By John Helmer, Moscow

For Russians to eat as much cheese as they want, there aren’t enough cows in Russia, and too many palm trees in Malaysia. The impact of year-old sanctions in cutting off the flow of imported cheese from Russia’s suppliers in Europe is to stimulate the production of domestic cheese. But at the same time Russian cheesemakers face a lack of raw milk supplies. To feed the market, palm oil is being used instead for products the Russian dairy industry is calling fake. If the Russian milk supply is to match rising demand, then Russian farmers and traders say the government must subsidize the cost of domestic milk production and deter palm-oil substitution.

“Adulteration by palm oil and bad politics behind sanctions have produced an impossible position for the dairy producers,” says an independent dairy farmer near Moscow. “Today we cannot produce enough affordable cheese for the masses! In provincial supermarkets and shops pseudo-cheese is being sold at Rb500 to Rb600 a kilo. This is impossible when the average supermarket insists on its mark-up of 100%. For one kilo of genuine cheese you need 10 to 11 litres of milk. That means a minimum cost for one kilo of cheese of Rb300 – and that’s just the cost of the milk.”

Reporting by the Institute for Agricultural Market Studies (IKAR) in Moscow shows that before the sanctions war against Russia began in the second quarter of 2014 Russian dairy production had started tentatively to revive, although the numbers for the dairy herd and milk volume were nowhere near the numbers before Boris Yeltsin took power in the 1990s. They were still below those of the last domestic economic crisis of 2008-2009.

NUMBER OF RUSSIAN CATTLE (blue), SIZE OF HERD (red), 1990-2014

Source: http://ikar.ru/research/195.html

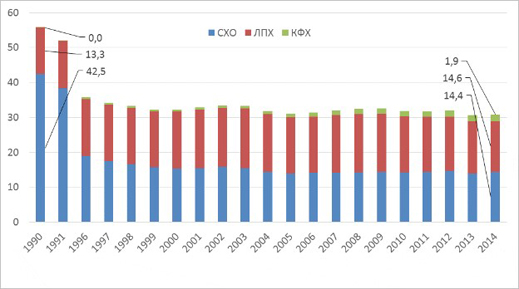

RUSSIAN GROSS MILK OUTPUT, 1990-2014

(in million tonnes)

Key: Blue = agricultural organizations, including state

Red = private farms, unincorporated individual farmers

Green = private farms, sunincorporated collectives

Source: http://ikar.ru/research/195.html

The reason for the growth of domestic milk output while herd numbers remained static is that the milk yield per cow has been improving with better feed, better farming methods, more working capital for farmers, more cash investment. One farm source qualifies this interpretation: “I do not trust IKAR statistics as these are based on regional oblast data, which are very often corrupted in order not to lose status or displease higher-ups! Only a few weeks ago the Ministry of Agriculture admitted that milk production is falling, as is the size of the national herd.”

OUTPUT OF MILK PER FARM COW, 1990-2014

(in kilogrammes)

Source: http://ikar.ru/research/195.html

US and European Union (EU) sanctions against Russian individuals started in March 2014. They were formally extended against Russian companies and banks in July. Before then, though, capital sanctions against Russian companies and banks, and against stockmarket trading in their shares and bonds, were introduced informally by the US Treasury.

The Russian Government reacted with counter-sanctions, starting with Australian meat and then extending to imports of most foodstuffs from the US, Canada, the EU states, as well as Ukraine. The Netherlands and Finland were the hardest hit of the EU exporters of cheese to Russia. The details of the counter-measures announced on August 7, 2014, can be read here.

According to the IKAR reports, the impact was a dramatic fall in imports of dairy products. Overall for the year 2014, imports of cheese and cheese products decreased by 35% compared to 2013 However, in the , final quarter, September through December, the decline in cheese import volumes was 63.5% compared to the same period the year before. The EU and Ukraine, which had dominated the Russian market with 74% of the imported cheese, were out.

Belarus stepped into the gap; its export volume of cheese to Russia was declining in the first half of 2014, but this revived rapidly in the second half. For the full year, Belarus was the main cheese supplier with almost 98,000 tonnes. The Netherlands and Finland ended the year with 24,953 tonnes and 18,894 tonnes, respectively. Argentina gained sharply, ending the year with shipments of 18 562 tonnes; that’s an increase over 2013 of 152%.

