By John Helmer, Moscow

Oleg Deripaska is running out of friends who stick up for him, especially at the Finance Ministry in Moscow and the Federal Tax Service.

Deripaska doesn’t deny that the practice of tolling, through which his United Company Rusal has saved at least $5 billion in tax payments to the Russian treasury over the past decade, is a boon. But he claims this is lawful. More, he claims it is approved by the Russian government. On the other hand, for the first time this month, the alignment of domestic political forces in Moscow has approached the point where officials dare to say aloud that Rusal’s tolling is a form of stealing.

The evidence of this ties Rusal’s tax liability to the UK High Court case, in which Deripaska’s former partner and founding stakeholder, Mikhail Chernoy (Michael Cherney), charges that a complex scheme of tolling and trading aluminium was devised by the two of them in the 1990s, and then used by Deripaska to corner the profits entirely for himself.

If Russia’s taxman is serious about collecting what Rusal owes, the evidence is now publicly available to him — not in Moscow where Deripaska may have retainers or friends, but in London where there are none.

According to the All-Russia Tax Forum, convened by the Russian Chamber of Commerce and Industry, tolling by an offshore-registered company like Rusal substantially lowers the tax paid in Russia, and for that reason the forum speakers declared that it should be banned. According to Gennady Gudkov, a deputy of the State Duma, who spoke at the conference, “tolling [is a] semi-criminal scheme, which compromises Russia.” Gudkov is a former KGB officer and a two-term representative of the Kolomensky district in the Moscow region.

Raisa Karmazina, a Duma deputy from the Krasnoyarsk Krai, said at the same conference that Rusal cheats the regional budget of more tax revenue today than it did a decade ago. This growing shortfall has led to protests from Krasnoyarsk deputies, who held two debates on the Rusal tax theft in sessions of the Krasnoyarsk regional parliament in November and December. Anatoly Bykov, the former co-owner of the Krasnoyarsk Aluminium Plant (KrAZ), who has been victimized in the past by Deripaska, testified against him. Alexander Uss, the regional parliament speaker, and Edkham Akbulatov, the former acting governor of Krasnoyarsk Krai, said that the region was powerless to act — Rusal’s tax position had to be settled in Moscow, they said.

The Accounting Chamber, Russia’s independent federal government auditor, told the forum it is opposed to Rusal’s tax cheating. The Chamber auditor Igor Vasiliev testified that in audits the Chamber has made of Rusal operations between 2005 and 2008, falsification by Rusal of the value of exported aluminium amounted to at least half a billion dollars per annum. Vasiliev said he estimated that Rusal’s untaxed income shielded from tax through tolling amounted to more than Rb60 billion per year ($1.9 billion). In the decade since Rusal was established, Vasiliev said, losses to the state budget, including annual tax payments, interest, and penalties, now add up to $11 billion.

The Accounting Chamber confirmed that Vasiliev had spoken at the forum, and given these estimates. Vasiliev himself declined to say more. Contacted at their Duma offices, Gudkov and Karmazina also refused to answer questions.

It is no news that Deripaska is opposed by the former prime minister who heads the Accounting Chamber, Sergei Stepashin, and also by the former prime minister who heads the conference organizer, the Russian Chamber of Commerce, Yevgeny Primakov. Both men have had long career ties to the security and intelligence services. Until now they have lacked the power to challenge Deripaska’s protectors in the government.

Prime Minister Vladimir Putin is not unaware of the tax evasion problem. In July of 2008 he publicly attacked the practice of tolling or transfer pricing, although on that occasion he singled out, not Rusal, but coal exporter Mechel as the offender. In remarks televised on a Moscow evening news broadcast, Putin said: “I already mentioned at the meeting [on July 24] that one company was exporting its product at a fraction of the domestic market price. The domestic price was 4,100 rubles ($176), and they were selling it to themselves, across the border, for 1,100 rubles, and then selling the product for $323. It is a reduction in the tax basis inside the country. It’s not paying taxes, it’s creating a shortfall on the domestic market, which means an increase in the cost of metals production.”

Russian law treats a difference of 20% or more in the price of goods sold between the domestic and export branches of a company as unlawful transfer pricing. All Russian metals exporters have operated offshore trading schemes, which employ variants of the differential pricing Putin described. Under pressure of their share listing requirements in London or New York, the steel groups have consolidated their trading operations on to their main balance-sheets. But transfer pricing in steel and coal, and tolling in aluminium, have continued.

Tolling is a scheme for the exchange of imported inputs to metal fabrication, such as alumina, at a fixed price, for aluminium that is exported. The smelters earn a fixed fee; the offshore trader earns the difference between the smelter fee and the market price of the metal — without paying tax in Russia. It is lawful if the importing companies are not connected to the smelter companies and the exporters. But if they are all part of the same holding, the tolling scheme is at risk of charges of illegal transfer pricing by the government.

The Russian government’s tax-take from the metal exporters has been substantially below that for the oil companies, which are subject to a windfall profits tax. But as the government has decided to reduce taxes on oil companies, in order to create incentives to stimulate oilfield production, the revenue authorities propose to fill the gap on the revenue side of the budget by taxing the metals sector. This is exactly what the latest conference recommends will be served by the abolition of tolling by Rusal.

The last time Stepashin attempted this publicly was in July 2008, just ahead of Rusal’s crash into insolvency. The text of the Chamber’s public statement, issued at the time, explicitly referred to Rusal as benefiting offshore through the difference between “the high price of realisation of products of processing for the foreign market and the low cost of services in the processing of the Russian enterprises [smelters] and was not subject to taxation in the Russian Federation.” At the time, the Chamber statement estimated the revenue value to Rusal at $2 billion.

