By John Helmer, Moscow

Tod Browning was an American filmmaker of the early 20th century who suffered from circus obsessions, alcohol, wife and career troubles, which distracted him from showing an interest in the Russian revolution. While the Bolsheviks were planning their takeover of the Kerensky government, Browning made his first feature film. Called Jim Bludso, the story line was about a riverboat captain who sacrificed himself to save the lives of the boat passengers during a fire. It was a hit of sorts.

What made Browning’s lasting fame, but also his notoriety, plus the booze problem, was his interest in circus freaks. His only remembered film in our time, titled Freaks (see image), is about a fulsome woman who falls for a rich midget, spurning the not so well-off circus giant. But then she mocks her husband and his mini-mates, who discover that she’s trying to poison him and inherit his money. She suffers a gruesome end at their hands, along with the strongman. Her feet are melted to the appearance of a duck’s; the giant’s penis is cut off. To make such a film acceptable to American audiences of 1932, the horrid bits were cut out.

Polyus Gold, Russia’s leading goldminer, is a bit like that.

When one of its owners, Russian giant Mikhail Prokhorov (front row far right), this week admitted to feeling a little guilty for some of his company’s “mistakes”, the Moscow and London sharemarkets responded with thumbs down. Since Prokhorov removed his longtime subordinate, Evgeny Ivanov, and became chief executive himself on December 9, the Polyus Gold share price has started moving down – even though the price of gold has gone both up and down, and the Russian Trading System (RTS) index for the Moscow stockmarket has grown 3%.

One month Polyus gold share price chart

Why, Prokhorov was asked by a friendly Moscow newspaper this week, has he taken operational control at Polyus Gold? He answered: “In the near future there is a lot to be done with the company. Some important projects will require my personal strong involvement.” By this he means his attempt – announced through Bloomberg on December 8 – to secure a primary London Stock Exchange listing, and then sell out to “one of the leading gold companies in the world”.

Although Prokhorov has been chairman of the Polyus Gold board, and kept Ivanov on a very short leash, Prokhorov claimed this week, “some mistakes were made, flaws – now they have been corrected. I feel partially guilty that I did not ensure that management could work normally.” The blame, Prokhorov intimated, was either Ivanov’s, or Vladimir Potanin’s, but not his own. Potanin was Prokhorov’s onetime partner and co-owner of Polyus Gold. “I’m better than anyone else, [so I] will join the team. In regard to the withdrawal of the company to the international level [it] is critical to do so as soon as possible.” The evidence of Russian goldminers who have sold assets to Polyus Gold in the past is that Prokhorov always dominated Ivanov, and took for himself a bigger share of the succcess bonus than he allowed his CEO.

One of the questions the international miners have always asked when they have examined Polyus Gold is whether Prokhorov has been over-valuing the assets. Then there was the problem of asset-stripping, evidence of which was charged against Prokhorov and Ivanov by Potanin and independent shareholders during 2007.

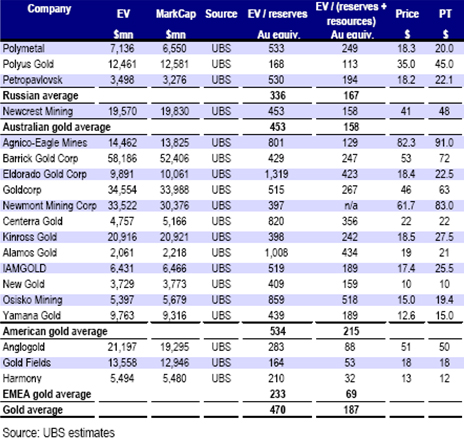

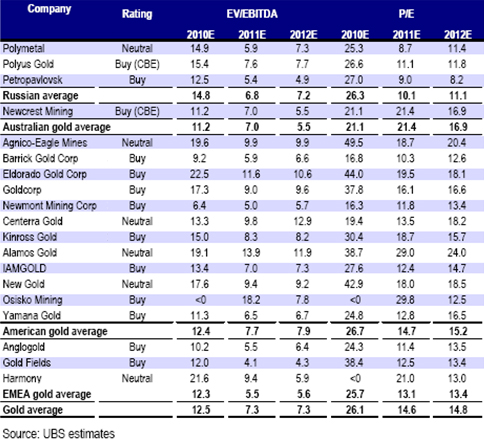

The bigger share of blame for mistakes like these, if they have happened, ought to be Prokhorov’s. At least this appears to be what the stockmarkets suspect. Since Prokhorov’s headlining of himself on December 9, Polyus Gold’s share price has been something short of a hit. But then comparing Prokhorov’s mining company to its peers, it’s dwarfed in relation to those internationals most likely to be interested in buying what Prokhorov says he is selling this time round. As this chart, prepared by UBS suggests, the share price to earnings ratio for Polyus Gold this year is projected to be 26.6.

Gold Fields of South Africa is at 38.4 (it was a takeover target of Prokhorov’s in 2004-2005); Kinross of Canada is at 30.4; it is the most likely buyer for Polyus Gold in Prokhorov’s mind. Newmont of the US, by contrast, is below Polyus Gold’s P/E at 16.3; Barrick Gold of Canada is at 16.8; AngloGold Ashanti at 24.3. Every one of them has taken years to look carefully at the possibility of joint venturing or buying assets from Polyus Gold. To qualify to mine Russia’s largest unmined gold deposit, Sukhoi Log in Irkutsk region, they have also judged that a powerful Russian partner would be necessary. But none of the internationals has been in a hurry to make commitments to Prokhorov, or give him their money to spend.

