By John Helmer, Moscow

@bears_with

This is the story of how Vladimir Putin changed his mind on who should own Russia’s most important asset sailing the seven seas. Or did he really?

This is also the story of the privatisation of Sovcomflot, the state-owned shipping company and one of the largest fleets of oil and gas tankers in the world. Or is that what really happened?

On July 23, 2019, Sergei Frank held his first meeting of the Sovcomflot board of directors appointed for the new financial year. Frank had been chief executive of the company for fifteen years; he had been planning to sell shares in the company on the London, or New York, or Frankfurt stock exchanges for almost as long. On one interpretation of that history – documented in one of the longest-running litigations in the British courts — the sale of the state shares and the distribution of the proceeds in private hands were the Sovcomplot.

A company press release quoted Frank at his board meeting as expressing his thanks to Sovcomflot’s shareholder for approving a new round of shipbuilding. The shareholder to whom Frank was obliged was, of course, the Russian government; and in the mid-summer of that year nothing seemed to be out of the ordinary there.

At the end of June 2019 Frank had been reappointed chief executive, and the members of the company’s board elected for the new financial year; they included an extra auditor. At the beginning of July Frank had celebrated receiving a medal from Prime Minister Dmitry Medvedev; it was the Pyotr Stolypin Medal First Class. According to the citation, Frank had earned his medal “for merits in development of maritime transportation and long-term dedicated work.”

Sergei Frank (left) briefs Prime Minister Dmitry Medvedev (right) on December 2, 2016; behind them (centre), Transport Minister Maxim Sokolov.

It was one month before Frank’s 59th birthday; he was well short of official retirement. A decade had elapsed since he told Lloyds List, the London shipping industry paper, that “the chief executive of a shipping business shouldn’t go beyond their mid-to-late forties. For my generation it will be very difficult to be leaders for the people who were born in the 1980s, as in some areas, they are more talented and capable.” As the summer of 2019 began, Frank had no intention of leaving his post. Then on September 17 it was reported he was being pushed out.

Source: https://johnhelmer.net/sergei-frank-loses-his-footing-at-state-tanker-company-sovcomflot/

According to Moscow sources at the time, a campaign was under way by the Federal Security Service (FSB) to remove Frank, and appoint Igor Tonkovidov in his place. Tonkovidov, just four years younger than Frank, had been trained as a marine engineer in Odessa and then in financial management at the University of London and INSEAD in Paris. He had moved in and out of Russian shipping companies until 2008, when he became head of fleet operations at Novorossiysk Shipping Company (Novoship); that was shortly after Frank arranged the formal merger of the two companies. Tonkovidov was then transferred to Sovcomflot where in 2012 he was named chief technical officer of the company. Ranked at the bottom of Sovcomflot’s senior management, he was not included in the board of directors.

In September 2019 government and state company officials had only just returned from their summer holidays when a handful of them leaked to Reuters and Forbes that Frank “may soon leave [his] post”. That autumn surprise was to be implemented by “convening an extraordinary meeting of shareholders to approve the composition of the board of directors and appoint its chairman.”

Prime Minister Medvedev had agreed to strip Frank of his powers in an order signed on September 12. This revealed that another election for the board of directors was being called just ten weeks after a vote had been taken to install Frank and his 11-member board. On to the new list Tonkovidov’s name was added; named a director for the first time, his title was still given as Sovcomflot’s chief engineer. Frank’s name appeared after Tonkovidov’s on Medvedev’s order; his title as chief executive wasn’t there.

In the Reuters version Frank was stepping aside, but not exactly down. Other sources close to the decision-making claimed Frank was being made to walk the plank. According to Reuters, “Frank will give up operational control of Sovcomflot and take over as chairman of the company’s board.”

In the Forbes report, a government source “noted that in the near future directives on the convening of an extraordinary meeting of shareholders to approve the composition of the Board of Directors and the appointment of its chairman will be issued. The possibility of appointing Frank, the [source] refused to discuss.”