Domestic manufacture of cheese also increased during 2014 by 15% over the previous year. . The year-on-year rate of growth for Russian cheese output had been running at 11% to mid-year; in the December quarter this accelerated to 24%. But dairy farmers warn – this was growth of pseudo-cheese; that’s to say, processed cheese made with vegetable fats, mostly from palm oil imported from Malaysia and Indonesia.

Russian customs data show that so far this year the palm oil import volume has been jumping by 16%. For more details on the fight over palm oil and pseudo-cheese, read this. For the favour the Kremlin has shown foreign companies Danone and PepsiCo in their takeover of the Russian dairy industry, click open. It has been these two companies which have driven the lobbying campaign in Moscow against adulteration, in large measure to drive out of business the smaller and midsize Russian producers of dairy products, including cheese.

IKAR reports the trend to import substitution which has followed the sanctions war isn’t all good news for Russian cheese. “It’s too early to draw optimistic conclusions. Despite a significant reduction in the supply, by the end of 2014 the price for 50%-fat Russian cheese soared by 33.4%, compared to the year earlier. This was the result, not just of the reduction of market supply, but also of the increase in the cost of production on the market. Import substitution which we often talk about, is impossible as long as the market remains in a deficit of raw milk. Especially since the growth of cheese production was due to the decrease in the production of other, lower margin [processed cheese] products from the milk.””

IKAR’s forecast for 2015 is more optimistic, with a 10% to 15% growth in Russian cheese manufacture, and a gradual decrease in domestic cheese prices.

The Russian state statistics agency Rosstat reports that domestic output of cheese and cheese products in the four months, January through April 2015, reached 180,000 tonnes, a gain of of 29.5% compared to the same period of 2014. This was significantly faster growth than the production of red meat, up 13.5%; poultry, 12.7%; sausage products, 0.6%; fish and fish products, 6%.

IKAR’s chief expert for the dairy sector, Alim Ayubov, calculates that this year the domestic cheesemakers require an extra 1.1 million tonnes of raw milk to meet the production growth target for cheese output. “In fact, the increase in the raw material base for all types of farms shipping raw milk to the processors has amounted to 420,000 tonnes.” Ayubov says IKAR is calculating that this year Russian consumption (counting production, import and export) of cheese this year will come to 770,000 tonnes. This is down from 785,000 tonnes last year, and 840,000 tonnes in 2013.

The Russian consumer watchdog, Roscontrol, warns that cheap cheese is fake cheese. Dairy farmers warn that the substitution of imports of genuine cheese is being managed by increased imports of palm oil for the production of pseudo-cheese. In July, Alexander Borisov, the co-chairman of the Russian Consumer Union (Roscontrol) announced the results of a sampling of cheese products which his organization had conducted. Nearly 70% [of the sample] was fake, he reported, and consumers were being deceived. According to the Roscontrol report, cheese manufacturers are increasingly replacing milk fat with vegetable fat, including palm oil. All the popular types of domestic Russian cheese can be made with palm oil.

Andrei Danilenko, head of the National Union of Milk Producers (Soyuzmoloko), agrees there is a high level of falsification in the labelling of cheese products on Russian store shelves. However, he said by total volume of supplies going into domestic cheesemaking, faking with vegetable fats accounts for no more than 20%. He said the government has agreed to raise the fines for violations to a deterrent level.

Sources in the palm oil trade accuse the Russians of discriminating for political reasons against imports from Malaysia and Indonesia. An independent trader says there are real problems of shipment hygiene. “I am very prepared to believe that they don’t clean the tankers properly between shipments in the Russian case.”

Soyuzmoloko is coy about the underlying dynamics of the cheese market. This year, the association acknowledges that there is more domestic raw milk. “Small growth there seems to be — 2.4% in the first half of the year. But this is clearly not sufficient to ensure the accelerated pace of production from the cheesemakers. So it is not entirely clear how the domestic abundance of cheese can occur.”