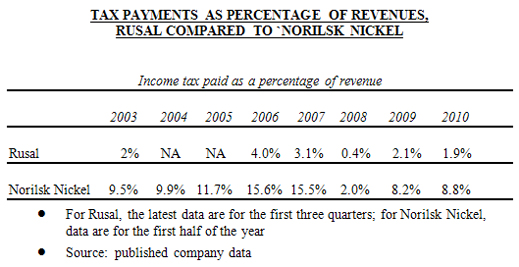

It is almost certainly more than that. The following table shows what the federal tax authorities discovered in a report to the government on September 6, 2004, when the percentage of tax paid to revenues declared was investigated for Rusal, along with other Russian metals exporters.

Conventional calculations of corporate tax rates rarely use this measure of income tax paid to recorded revenue. It was appropriate in the Russian case in 2003-2004, and since then, because these baseline numbers for sales revenue and income tax paid are more easily verified than other Russian balance-sheet numbers prepared by accountants and auditors.

What the table shows is that at 2% in 2003, Rusal was paying proportionally far less tax than its Russian peers. The comparison with Norilsk Nickel is included in the table because in Deripaska’s recent effort to take over Norilsk Nickel, he has been critical of the company’s balance-sheet.

As can be seen, Norilsk Nickel consistently pays roughly four times the amount of tax to the Russian treasury than Rusal. Reading across the table by year, it can also be seen – just as Deputy Karmazina said of the position in Krasnoyarsk Krai – Rusal is paying less tax today than it did in 2003. If the federal tax authorities were instructed by the Finance and Economic Developmernt Ministries to calculate what the effective tax rate for Rusal would have been, if the tolling schemes were invalidated, and if Rusal had paid tax at the peer benchmark rate, then the company would be liable to pay at least $500 million more per annum, or not less than $5 billion for the period through to the end of this year.

When word of Rusal’s minuscule tax rate leaked out in 2004, the company spokesman Yevgenia Harrison responded by acknowledging that Rusal was able to lower its tax rate by the use of tolling contracts with offshore companies it claimed not to own or control; and by a regional tax relief scheme for corporate affiliates registered in the fareastern region of Chukotka, where Rusal had no other business and negligible investment. Regarding the Tax Ministry report, Harrison said at the time Rusal was not under official investigation. “To dramatise what is a routine governmental report into an article that insinuates that Rusal has acted somehow improperly is misleading and damaging to the company’s corporate reputation; a reputation that we are working hard to develop as the company, and indeed Russia, moves forward.”

Harrison lost her job for disclosing more about tolling at the time than the company considered prudent. She was replaced by Vera Kurochkina, who was promoted by Deripaska to the Rusal board a few weeks ago. She too is under investigation.

When Rusal prepared its sale of shares on the Hong Kong Stock Exchange a year ago, the prospectus that was drafted and approved refers to tolling in three places – once in a statement of the group’s principal risks, and then, repeating what had already been said, in a section on sales; and finally, repeating for the second time, in a section on tax. What Rusal told prospective share buyers a year ago admits the riskiness of tolling, and the possibility that the Russian government will change its mind on the lawfulness of the scheme.

“The Group also uses tolling arrangements, mainly because a substantial portion of its alumina is sourced from outside Russia and processed by smelters in Russia, and the majority of third party sales of aluminium are outside Russia. Pursuant to the Group’s international tolling arrangements, a tolling company, registered and subject to taxation in Switzerland and acting upon instructions of the principal trading company of the Group, purchases materials, such as alumina, and arranges for their delivery to manufacturers, such as aluminium smelters, in another country for processing into end products, such as primary aluminium, in consideration for a tolling (or processing) fee. The title to the materials or end products is not transferred to the manufacturers and, therefore, where tolling is employed, the shipment of raw materials and end products into and out of the country of the manufacturer is not characterised as an import/export operation and is not subject to local import/export duties. The tolling company and the manufacturer are taxed on their respective profits in their respective countries of tax residence. This tax treatment of tolling arrangements in Russia is subject, among other things, to the requirement that imported materials are processed within a set period of time and, consequently, that finished goods are exported from Russia within that timeframe….

“Management intends to continue relying on tolling arrangements of the kind described above with respect to aluminium production in Russia when the alumina is sourced, and the finished aluminium is sold, outside Russia. Tolling arrangements are permitted under Russian law and the Group’s tolling agreements are regularly registered by the Russian customs authorities. The Directors believe that the Group’s tolling arrangements are conducted on appropriate commercial terms based on applicable Russian law and regulation….

“Russian transfer pricing rules effective since 1999 give the Russian tax authorities the right to make transfer pricing adjustments and to impose additional tax liabilities with respect to all “controlled” transactions, provided that the transaction price differs from the market price (upwards or downwards) by more than 20%. “Controlled” transactions include transactions with related parties, barter transactions, foreign trade transactions and transactions with unrelated parties with significant price fluctuations (i.e., if the price of such transactions differs from the prices of similar transactions by more than 20% within a short period of time)…The Russian transfer pricing rules are vaguely drafted, leaving wide scope for interpretation by Russian tax authorities and courts. There has been very little guidance (although some court practice is available) as to how these rules should be applied. … Certain amendments to the Russian transfer pricing laws and regulations are expected to be considered by the Russian legislative authorities and the new rules are expected to become effective in the near future. Such amendments, if adopted, are expected to result in stricter transfer pricing rules.”

The Finance Ministry, the Federal Tax Service, and the Duma Committee on Budget and Taxes were each asked to say what, in their interpretation, is the difference between lawful tolling and unlawful transfer pricing. For the time being, they have not replied.

Leave a Reply