The press leaks were intended to prevent Frank’s closest supporters, Mikhail Fradkov — no longer prime minister (2004-2007) or head of the Foreign Intelligence Service (2007-2016) — and Gennady Timchenko, the US-sanctioned oligarch, from making a last-minute move to persuade Putin to rescue Frank. “Timchenko’s health deteriorated in the summer,” it was reported from a Russian shipping source, “and because of the US sanctions he has been forced out of the oil trade, so the takeover [of Sovcomflot] he and Frank had planned is impossible. Into the gap Tonkovidov is the FSB’s man.”

By this, the source meant that Frank’s plan to sell Sovcomflot shares on the New York, London or Frankfurt stock exchanges had been taken over and cancelled by state officials. Whatever would happen next to the state shares in the shipping company, the source said he didn’t know. He was certain, though, the original Sovcomplot had come to its end.

After favouring Timchenko and Frank, Putin had changed sides. Not all Putin cronies, to use the US propaganda term, had turned out to be equal. As for the role of the KGB network — another propaganda term — that has turned out to be more the Russian reaction to the US sanctions than the American reason for them.

In the 2020 year which followed, Sovcomflot’s fortunes depended, as they always did, on the price of crude oil; the rise and fall of tanker rates to transport it; and the cost of servicing the company’s heavy loan debt. In Frank’s fifteen years in control of the company, he had more than quadrupled this debt – from $770.8 million to $3.5 billion — and although he had also multiplied the fleet, the company’s vessels were unable to earn money fast enough to cover the rising cost of repaying the loans.

In 2018 the Brent crude oil price had risen well above its 2017 level, rising from $67 per barrel to $84 in October and down again to $50 at the end of December.

THE BRENT OIL PRICE FROM 2018 UNTIL NOW

Source: https://tradingeconomics.com/commodity/brent-crude-oil

Over the same period the Baltic Dirty Tanker Index, the shipping industry’s measure of freight rates for crude oil transportation, rose from 680 at the start of the year to a peak of 1,256 in December. Sovcomflot’s tanker revenues barely budged, however, at $1.1 billion. Vessel operating costs fell modestly by 6%. The bottom line was loss-making. At $46 million for 2018, however, this was two-thirds less than the $113 million lost the year before.

In 2019, the oil market was less volatile: the Brent oil marker commenced at $55 and ended at $66. The tanker rate index started sharply downward, hitting lows from 620 to 650 between April and July, then picking up again to reach between 1,500 and 2,000 in the last quarter of the year. Sovcomflot’s financial condition improved markedly. Revenues grew to $1.3 billion, up 18%; costs went down by 6%. The difference turned into a net profit of $225 million.

In 2020, the company managed to keep its tanker earnings stable even as the demand for oil collapsed with the onset of the pandemic, followed by the introduction of OPEC output limits. The tanker index plummeted from a high of 1,500 in January – when tankers were hired to store surplus oil at anchor in harbours around the world until market demand recovered — to between 400 and 550 in the second half of the year; that was as low as the index had fallen since 2009.

Notwithstanding, as of June 30, 2020, Tonkovidov announced that Sovcomflot’s revenues had jumped by almost a third over the same period of 2019, while vessel operating and debt financing costs remained more or less the same. The bottom line was a profit of $226.4 million; this was up by 149% on the year earlier. It was a decidedly better performance than a report of June 2020 from the Fitch ratings agency was forecasting. According to Fitch, falling tanker rates would press downwards on Sovcomflot’s revenue and profit lines. “SCF [Sovcomflot] has not yet been negatively affected by the coronavirus pandemic beyond small operational difficulties, which the management believes are manageable and negligible. However, we assume,” said Fitch, “that SCF’s earnings will fall in 2H20 despite a healthy 1Q20, resulting in annual EBITDA [earnings before interest, taxes, depreciation and amortization] in 2020 that is about 19% lower than 2019.”

A month later, on July 17, 2020, the Standard & Poor’s (S&P) rating agency reported greater optimism. “The company will generate sufficient cash to absorb large, although diminishing, committed capex [capital expenditure] of $450 million-$500 million (including the dry-dock and special survey expense) and continue gradually reducing adjusted debt to about $3.3 billion in 2020 from about $3.6 billion in 2018.”

