Toronto Stock Exchange has gone from C$2.2 billion to C$24 million. The share price trajectory since Finsky took control sets something of a record among Russian miners.

3-YEAR SHARE PRICE TRAJECTORY OF WHITE TIGER GOLD

Source: Bloomberg

This is how Finsky reversed the Russian assets he was holding in the private Russian entity Dalsvetmet into the Toronto-listed TWG. Here is the continuation of the story when Finsky arranged for WTG to merge with a bigger Canadian goldminer, Century Mining. And this is how the combination was preparing for its fall a year ago.

Since then the share price of WTG has dropped from 48 cents to 5 cents, despite financial reports from WTG showing – for the nine months to September 30, 2012 – that gold production was up 19% over 2011, gold sale revenues up 26%, and gross profit up 83%.

Notwithstanding, after a doubling of administrative charges and extraction of a 15% rate of interest charged by Finsky for lending money to WTG, the bottom-line has continued to be loss-making. WTG’s explanation for the surge in its administrative expenses from $3.7 million to $8.6 million is that they “include increased wage and salary obligations as a result of an increase in staff, higher legal and accounting fees, and leasing costs resulting from the relocation to new offices.”

The junior goldmining investment market in North America attracts constant analysis, and investors pay close attention to rumours for signs of future share price direction. So it was when a Deutsche Bank executive claimed at a Canadian conference early this month that WTG is getting ready to sell Century Mining’s mines; and that if the deal materializes there will be a news release in about two weeks. The Deutsche Bank man didn’t identify the potential buyer apart from suggesting it was smaller than a big mining company. The timing in the forecast is about now.

One of the Canadians who heard this says he is suspicious. “I believe Intergeo is making another run at a TSX listing. Wouldn’t surprise me that the Russians buy back the mines from the bank for Intergeo on the cheap, since we don’t know the amount defaulted on.” The source was speculating. He was also referring to last year’s default, when Century Mining was unable to produce enough gold to meet loan repayment terms with Deutsche Bank. WTG announced what had happened on May 25, 2012. The detailed release suggested that WTG had decided to let Deutsche Bank take over Century’s mines in Quebec and Peru, removed Century mining’s assets and liabilities from its active balance-sheet, and concentrated instead on Finsky’s original Russian assets: “The Default and the enforcement proceedings are not expected to affect White Tiger’s Russian assets…Going forward, White Tiger intends to focus on the continued development of its Savkino and Nasedkino projects in Eastern Russia. The Savkino mine continues to be on target to meet its expected production of 20,000 ounces of gold in 2012, and White Tiger is currently developing Phase 2 of the expansion plan at the Savkino mine with the objective of increasing gold production to approximately 50,000 ounces in 2013.”

In the event, WTG didn’t make its gold target at Savkino. By the end of the year, it had produced just 18,261 troy ounces. Hope for more was undiminished: “we remain on track with the development of Phase 2 of the Savkino Mine—scheduled to go into production in May of this year.”

Did this shortfall mean that not enough gold was delivered to Russian state bank VTB to meet its loan repayment terms, and trigger a second default? The answer depends on how much money VTB has loaned WTG. According to Finsky’s initial announcement, through WTG, VTB was offering US$150 million. Exactly how much has been drawn, and how much WTG has received, are questions WTG’s reports don’t make certain. The company’s last financial report, issued last November, says: “On February 2, 2012, Diascia entered into an agreement with VTB for a senior secured term loan facility (the “VTB Facility”) of up to USD$150 million to fund White Tiger’s production, development and exploration activities. The VTB Facility has a final maturity date of 60 months from the date of execution of the facility agreement, that might be extended for up to 24 months at the sole discretion of VTB. Interest is calculated at a floating interest rate of 3 month LIBOR plus a margin of 8 to 14% per annum, based on White Tiger’s annual gold production. Security for the VTB Facility includes guarantees of the OpCos, as well a pledge by Diascia of its participatory interests in the OpCos and pledges by White Tiger and Diascia Holdings (BVI) Ltd. of their respective shareholdings in Diascia. The funds are to be made available in three tranches, with the initial USD$80,000,000 of the facility divided equally into tranches A and B. Tranche C, in the amount of USD$70 million, remains uncommitted, however Diascia may request, upon written notice, that VTB make the funds available, and is subject to further negotiations between the Company and the bank.”

