By John Helmer in Moscow

How much gold should potential investors in Alexei Mordashov’s gold-mining venture, now named NordGold, think they are buying into?

The question arises because the gold equity market assigns exponential gains in enterprise value, and hence share value, when the volume of unmined gold reserves rises above the conventional thresholds of small, medium, large, and mega. Mordashov’s NordGold is trying to climb fast on this ladder, as the proprietor prepares the company’s assets for an initial public offering. So Mordashov’s latest announcement that his venture has hit the 22 million troy ounce level is an invitation to investors to increase their valuation, before the IPO is launched.

It is possible that the delay in the IPO past the close of this year’s issue deadline reflects a relatively low valuation – and a lack of imagination or confidence on the part of investors.

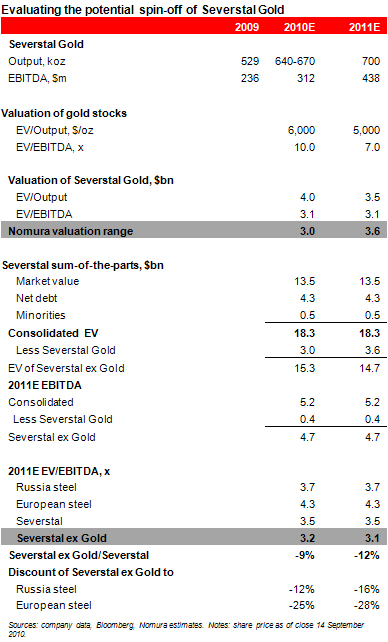

When Vladimir Zhukov of Nomura published his estimates last month, he concentrated on actual gold production and proven reserves. “Severstal Gold,” he reported,, “holds 12.5moz of gold in measured and indicated resources, most of which are contained in the West Africa (8.4moz), followed by Russia (3.3moz) and Kazakhstan (0.8moz).”

Here is how Zhukov estimated the potential IPO value of the company:

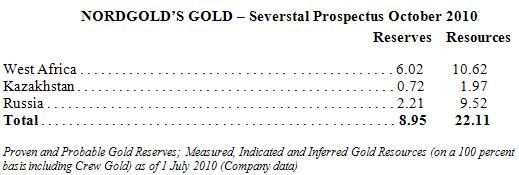

So how come, investors ask, did Mordashov arrive in this week’s Severstal loan note prospectus at this calculation of the reserve base at almost double the earlier number: “NordGold has approximately 22.1 million ounces of measured, indicated and inferred resources according to JORC as of 1 July 2010, most of which are equally distributed between West Africa (44.0 percent) and Russia (43.0 percent) with the remaining 13.0 percent located in Kazakhstan.”

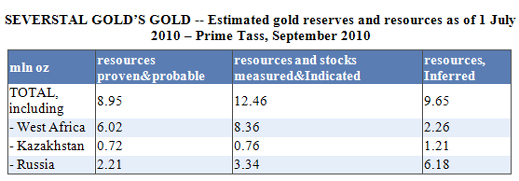

When the NordGold and Severstal spokesmen in Moscow are asked to clarify this calculation, they decline to respond. This is more bad temper than a want of transparency on the company’s part. For the difference isn’t difficult to spot. It is in the figure for gold that hasn’t been proven yet, but is reported as either indicated or inferred. Here are two company-authorized versions of the additional count which have been issued:

It’s plain that the second table skips over the category of measured and indicated gold, and peers straight into the black hole of inferred resources. This multiplies the gold count total by 2.5 times. Taking Mordashov’s portfolio region by region, it can be seen that the West Africa count jumps by a magnitude of 1.8. The Kazakh count jumps by 2.7 times, while the Russian count is multiplied by almost the same factor – 2.5 times.

So, what is happening to NordGold’s value is deep under the ground – and more in the Russian and Kazakh underground than the West African, if numbers and multiples like these have any meaning. But that’s the point – what value should be attributed to the non-proven magnitudes and multiples?

This is how the latest Severstal loan note prospectus describes the position: “NordGold currently operates eight productive mines in Burkina Faso, Guinea, Kazakhstan and the Russian Federation. The Taparko mine in Burkina Faso, as well as the Irokinda, Zun-Holba and Berezitovy mines in the Russian Federation, are owned through High River Gold, in which the Group holds a 70.4 percent controlling interest [increased to 72.6% , according to an October 11 announcement] and the LEFA mine in Guinea is owned through Crew Gold, in which the Group holds a 93.4 percent controlling interest. NordGold maintains a 100.00 percent interest in each of the Neryungri, Aprelkovo and Suzdal mines, located in the Russian Federation. NordGold organises its business across three core regions:

West Africa:

• Somita: Comprises the Taparko mine in Burkina Faso, an open pit gold mine consisting of three open pit deposits. In 2009, this facility produced 97.7 Koz of gold.

• Crew Gold: Comprises the LEFA mine in Guinea, an open pit gold mine consisting of two material open pit deposits. In 2009, the mine produced 178 Koz of gold.

• Development West Africa: Comprises a number of properties in the development and exploration stage located in West Africa. The key development project in West Africa is at Bissa, which is expected to begin production in 2013. The Group also has over 30 exploration permits in Burkina Faso, where exploration works are being carried out, and the assessment of exploration potential by Crew Gold in Guinea is currently underway.

Kazakhstan:

• Celtic and Semgeo: Comprises the Suzdal underground gold mine in Kazakhstan and gold deposits in the auxiliary open pit gold mines of Zherek and Balazhal in the vicinity of Suzdal, which are currently under technological review and exploration. In 2009, this operation produced 114.7 Koz of gold.

Russia:

• Berezitovy: Comprises an open pit gold mine located in the Amur region of the Russian Federation. In 2009, this operation produced 87.3 Koz of gold.

• Buryatzoloto: Comprises the operations of Zun-Holba and Irokinda, two underground gold mines, located in the Buryatia Republic of the Russian Federation. In 2009, this operation produced of 154.6 Koz of gold.

• Neryungri-Metallik and Aprelkovo: Comprises open pit gold mines in the Republic of Yakutia and Transbaikal region of the Russian Federation. In 2009, this operation produced 79.1 Koz of gold.

• Development Russia: Comprises properties in the exploration and evaluation stages located in the Russian Federation.”

That last item contains a very big unknown, and also a big push on the value of the entire table.

This is the Prognoz silver deposit in the Sakha republic of fareastern Russia. The story of the current litigation between Mordashov and the 50% owners of Prognoz has been reported here. And so has the jump in proven, inferred and suspected resources at Prognoz. The Canadian regulation compliant reserve and resource estimate, prepared by Micon in 2008, was for almost 111 million oz of silver. But additional drilling and sampling, which has yet to be carried out at Prognoz, have suggested resources of between 94 million to 194 million oz. Converting these numbers at the current silver to gold price ratio, Prognoz may hold a mineable gold equivalent reserve from 1.94 million oz to 5.34 million oz. But then again it may not.

If Mordashov aims to persuade investors that his NordGold is worth a lot more than he’s been given credit for so far, he appears to be including a sizeable Prognoz count. This is not only unproven geologically; its ownership is also undecided between powerful Russian partners who are still slugging it out with Mordashov in court.

Leave a Reply