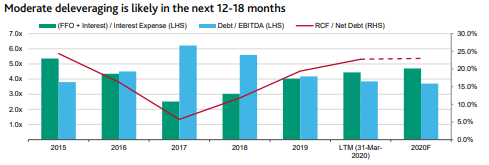

Moody’s, the third international rater, issued its assessment of Sovcomflot on June 9, 2020. Its analysts charted the blow-out of company debt – “credit metrics” and “leverage” were the terms they preferred — but they did not criticise Frank for it; nor did they report that his replacement by Tonkovidov pointed to a significant change of government policy for the company. Moody’s missed the significance of the personnel change.

DEBT-TO-EARNINGS AND OTHER MEASURES OF SOVCOMFLOT’S LEVERAGE

KEY: FFO=funds from operations; LHS=left hand side (cost in base currency); EBITDA=earnings before interest, taxes, depreciation, and amortization; RCF=retained cash flow; RHS=right hand side. Source: http://sovcomflot.ru/

Sovcomflot’s “credit metrics deteriorated significantly in 2017, driven by the market downturn, which coincided [sic] with an extensive programme of debt-funded vessel construction and asset acquisitions (the company added more than $1.0 billion worth of assets to its balance sheet in 2016-17). As a result, the company’s leverage, measured as adjusted debt/EBITDA, rose to 6.2x in 2017 from 4.5x in 2016. In 2018-19, SCF reduced its investment activity, which, coupled with gradually improving EBITDA generation, resulted in its adjusted leverage declining to 5.6x and 4.2x, respectively.” There was a fresh warning of the risk of not being able to earn enough to cope with debt. “Despite the sound recovery in SCF’s financial metrics, with its adjusted debt/EBITDA likely trending below 4.0x in 2020, its credit profile has historically been fairly volatile and the company still needs to demonstrate its ability to maintain leverage at a comfortable level through the market and investment cycles.”

The government decided it was time to sell company shares on the Moscow Stock Exchange. The banks selected for the deal were VTB and Sberbank of Russia; Citigroup, JP Morgan and Bank of America from the US; ING of The Netherlands.

The plan, the company had assured Fitch in mid-June, was to privatise a block of 25% minus one share. Standard & Poor’s report of mid-July warned against privatising a larger stake than that. “The rating may come under pressure if we revised down our assessment of the likelihood of government support. This could occur if, for example, the government decreased its stake in the company to less than 75%.” In other words, so long as Sovcomflot was carrying a heavy loan debt, the company’s shareholders were protected from the risk of default by the Russian state. Reduce the state stake, and the risk of the debt Frank had left behind at his departure would grow.

The Moody’s report said the same thing: “The government has named SCF [Sovcomflot] a candidate for privatisation and plans to sell 25% less one share of SCF by 2022. We do not expect the privatisation of a non-blocking stake to have any significant effect on the company’s operations or reduce the degree of control of the state over SCF.” An extra caution was added – Moody’s advised the company to use the cash from the share sales to pay down its debt balance. “Privatisation could improve SCF’s credit profile if proceeds are applied to recapitalise the company as initially planned.”

Remove Frank, cut the debt, start selling the shares, and wait — the value of the company would be bound to rise, the new men in charge of the shipping company appeared to be telling themselves. Once the financial details became available in March of 2021, when the full-year financials were released, it became clear the wait would be a long one.

Tonkovidov had been promoted against Frank by a national security faction of government officials. Frank’s strategic mistake, in their eyes, had not only been to increase the company’s debt to a record level, increasing its dependence on international banks, especially American ones; but he had also built a fleet too big to serve Russian oil and gas exports, thereby increasing its vulnerability towards foreign energy customers, especially the Anglo-American group, such as ExxonMobil and Royal Dutch Shell.