It seems that just US$40 million was paid out by VTB. That was on March 26, 2012. Diascia, the recipient, is described in WTG’s papers as the Cyprus-registered company which is a subsidiary of WTG. The two are connected, possibly owned by Diascia Holdings, a British Virgin Islands registration.

Who in addition to Finsky owns Diascia (BVI) isn’t known. How much of VTB’s $40 million may have stuck to Diascia’s palms and not been handed over to WTG is also not known.

Immediately after the VTB disbursement, WTG repaid Sberbank $10.3 million owed from the year before. Rouble loans equivalent to US$1.5 million and $833,000 owed to IFC bank, a Prokhorov entity, were also repaid from the VTB cash. Other loans due to Finsky and the second Russian shareholder of the company, Sergei Yanchukov, were also paid out from the VTB money. These were all high, or very high, interest-rate loans. According to WTG, “it is the policy of the Company to conduct all transactions and settle balances with related parties [Prokhorov, Finsky and Yanchukov] on market terms and conditions in the normal course of business.” Finsky’s loans to WTG were through an entity called Kirkland Intertrade Corporation, while Yanchukov’s loans came from his company called Unique Goals International Ltd.

Still, it seems most of the VTB first-tranche loan of $40 million failed to make it out of Diascia’s account and into WTG’s. Again according to the last WTG report, on March 26, 2012, “Tranche A, in the amount of $40 million (USD$40,000,000), was received by Diascia. A portion [sic] of the proceeds of Tranche A was used to repay existing secured and unsecured bank loans.” Six months later, by September 30, WTG says “the Company’s loans and borrowings increased by $10,677,000 (current and noncurrent) as at September 30, 2012, as compared to December 31, 2011, primarily as a result of the first drawdown of the VTB Facility. The drawdown was used in part to repay existing secured and unsecured bank loans and the balance to support the Company’s operating activities related to the Savkino mine.”

What happened to $29.3 million – that’s the difference between $40 million and $10.667 million, which appears to have been kept by Diascia? According to WTG, “in addition [to its quarter-share of the VTB first loan] the Company received new shareholder loans of USD$9.5 million and repaid a shareholder loan of USD$3.0 million in the first nine months of 2012.” The total debt shown on WTG’s books as of September 30 was C$22.5 million. But most of that appears to have come from Yanchukov, whose loans through Unique Goals are reported to have been C$20.4 million as of July 31, then revalued to C$17.5 million after an extension of the maturity date to 2015. Yanchukov also charged WTG for the loan extension by taking share purchase warrants. By October last, after taking repayments and extending new loans, WTG seems to have owed Finsky (Kirkland) $5 million. This was then converted into shares, clearing the debt and leaving Finsky with 50.09% of the WTG issue. At the same time, Yanchukov was reported to be holding a 17% stake.

The second and third VTB loans remain hypothetical. WTG says: “Tranche B in the amount of $40 million (USD$40,000,000) can be utilized by Diascia upon the fulfillment of certain conditions precedent among others, the delivery to VTB of an updated NI 43-101 compliant technical report on the Nasedkino project.” The company claimed in September that it was days away from receiving another $19 million from VTB, and on October 10 the money was paid, this time to WTG, not to Diascia: “The initial drawdown of US$19 million under Tranche B has been received by the Company and will be used to fund the Company”s capital development program.”

That left $21 million to be drawn from the tranche. By the end of the year, WTG admitted it couldn’t do that because it was producing less gold for delivery to VTB to sell than its loan terms required. “As the Company now expects that it will not meet the December 31, 2012 gold sales covenant under the VTB Facility, VTB Capital has been notified to ensure that any potential concerns of VTB Capital are addressed and so that the Company will continue to have access to the remaining $21.0 million under the VTB Facility.”

The talks with VTB dragged on into February without agreement. Technically, WTG was in default, it conceded, but VTB wasn’t issuing formal notice and seizing the collateral. The financial position for WTG was so dire last month that Yanchukov had to come up with a loan of $1.5 million to tide the company over for 30 days while it continued negotiating with the state bank.