Prokhorov has also proved reluctant to spend much of his own on the biggest of Polyus Gold’s unmined assets – the Natalka deposit in the Magadan region. True, according to the company’s published statements, “Polyus Gold’s vision of Natalka provided for unique exploration opportunities and high possibility of substantial increase of its reserves.” And increase is exactly what they have been doing, the company says. In 2007, the reserves and resources were calculated at 59 million ounces of gold, with 48 million oz recoverable from the main mine pit at an estimated recovery grade averaged over the full mine life of 1.7 grams per tonne. International standard estimations have since put the big number at 68.6 million oz, with 41 million oz recoverable at a grade average of 1.13 g/t.

Despite the big numbers and their importance for Polyus Gold’s future gold production level, the company didn’t appear too keen to invest in the Natalka project or others it was carrying on its books. On September 24, 2008, President Dmitry Medvedev publicly chided Prokhorov and Ivanov for this: “I understand that it’s difficult for businesses to work, that we have an unwieldy bureaucracy, but don’t whine,” Medvedev warned. “If gold mining profits are too marginal for you, give up this work; we’ll find someone else. If you want, we can take the license back.” Link

Prokhorov’s next scheme was to improve the sell-off of his company by arranging a backdoor listing on the London Stock Exchange through a reverse takeover of the junior miner across the southeastern border, Kazakh Gold. This was also designed to remove Prokhorov’s gold business from close supervision by the Kremlin.

But the scheme turned into a two-year scandal in which the blame for alleged asset theft, diversion of more than $220 million in Eurobond and shareholder funds, and fraudulent gold production and reserve claims has been firmly planted on the Assaubayev family, the selling shareholders of Kazakh Gold. This affair was recently settled on terms that leave the Kazakh Gold registration in Prokhorov’s hands, where he wanted it; and the Kazakh assets and liabilities with the Assaubayevs.

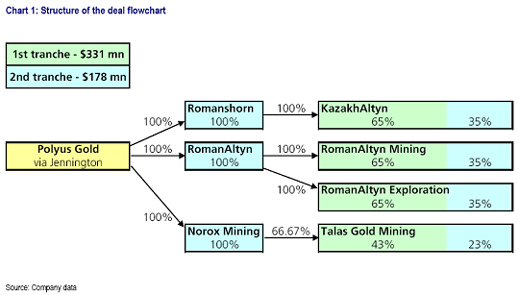

However badly the reputation of the latter may have suffered, the question has been asked – can a dealmaker as shrewd as Prokhorov have been as much in the dark as he claims retrospectively for a year or more, as he negotiated the takeover scheme? Look carefully at this deal chart, prepared by UBS analyst Alexei Morozov on December 8, showing how Prokhorov and the Assaubayevs have now agreed to unwind and reverse the deal they originally worked out in 2008 and 2009, before they started accusing each other:

Is it possible for Polyus Gold and Jennington, the Prokhorov companies, to have miscalculated with such big numbers as the Assaubayev goldmining vehicles, Romanshorn, RomanAltyn and Norox Mining are now pledging to repay? And if mistakes like that really happened, what asset valuation mistakes might Prokhorov be capable of inside his very own Polyus Gold, on the Russian side of the frontier?

According to the UBS report, the outcome between Prokhorov, the Assaubayev family and the Kazakh government is a deal in which “Polyus Gold will not incur any economic loss as a result…Eventually Polyus will have a Jersey registered company with cash on its books, which may become a consolidation centre for the company during the reverse takeover of KazakhGold by Polyus at a later stage.”

Ten days after Prokhorov declared he is winding up his KazakhGold problems, he announced a new set of estimates and projections for the Natalka goldmine project.

The good news is that Natalka is now estimated to be capable of producing 1.5 million oz of gold per annum for the life of the mine; this compares with 1.2 million oz which Polyus Gold currently produces from all operations (70% of that comes from the declining Olimpiada mine). Also, the expert estimates suggest the average grade for Natalka’s life of mine production will be 2 grams per tonne, rather than the 1.13 g./t target previously announced. Inside this average figure, however, it turns out, the company now acknowledges, that the grades will be lower in the initial phase of mining than it has previously suggested. This in turn suggests that mine output may be lower, and mine costs higher.

The not so good news is also that the project start-up is delayed for so long beyond previous targets, Prokhorov’s intention may be to sell out of the company beforehand. In that event, who knows when Natalka may produce?

Vladimir Zhukov, the metals analyst for Nomura in Moscow, reports this week: “The largest negative surprise of the new management guidance for phase one [of the Natalka mine plan] is a significant reduction of gold grade, gold output and a resulting increase in cash cost… While disappointing, we believe that the bulk of potential negative surprises for Natalka has been exhausted and we have now much more confidence in the new numbers provided…

In terms of positives, we highlight the improved overall parameters of the mine with now higher life-of-mine ore grades and sustainability of the reserve base at much more reasonable cut-off grade assumption. In our view, a significant downgrade of the operating parameters for phase one owes to the choice of a very conservative mining plan, which suggests the possibility of upside surprises once actual mining is launched.”

According to Morozov of UBS: “we believe the market is accounting only for a minimal value of the Natalka mine, foreseeing complexity and numerous problems related to it. It appears to us that the real work on Natalka will occur only in 2012-13 when there could be a new management team in place as the result of a potential merger with another major gold producer. Thus, we see the Natalka mine as the function of a potential merger. Should Polyus obtain a more experienced management team with a stronger ability to deliver growth, the market would start to price in more value for Natalka due to lower execution risks.”

That’s the polite way of saying that what the market really thinks of Prokhorov as a goldminer is that it is waiting for him to sell out and go away. Far away.

Leave a Reply