At IKAR Ayubov says the biggest market share for milk processing is taken by Pepsico, which owns the Wimm Bill Dann brand production line, and Danone which owns Unimilk. Danone doesn’t produce cheese in Russia; PepsiCo launched its first cheese product, Lamber, in May of this year. “In the cheese market the largest player is the foreign company Hochland Russland, but it is engaged in the production only of processed cheese. The other cheese companies are mainly domestic, with no clear leader and noone with a market share of more than 5%.”

The country’s largest dairy producer, Belebey Dairy Plant in Bashkortostan, says that over the past five years it has been increasing its output by 15% to 20% per annum.

Belebey is producing Russian-branded substitutes for French Belfort and the American Belster type. Source: http://www.bashinform.ru/eng/773057/

In the first half of this year, Belebey says its growth rate is 16%.

The latest report from Russian Customs shows that import substitution for Russian cheese is overwhelmingly the substitution of palm oil for dairy milk. In 2013 the import volume of palm oil came to 746,560 tonnes. Under pressure from the regulators, it dropped to 706,325 tonnes in 2014. This year to September 30, the import volume was 614,170 tonnes. At the average monthly shipment volume, this marks a 16% rate of growth since last year.

Philip Owen of Volga Trader is a leading analyst and broker for the Russian farm sector and food trade. Volga Trader provides companies in the food supply industries with the means to enter the Russian market by finding importers, or by organizing investments. It has an operations centre in Saratov, and a sales office in Bridgend, Wales. For his forecast of the Russian cheese industry, Owen says: “I think Russia will struggle with import substitution. The problem is not just adding cheese- making capacity. The problem is also liquid milk supply. Russia has banned the import of liquid milk from the European Union, including formerly important suppliers such as Lithuania. This has not resulted in greatly higher prices at the farm gate because of the power of the milk processors and other parts of the distribution system. Without much higher prices at the farm gate, there is not much incentive for local investors to make the three-year investment in creating a new dairy herd with commercial interest rates at 20%. It is a different proposition for foreign investors with low borrowing costs. But the current political climate is not encouraging. For example, both the Saudi and Abu Dhabi sovereign wealth funds have withdrawn their investments of $10 billion and $4 billion respectively from the Russian Direct Investment Fund. In the Saudi case, that was within weeks of joining. The EBRD is restrained by the sanctions. China invests to acquire resources, not for financial return.”

Owen (right) acknowledges that “to some extent, Russia is able to compensate with imports of dried milk powder. However, the world’s primary source is the People’s Republic of China where there have been a number of scandals about adulteration. Countries like Uruguay, New Zealand and Pakistan are available as alternative suppliers of milk powder and cheese. But there are still issues of approval and indeed capacity. As in the pork business, foreign processors do not like to be over-dependent on a single country as a customer.” Veterinary health certificates and import permissions are required. These tend to deter middle sized producers.”

Owen (right) acknowledges that “to some extent, Russia is able to compensate with imports of dried milk powder. However, the world’s primary source is the People’s Republic of China where there have been a number of scandals about adulteration. Countries like Uruguay, New Zealand and Pakistan are available as alternative suppliers of milk powder and cheese. But there are still issues of approval and indeed capacity. As in the pork business, foreign processors do not like to be over-dependent on a single country as a customer.” Veterinary health certificates and import permissions are required. These tend to deter middle sized producers.”

“A comparison between the shelf space devoted to cheese and other dairy products in a UK supermarket and a Russian supermarket will tell you that less cheese is sold per capita in Russia.From memory Russian consumption is about 6 kg a head.”

Data for 2013 – source: http://npaper-wehaa.com/cheese-reporter/2013/10/s2/#?article=2050715

According to Owen, “there are alternatives to hard cheese on the Russian shop shelf, in particular different varieties of cottage cheese—tvorog (pictured below), for example. Kefir competes for the same consumer spending. Even so, the cheese shelf in a produce store in the Russian provinces does not offer a lot of variety. In Saratov, there will be 2 or 3 local producers making more or less the same product. There is a large latent opportunity to sell more cheese, not only for import substitution but in places where imports weren’t very strong in the first place.