The company issued this claim on February 21: “On February 21, 2013, Diascia received a letter from VTB Capital stating that all the rights and remedies now or at any time in the future available to VTB Capital under the VTB Facility are hereby reserved. To date, the Company has not received any notice from VTB regarding any intent to realize its security under the VTB Facility.” Asked this week whether WTG is in default, and what VTB intends to do about it, the VTB spokesman said: “VTB has good relationship with White Tiger Gold. The Bank has no problems when working with this client.”

As UK High Court judges say, this was less than candid — at least it was between December and last week. Then what happened is that Finsky sold out to Yanchukov. At least according to the WTG announcement on March 20, it seems the company has a new owner, although why and how this resolves the VTB default isn’t clear from the release. “White Tiger Gold Ltd… announces that it has been notified that an insider and shareholder of the Company, Unique Goals International Ltd (“Unique”), has completed the purchase (the “Purchase”) of an aggregate of 268,700,731 common shares of the Company (“Shares”). The Company understands that the Purchase was completed by way of private transactions with two beneficial shareholders of the Company, with 238,700,371 Shares being purchased from companies wholly-owned by Mr. Maxim Finskiy, a director and insider of the Company, and 30,000,000 Shares being purchased from Inger Industries Ltd.”

The owner of Inger, with 6.2% of WTG’s shares and thus the second selling insider, made his public debut in this announcement. He hasn’t been identified yet.

WTG went on: “Unique is controlled by Mr. Sergey Yanchukov. As a result of the Purchase, Mr. Yanchukov now beneficially owns, or has control and direction over an aggregate of 338,300,208 Shares, representing approximately 70.25% of the issued and outstanding Shares. If the warrants of the Company controlled by Mr. Yanchukov are fully exercised into 204,010,013 Shares, Mr. Yanchukov would control 542,310,221 Shares representing approximately 79.10% of the issued and outstanding Shares (after giving effect to such exercise).”

The transaction looks like a case of Tweedledum and Tweedledee, and there has been no clarification from WTG since the Yanchukov takeover. At what price has Finsky sold to Yanchukov? How can the latter afford it? And why should VTB be so satisfied with the outcome it has agreed not to seize the assets Yanchukov has just paid for?

The transaction looks like a case of Tweedledum and Tweedledee, and there has been no clarification from WTG since the Yanchukov takeover. At what price has Finsky sold to Yanchukov? How can the latter afford it? And why should VTB be so satisfied with the outcome it has agreed not to seize the assets Yanchukov has just paid for?

The likely answer is that VTB loaned Yanchukov the fresh money to chase out the bad. If so, VTB should have some explaining of its own to do, since the records of Yanchukov’s Moscow-based holding, Mangazeya, reveal a tiny oil business, little cash, accounting losses, and significant debt. A Moscow newspaper report this week estimates the market value of the sale and purchase transaction for WTG at $16 million; that is sixteen times more than the Rb37.7 million which Mangazeya calculates to be its asset value on February 28. The newspaper also reports that VTB had lost confidence in Finsky; why, has not been reported.

Finsky speaks to newspapers when he is advertising. He and Intergeo’s chief executive, Grigory Potapov, refuse to answer questions on these issues and the company’s intention to try another shot at selling shares on the TSX.

Mangazeya reports its financial condition in 2010 and 2011 here.

In the group’s annual report for 2011 it is claimed that it produced just over 12,000 tonnes of hydrocarbons, mostly gas condensate. The sales value was reported at Rb172.7 million (about $6 million).

Yanchukov’s deputy and chief executive of Mangazeya is named Evgeny Konstantinidi. He was contacted at his Moscow office and asked these questions: Has Mr Yanchukov bought out all remaining interests of Mr Finsky and Mr Prokhorov in White Tiger? How much does White Tiger [note: not Diascia] owe to VTB? Have White Tiger and associated companies defaulted to VTB, and what is the way out of that problem? What is the strategy for White Tiger now?

Konstantinidi replied that at present he and Yanchukov can’t provide comments, but if and when they will have something to say, they will do so.

Leave a Reply