By John Helmer in Moscow

A public statement by Deputy Prime Minister Alexei Kudrin, which he then corrected a few hours later, confirms what Russia’s rival oligarch groups, including those seeking Rusal’s bankruptcy, have believed for many weeks. Oleg Deripaska, controlling shareholder of United Company Rusal, has given up control of his shares to Russian state officials in order to stave off his foreign and domestic creditors. It is also the decision of the state officials involved that, for their interest, possibly the state’s, but not necessarily to benefit Deripaska himself, the company must be protected from a shareholding combination of Chinese, Libyan, and other foreign shareholders. In short, Rusal has been nationalized in effect, if not in form.

This is not a last-minute expedient to make Rusal’s initial public offering (IPO) of shares appear to be a genuine privatisation transaction. The transfer of Deripaska’s control stake is a new stage in the way in which state officials run the aluminium concession, which Deripaska has brought to the point of bankruptcy at home, and asset forfeit abroad.

Kudrin, who is also the Finance Minister and holds a seat on the board of Vnesheconombank (VEB), was commenting last Wednesday, November 25, in advance of what was expected to be the Hong Kong Stock Exchange’s (HKEx) approval of Rusal’s listing application; the review of the application of the application had been scheduled for November 26 by the HKEx Listing Committee, after it had postponed consideration at its meaning the week before.

Kudrin was trying to explain what would happen to Rusal after the IPO, at which VEB had already voted to buy at least 3% of the 10% of new shares to be issued. That vote, on November 19, was led by VEB’s chairman, Prime Minister Vladimir Putin. According to Kudrin, “Deripaska will lose control after issuing the 10 percent. But we’ll get the controlling stake after buying 3 percent. VEB made this decision and I voted for it as a supervisory board member.”

Kudrin was clearly implying that the state would take control of the company away from Deripaska at the board and shareholder level; at present, Deripaska is the chief executive, with a control stake of 53%. The board chairman is Victor Vekselberg, with an 18% stake (shared with Len Blavatnik). For foreign investors to buy into Rusal’s IPO, Kudrin appears to have meant that they could count on a state guarantee of control of the company. The implication was that Kudrin acknowledged that Deripaska was a risk he knew potential investors – possibly the HKEx — were having trouble accepting ahead of the IPO.

Noone in Russia of high official rank has ever dropped a hint like that one before. Later in the same day, Kudrin tried to clarify the meaning of what he had revealed. “When I said Deripaska and VEB would jointly control more than 50 percent,” the minister claimed, “I didn’t mean that the government would control the company together with Deripaska. There will be more than 50 percent in total, from a mathematical point of view.” Kudrin then claimed that the state bailout bank will participate in running the company “within its 3 percent.”

Because VEB has already been doing this since it gave Rusal a $4.5 billion loan in November 2008, Kudrin can’t have been acknowledging the obvious. What has already been widely reported about the VEB transaction of a year ago – the single largest bailout by the Kremlin of any Russian company or oligarch – is that it is secured by the 25% stake in Norilsk Nickel, which Rusal had borrowed to acquire in early 2008; plus at least two of Rusal’s domestic aluminium smelters. In addition, the state auditor, the Accounting Chamber, plus other government agents, conducted a review of Rusal’s operating accounts during December 2008 and January 2009, reporting to the government and the VEB on what they had found, and what control measures they recommended. That report, according to the Chamber, is a state secret.

So what was new in what Kudrin tried saying twice over? In almost all major bailouts by governments around the world, it is the accepted practice that the chief executive or controlling stakeholder cedes operating control of his insolvent enterprise, in return for the rescue and the investment of public money. Deripaska has almost acknowledged this himself. For he told a Bloomberg interviewer, as part of a promotion of the Hong Kong share sale early this month: “I am not working for money. I have my interests and I try to realize what I can do, and for now I am focused on Rusal because it is very important for Russia.”

Russian banking sources believe that what Deripaska meant, and what Kudrin also meant to expose publicly, is that Deripaska has made an agreement with high state officials to cede a large part of his control shareholding, in return for their protection against his ouster altogether. Informally, and also secretly, this makes Deripaska a de facto trustee. Seeking a bankruptcy procedure against an insolvent Rusal would do the same thing de jure, according to Russian law and accepted bankruptcy administration practice. But, it seems, high state officials have already decided that won’t be necessary in Deripaska’s case. He, it seems, is offering a cash-out and buyback option to the state, much like those he has already signed over to Cherney, Vekselberg, and the other major shareholder, Mikhail Prokohorov.

Kudrin was letting this cat out of the bag.

Regarding Deripaska’s qualifications to continue running the company, the Russian government has long been split into two factions. President Dmitry Medvedev, his economic advisor Arkady Dvorkovich, and to a lesser extent First Deputy Prime Minister Igor Shuvalov have been in favour of trusting Deripaska to get on with the job. They proved unable, however, to formalize Deripaska’s proposal for the state to acquire preferential, non-voting shares in Rusal in return for more cash to cover his liabilities. Had they succeeded, they would have taken over the aluminium concession, and its benefits, according to the informal Russian code of governance, from political rivals, Prime Minister Putin and Deputy Prime Minister Igor Sechin.