Sovcomflot has traditionally been coy in disclosing how much of its debt is under foreign bank control, as well as the proportion of its oil and gas cargo chartering customers who are not Russian. The start of the US sanctions war against Russia in 2014 has made both points sensitive ones in Moscow, and so more or less secret.

However, as early as October 2010, when Frank hired JP Morgan and Deutsche Bank to join the Russian VTB Capital to sell $750 million worth of debt securities, the company was obliged to warn: “the Group derives a significant portion of its revenues from Russian and international oil and gas companies. During 2009, the Group’s largest customer accounted for approximately 9% of the Group’s gross revenues, and the Group’s 10 largest customers accounted for approximately 52% of the Group’s gross revenues over the same period. If one or more of the Group’s key customers breach or terminate their charter contracts or renegotiate or renew them on terms less favorable than those currently in effect, or if any such customer decreases the amount of business it transacts with the Group, it could have a material adverse effect on the Group’s business, financial condition, prospects and results of operations.”

“Terrorist attacks and war or other events beyond the Group’s control that have an adverse effect on the production, transportation or distribution of oil and oil products could entitle the Group’s customers to terminate the Group’s charter contracts, which would have an adverse effect on the Group’s business, financial condition, prospects and results of operations.” The likelihood of US and NATO war against Russia seemed as remote in mid-2010 as it was certain a decade later, in mid-2020.

Sovcomflot’s prospectus of 2010 had identified a list of US and NATO-allied oil company clients, including ExxonMobil (US), Chevron (US), ConocoPhillips (US), British Petroleum (UK), Shell (Anglo-Dutch), Total (France), Repsol (Spain) and Statoil (Norway). It also listed as customers the international oil traders Glencore (Switzerland), Trafigura (Singapore), and Vitol (Switzerland), together with Timchenko’s Gunvor. But it avoided revealing what proportion of Sovcomflot’s revenues was earned transporting their cargoes.

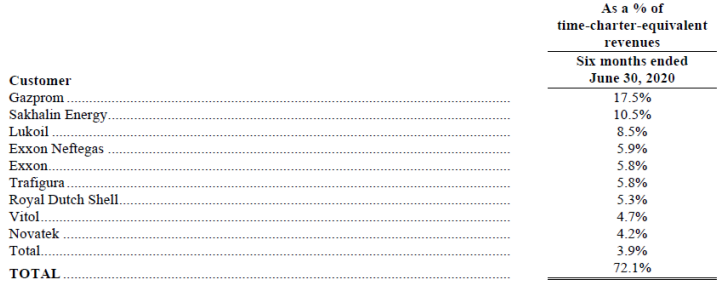

A decade later, in June 2020, the company had become significantly more Russia-centric and less dependent on the US and NATO for clients:

SOVCOMFLOT’S TOP CUSTOMERS

Source: Sovcomflot, share sale prospectus, October 7, 2020 – page 3. The figures for Trafigura and Vitol indicate crude oil produced by the state oil company Rosneft. Compared to a set of client figures reported by Moody’s for 2019, Total was up significantly, Exxon was up slightly, Shell down significantly, and the balance for others had dwindled by 7 percentage points.

The company had also reoriented its vessels to what it has called “industrial” business. This includes gas transportation and the operation of LNG and liquefied petroleum gas (LPG) tankers. It also includes running shuttle tankers between offshore wells and larger vessels bound for export ports, as well as onshore terminals and refineries; operating vessels for seismic research of the deep seabed; and delivering workers, supplies and other logistic services to offshore rigs and platforms, most of them in the heavy ice conditions of the Arctic region. In 2005, Frank’s first full year as chief executive, this line of business was non-existent; in 2010 it accounted for 18% of the time-charter equivalent revenues of the company; in 2020 this had grown to almost 51%; by the end of June this year, the industrial business segment – gas plus offshore operations – was up to 65%.

Source: http://www.scf-group.com/

From 2014 US sanctions had been attacking the main Russian oil and gas producers, and targeting their foreign partners and sources of capital for the development of the Arctic offshore fields from which the oil, gas and industrial lines of Sovcomflot’s business flowed. War risk, especially US sanctions threats, made a share listing in the US or UK impossible; it also made a discount for Sovcomflot’s share price inevitable.