“Russian cold chain distribution still leaves something to be desired. National distribution is therefore difficult and expensive so national brands struggle to develop other than through the big supermarkets but they have half the market share of supermarkets in the UK.

“Large scale cheese production for a national market needs investment in a bigger dairy herd and temperature-controlled distribution systems. It is not just a case of building new processing plants. The first step is to direct more profit to farms so that they can afford to increase milk production.”

An independent dairy farmer in the Moscow region says the palm oil substitute is a short term expedient. The domestic dairy farmers cannot expand their production to fill the gap – “not in a short period of time. This will take 5 to 10 years. Also, a stable system of federal assistance is needed, particularly in the cost of credit, but then we have the restrictions of the World Trade Organization (WTO). So we should leave the WTO!”

Asked what policy he recommends for the Kremlin to stimulate domestic production of milk for cheese-making, he said: “15 to 20 years credit with subsidised interest rates from Government and a policy to subsidize milk per litre.”

Roscontrol points out that domestic dairy producers and cheesemakers suffered unfair disadvantage from the heavy subsidies which the EU has been paying to their exporters. Removing the EU products from the Russian market helps equalize the competition.

Proposed government regulation of product labelling will also help, says Ayubov of IKAR. “Information characterizing the content of the milk-product of palm oil or milk fat substitute made with palm oil, must occupy at least 30% of the total area of the product label and (or) the front of the consumer packaging . This information is to be put in capital letters in black on a white background — bold, clear, easily readable, with a font size as large as possible. Line spacing should not exceed the height of the font. Information should be evenly distributed across the area bounded by the frame.”

“If the draft is adopted, and its implementation carefully monitored,” Ayubov adds, “it can be expected that in the next two years, raw milk prices will go up, and we will see significant increase in the demand for it. This will allow the industry to move towards positive profitability, thus multiplying the number of investment projects in dairy cattle. Yes, the prices for dairy products will increase even more; the production of finished products will be reduced, as well as consumption. However, only in this case can we talk about import substitution. This is now much more important than the volume of cheese production, and the increase in raw materials.”

Vadim Gitlin (right), executive director of Roscontrol, says: “It is no secret the EU heavily subsidized farmers and dairy production costs. As a result, lower-quality products often fell on our tables just because the price was more attractive. Losing out in this competition, the domestic manufacturer could not evolve to increase his production, or lower his prices by reducing the cost of the manufactured product. European dumping pushed the Russian producer, not to withdraw from the market, but to make his products affordable by using lower quality components. Now, in the market when the share of imported goods has fallen, we can see increased production of Russian natural cheese. Yes, both dairy fat and fake, but the market is now open to a good product at a reasonable price.”

Vadim Gitlin (right), executive director of Roscontrol, says: “It is no secret the EU heavily subsidized farmers and dairy production costs. As a result, lower-quality products often fell on our tables just because the price was more attractive. Losing out in this competition, the domestic manufacturer could not evolve to increase his production, or lower his prices by reducing the cost of the manufactured product. European dumping pushed the Russian producer, not to withdraw from the market, but to make his products affordable by using lower quality components. Now, in the market when the share of imported goods has fallen, we can see increased production of Russian natural cheese. Yes, both dairy fat and fake, but the market is now open to a good product at a reasonable price.”

Ayubov of IKAR concedes that cheese “has always been a product that not everyone can afford. That is why we have such a high proportion of processed cheese. Now the situation has worsened considerably. People have begun to save on everything. A case in point — the physical volume of cheese wholesaled in Russia has decreased by 10%.”

At Roscontrol Gitlin is forecasting investments in Russian dairy production to grow. “Over the next two years we will see the trend of growth in the domestic production of cheese. Competition will gradually increase, as imports from other countries [Latin America], too, will grow, but at a slower pace than before. As for the cheese produced with the use of vegetable fats this will also increase its market share by offering Russians a cheaper product. But the planned tightening of labeling will allow consumers to make informed choices about what they want to buy — cheese or cheese product. In the next five years, against the background of the strengthening of the supervisory role of the state and public consumer control, we expect growth in the production of high-quality Russian cheese, though this will require a lot of effort.”

Leave a Reply