In 2006, Putin and Sechin were clearly in command of the state aluminium concession. They favoured Deripaska to absorb Vekselberg’s SUAL aluminium company, and told the latter he would not be allowed to go to the London Stock Exchange (LSE) to list SUAL independently. That gave Deripaska the Russian aluminium monopoly. But a year later, in 2007, Deripaska risk prevented the LSE listing that was attempted. This risk, as the underwriting and advising banks explained it at the time, comprised two parts.

The first was that Deripaska was a trustee for others, and didn’t lawfully or in practice own all the shares he claimed to own. This was, and still is being tested in the UK High Court, where the banks have reason to fear the court will rule in favour of Michael Cherney’s (Mikhail Chernoy) claim to a 13% shareholding in Rusal, held by Deripaska on trust for Cherney since 2001. The second of the Deripaska risks was that Deripaska’s business practices exposed Rusal to being nationalized by the Kremlin. When the London IPO attempt was abandoned on these grounds, Deripaska tried again in 2008 in Shanghai and Hong Kong, but failed for lack of Chinese buying interest.

Now that he appears to be failing once more, for the two London reasons, plus a third — Rusal’s indebtedness – the state concession itself is threatened with asset breakup along the metal production chain; massive loss of Russian employment; and long-term destruction of creditworthiness. Arguably, Medvedev might have said to Sechin – look what your boy has gotten us into? Arguably, Sechin might have replied – mind your own business. To which, arguably, Medvedev might have retorted – if there’s no listing, you and I won’t have an aluminium business to mind.

In this clash of person and interest, Kudrin represents the treasury interest. No ideologue, Kuchin is the tightwad of the state who is disinclined to release funds and add liabilities, unless they are fully secured. So what he was saying on November 25, for the first time, was that if Putin and Sechin agree to a new VEB bailout – at least 3% of the Rusal shareholding – that should be secured by something that hasn’t been touched before — Deripaska’s personal assets, his personal shareholding stake. There aren’t so many Rusal assets left with which to secure fresh loans, and shares are non-secured stakes, whose valuation is disputable in the marketplace, and much lower as security for a new bank transaction.

And so, what Kudrin appeared to mean was that if the Hong Kong IPO goes ahead, and the state, through VEB, is to be the anchor investor, and largest share buyer, Deripaska would have to give up his personal shareholding control, and that he would be subject to state control from now on.

But other Russian banking sources already believe that Deripaska did this some time ago, at least not later than the point at which the rival oligarch group, Mikhail Fridman’s Alfa Bank group, began its attack on the assets and filed for court-ordered bankruptcy and transfer of operational control to someone new. In this contest, Medvedev has publicly tried to defend Deripaska from Fridman. Fridman has consequently been deterred; but not by Medvedev’s intervention alone. The conclusion the Russian sources draw is that Deripaska has arranged a protective trusteeship with Sechin as well. Kudrin appears to have wanted this to be understood publicly.

Until the point at which the HKEx delayed approval of the listing, Deripaska’s IPO strategy was a desperation measure to deal with the risk to his own shareholding of a state takeover. If, Deripaska appears to have calculated, he could find a strategic investor or two abroad, then he could recruit them to preserving his personal control of the company, and thereby pit them against the state shareholder trust at home. The evidence is clear that Deripaska tried to draw in state-sponsored shareholders from China, Malaysia, Singapore, Libya, and indirectly, through the Paris and New York banks, two other sources – the French and US governments.

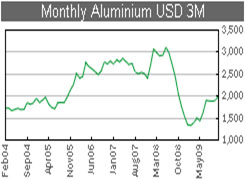

The one company valuation that has leaked out of this process is $19 billion, which, according to a source close to the offer, was indicated to the Libyans. That means that Deripaska has been trying to persuade someone to give him a fresh $1.9 billion, and allow a start to clearing Rusal’s foreign bank debts; with the promise of a steady increase in Rusal’s equity value as the price of aluminium price goes up. One technical speculative problem – during November commodity aluminium rose over $2,000 per tonne in the international maket, and is now headed downward again.

| This is a big gain over the sub-$1,500 price at which it was trading at the start of this year. But it is nowhere near the $3,000 peak before last year’s crash. If the aluminium market experts don’t believe there is sustainable demand to keep aluminium at $1,900 to $2,000, and if lagging demand for the metal will add substantially to the surplus of aluminium next year, then the only direction for Rusal equity value next year is not up, but down. |  |

Now offering stakes of strategic Russian resource companies to the US is a dangerous business, as Mikhail Khodorkovsky has had six years so far to ruminate on in a Siberian prison. There is no direct evidence that Deripaska paid his two calls this year to the US for the purpose of selling Rusal to the Americans, but there are indirect hints – the meetings he is reported to have had with the New York investment banks; and his statement, on a BBC television interview in the summer, that he had been approached to betray Russia to the Americans, and had resisted.

Last week, Kudrin desired it to be known that Deripaska had met a second test of his patriotism. His resistance to the new terms of a Russian state purchase of Rusal shares is at an end also.

Leave a Reply