In September Reuters was told by “two sources familiar with the [share sale] plans” that “there was strong Russian interest, some of which could act as anchor investors.” The aim was “to raise at least $500 million in an initial public offering (IPO) on the Moscow Exchange…in a deal that could value it at roughly $10 billion.”

This valuation was calculated by comparison with Sovcomflot’s international shipping company peers. “A banker involved in the deal pointed out its peers trade at 7-12 times their expected core earnings (EBITDA). Sovcomflot posted EBITDA of $1.03 billion in the 12 months ended June 30 [2020].” Thus, the target valuation to which Reuters and its Sovcomflot sources were pointing was between $7.2 billion and $12.4 billion – or $9.8 billion down the middle.

These numbers were a fantasy. The list of international peers cited by Reuters revealed none with a market capitalisation above $1.5 billion: Reuters listed Scorpio Tankers, then at $916.4 million; Frontline, $1.4 billion; Golar LNG Partners, $1.2 billion; Hoegh LNG Partners, $525.3 million; GasLog, $545.5 million; and Cosco Shipping Energy Transport, $476.7 million. The one exception on the list was the Chinese state shipping company, China Merchants Energy Shipping, whose market cap was $5.4 billion. China Merchants Energy Shipping has a smaller tanker fleet than Sovcomflot; at its initial public offering on the Shanghai exchange in 2011, its market capitalisation was priced at almost ten times earnings; the cap then came to $566 million. Today the China Merchants Energy Shipping’s market cap is ten times the initial value.

Two weeks after Sovcomflot’s IPO announcement, Reuters was told by the company’s bankers not to exaggerate. There were simply no buyers for wishful thinking. Bankers involved in the deal now claimed that “investors should expect the IPO to price at 105 rubles ($1.34) per share, with books oversubscribed. That compares to an initial marketing range of 105-117 rubles per share.” They added that the company “is expected to be valued at about $3.2 billion after the deal. It is issuing new shares worth up to $550 million and plans to use the proceeds for investments in new assets, decarbonisation and deleveraging.”

By the time the order book closed and share trading started on October 7, instead of selling the target of 25% of the company’s shares, just 17.3% had been placed. The opening share price was at the bottom of the range, Rb105 ($1.34); market cap, $3.2 billion. The share price then nose-dived in the first hours to Rb91.56 – that was a decline of 13%.

According to a briefing from those involved, reported by Reuters, the anchor investors took 85% of the share offering; just 15% of the shares went to retail investors in Russia and abroad. The state wealth institution Russian Direct Investment Fund (RDIF) acknowledged it was one of the anchor investors “along with leading wealth funds from the Middle East and Asia”.

This too was an exaggeration. According to Sovcomflot’s financial report issued on November 16, the share sale at Rb105 had produced total gross proceeds of Rb42.9 billion, equivalent to $550.2 million. However, the company itself had to buy back from the underwriters 37 million of the 408 million shares issued. This block, 9% of the IPO, had been bought by the underwriters to prevent the nominal price falling below the low target of Rb105. Sovcomflot called this price-rigging “the course of stabilization activities”. The deal was that, in return, Sovcomflot itself would buy back the shares from the banks. According to the company report, “such shares were repurchased by OOO SCF Arctic, a wholly owned subsidiary of the Company, at RUR 3,701.6 million (equivalent to $47.2 million, as of the date of date of exercise of the repurchase option). These shares are held by SCF Arctic in treasury.”

In other words, Sovcomflot was an anchor investor in itself – the leading one. The free floating shareholders amounted to 15.6%; the Russian government held 82.8%. The bank deal arrangers charged $22 million for the appearance of the privatisation. Net proceeds amounted to $481 million before subtracting outlays of state funds from RDIF and other Russian “anchors”.

