By John Helmer in Moscow

Gennady Timchenko and his allies in state-controlled companies in the Russian oil business are gradually consolidating their dominance over much of Russian oil from the wellhead to the tanker enroute to international markets, and much of the transportation network in between. As the largest energy exporter in the world, Russia naturally aims to be a reliable supplier to its clients. And Timchenko, who lives in Switzerland and France and reportedly carries a Finnish passport, is by all accounts a very reliable fellow. The London law firm Schillings vouches for him – and that says a lot.

It was thus no surprise when Kommersant, a Moscow newspaper, reported today that Timchenko’s group of companies may be the strategic investor and purchaser of the 50% shareholding which the Russian Railways Company (RZD) is planning to sell in its affiliate, Freight One, as it is known in English; or First Cargo Company (PGK) as the subsidiary is also known in Russian.

If that were to happen – take a deep breath — Timchenko would add PGK, which controls about one-third of the rail transportation of oil in Russia, to Transoil, a company he already owns, which has a share in the same market of about 5%. He also has been building substantial stakes — direct, indirect, allied – in the Primorsk, Ust-Luga, and Novorossiysk oil export terminals in western Russia, and in Kozmino Bay, in the fareast. His Geneva-based Gunvor group is one of the most powerful traders of oil for Rosneft and other Russian producers and exporters. Also, he is rumoured to be a likely bidder for the state’s 20% shareholding in the state oil tanker monopoly, Sovcomflot, when that is privatized next year.

Just how Timchenko came by his interests in the Russian oil transport market can be found in thousands of pages of testimony and cross-examination from the UK High Court proceedings in a case brought by Sovcomflot chief executive Sergei Frank against his predecessor, Dmitry Skarga, and others against whom Timchenko turned.

You may now breathe out — for there is no certainty that Timchenko has been selected by RZD as its preferred partner to run the oil car and rail tanker business. PGK’s spokesman told Fairplay: “It’s up to RZD to decide, because we are a 100% subsidiary”. At RZD, the spokesman confirms the remarks made yesterday by senior vice president Valeriy Reshetnikov, when he announced that the 50% shareholding in PGK will be sold off. Reshetnikov also reportedly said that the majority bloc of shares in PGK will be sold to a “strategic investor”, and that the decision to authorize the transaction had been taken “at the government level this spring.”

RZD, said Reshetnikov, “is relinquishing control in favour of a strategic investor. We will retain a blocking stake, but we should not take part in operational management.” A blocking stake in Russian practice is customarily no more than 25% plus one share. So the implication of Reshetnikov’s remarks is that the state stake in PGK will be even further diluted, making the takeover by the strategic investor tantamount to operational and financial control.

A Transport Ministry source is quoted by Kommersant as saying something slightly different. There are several options for the privatization, the ministry said through an anonymous spokesman. “The proposals come one after another. They are all discussed. But at this stage the final form has not yet been determined.” The ministry source told the newspaper that after the “strategic investor” takes over the 50% stake, RZD may float and sell another 25% of the shares in an initial public offering. That may put the strategic investor in the advantageous position of paying a discounted price set by the government, before public sharebuyers have to bid in the open market. No value for PGK has been fixed for either sell-off, but the newspaper claims Freight One-PGK may be worth a total of $5 billion.

RZD refuses in its comments on the speculation to identify Timchenko as the strategic buyer of PGK. This response implies that Reshetnikov’s reference to a strategic investor is correct. Other published speculation points to a rival bidder from the oligarch ranks – Vladimir Lisin, the steel magnate who already controls port outlets for his metal exports.

The Kommersant report also refers to a fight over jobs between those who currently run RZD’s freight subsidiaries and the placemen Timchenko is believed to want to put in their place; that is, if he takes control of PGK. These personal rivalries appear to have triggered parts of the press report with the aim of mobilizing an alliance of interests to compete against Timchenko.

Igor Romashov, the figure purportedly identified as the favourite to take over at PGK, if Timchenko buys the company, is a veteran oil mover. He was chief executive of Transoil from 2003 to 2006; then in charge of the Federal Agency of Railway Transport until 2008, when he became a senior vice president of Rosneft. When contacted by Kommersant, he said he hadn’t been offered a new job at PGK. His apparent rival is Salman Babayev, more a veteran railwayman than an oil mover, who currently heads Freight One-PGK and is thus most directly threatened by the “strategic investor”. Babayev says there hasn’t been any discussion of his leaving his present job, although the subject of his expiring employment contract there is apparently on the agenda for a board meeting at RZD headquarters later this week.

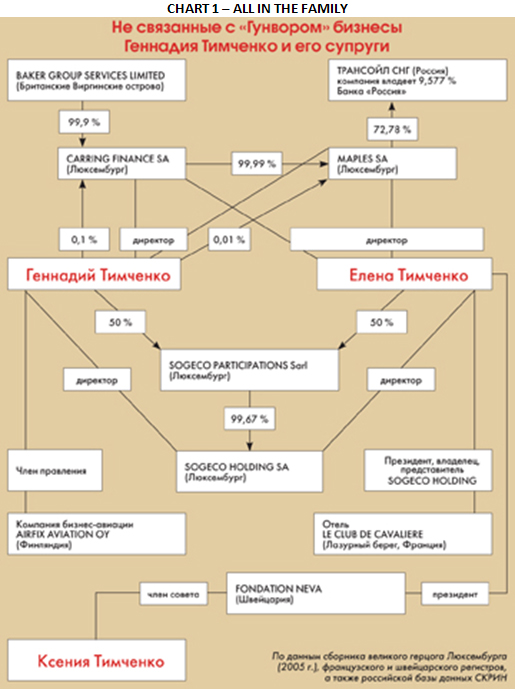

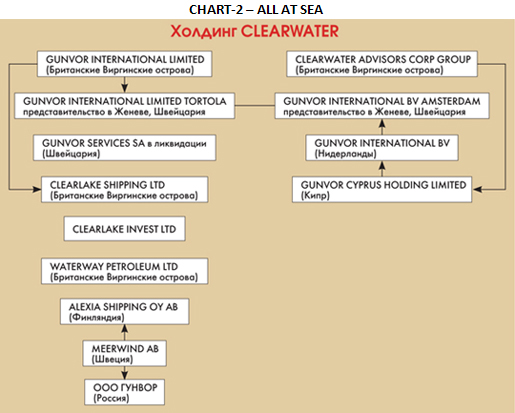

Experts in the Russian oil transportation industry generally bite their tongues when it comes to talking about Timchenko and his interests. When Novaya Gazeta, a Moscow publication, reported last year on the Timchenko family businesses (chart-1) and the shipping company network (chart-2), Timchenko’s lawyers threatened criminal prosecution.

Timchenko’s Transoil is currently estimated to own 35,000 tank cars which operate in a relatively restricted geographic region between the Kirishi oil refinery, in the Leningrad region east of St. Petersburg, and the Gulf of Finland and Baltic coastal ports. Freight One-PGK operates 77,000 tank cars, while RZD operates another 190,000. The main destinations for PGK’s oil cargoes are the Baltic coastal ports, Poland, Finland, and in the east, Mongolia and China.

According to the most recent financial and operating reports, PGK carried 49.9 million tonnes of oil and products in the first eight months of this year; that total is up 19% on the same period of 2009. In 2009, total cargo volume for PGK – including oil, ores, metals, fertilizers, cement and other construction materials – amounted to 232 million tonnes. Compared to the crisis year of 2008, when Russian exports and domestic demand plummeted, this cargo volume was almost up 190%. Oil transportation volume in that period was 62.1 million tonnes, making 27% of the aggregate.

RZD operational reports indicate that by counting the number of oil cars, RZD holds 52% of the market in Russia; PGK, 33%; BaltTransService, 7%; Transoil, 5%; and Transleasing, 3%. For more details of Russian oil movement to the export and domestic markets, click here.

Maria Chernova, spokesman of the Federal Antimonopoly Service(FAS), told Fairplay that her agency has yet to hear from RZD or Freight One for authorization of the sale of the majority shareholding. While she said she doesn’t know who the strategic purchaser may be, she added that if he or the purchasing company is not Russian, the Law on Foreign Investments would require a review of the transaction by the Foreign Investment Review Board. That is chaired by Prime Minister Vladimir Putin. In March of 2009, the London Times reported that “we stated wrongly that Gennady Timchenko is a close friend of Vladimir Putin…The true position is that, though Mr Timchenko and Mr Putin do know one another, the relationship is more one of casual acquaintanceship than of friendship or of the two men being ‘close friends’.”

Moscow maritime analyst Alexei Bezborodov commented: “Until there is a government ruling [on the sale], it’s nothing but a PR move”.

RZD told Fairplay: “The sequence [of the transaction] is the following. First, the RZD board makes a preliminary decision on the stake’s sale. Then the company turns to the government for approval, and this stage could take up to a year, maybe faster. Only then the company turns to FAS. We cannot say if [the purchaser] will be a foreign or a Russian company. But probably a Russian one, because railway transportation is a strategic sector.”

Dmitry Adamidov, a transport analyst with Investcafé in Moscow, told Fairplay: “We won’t be able to call Timchenko a monopolist in the classical sense of the word. The fact is that almost all the major oil companies also own a park of tank cars, or have a stake in a transport company. Periodically they think about selling non-core assets, but if the transport companies raise their prices, the oil companies quickly revive the projects of their own transport companies. Therefore, even after taking a monopoly position in the market, any company will have to be very careful in dictating prices.”

Leave a Reply