Almost all of the Sovcomflot share sale had been paid up by Russian state funds, either committed directly or loaned to intermediary buyers with promises of profitable buybacks. They began selling immediately, according to stock brokers at the exchange. “According to Vasily Karpunin, head of the BCS World of Investments information and analytical content department, rather ‘large volumes for sale were visible, which indicates a desire to exit the securities by a large participant.’ It is unlikely that these can be private investors, ‘because they for the most part implement a long-term investment strategy,’ he notes. Evgeny Shilenkov, Deputy General Director for Active Operations of Veles Capital IC, believes that investors who ‘expected the book to be re-signed’ without ‘seeing the upside’ began to sell the paper, but did not find demand ‘near the placement price.’ Buyers appeared at a price 10% lower – they were those who did not want to participate in the IPO the day before, he adds.”

After twenty-four hours the Russian business press called Sovcomflot’s share sale a failure. “Technical difficulties, lack of information, the speculative component, and other factors” were blamed by Pavel Gavrilov, an analyst with BCS Express. He tried to sound hopeful. “The short-term potential disappears very quickly due to the failed IPO. But the long-term view of the ‘sea wolf’ remains moderately positive. We can assume that the accumulated negative in the stock price will eventually go away. This is supported by strong financial results, new projects and contracts. From a psychological point of view, we need to return to the level of the IPO price — 105 rubles. Perhaps this will restore confidence to investors, and an uptrend will begin, which will be fundamentally fully justified. It will take several months to implement such a scenario.”

For the time being, however, “we can conclude that rapid growth of capitalisation will not happen. First of all, the shares need to return to the IPO level of 105 rubles, which is a certain psychological point for investors. This is possible with a stable external background, as well as a positive news background.”

Three charts show that as far as the buyers and sellers on the Moscow exchange are concerned, Sovcomflot has only itself to blame, as the tanker market news had been helping to propel the share prices of its international rivals in the opposite direction; that is upwards.

THE FALL OF SOVCOMFLOT’S SHARE PRICE SINCE PRIVATISATION

October 2020-November 2021

Source: https://markets.ft.com/

Market capitalisation, Rb206 billion ($2.9 billion) – this marks a decline of 13% since the initial share sale, October 7, 2020. According to the company’s annual report for 2020, prepared in April 2021, the free float, originally planned to be 25%, was just under 18% at the IPO, and now amounts to 15.6%; the state has retained a shareholding of 82.8%.

HOW SOVCOMFLOT COMPARES WITH ITS US & NORWEGIAN TANKER RIVALS

November 2020-November 2021

Source: https://markets.ft.com/ KEY: Dark grey=Sovcomflot (market cap $2.9 billion); orange=Frontline ($1.8 billion); orange=SFL ($1.1 billion); green=DHT ($1.1 billion ); yellow=Teekay ($369 million). Sovcomflot’s market cap remains larger than its international peers, but all of them perform better and above the Sovcomflot share-price line.; this indicates market rigging by Russia’s state banks.

HOW SOVCOMFLOT COMPARES WITH ITS BIGGEST INTERNATIONAL RIVAL, CHINA MERCHANTS ENERGY SHIPPING

Source: https://markets.ft.com/

China Merchants’ current market cap is $5.5 billion.

What was really happening inside the company and inside the Moscow market, which the outsiders didn’t know, and the insiders had no intention of revealing?

“The sale of newly issued shares has had nothing to do with open market activity or economic efficiency for the state as shareholder or for the company itself,” a Sovcomflot insider said. “The proceeds were not used to pay substantially increased dividends to the state or even to direct sale proceeds into the state budget. The company has not announced any new Russian project in partnership with the state. They are sitting on the money.”

“The privatisation operation – operation is the only term that’s appropriate – was carried out to convert piles of rubles from an oligarch group into shares of a company whose assets are valued in hard currency. This operation was camouflaged by side investors who have lost their money. As for Frank’s scheme for promoting the merger of Novoship and Sovcomflot and listing the shares at a premium price, the sharp, sustained drop in the price of the company’s shares since last October on such a protected and controlled stock exchange like Moscow’s has demonstrated his final failure.”

“Tanker companies have never been a good investment,” says Alexei Bezborodov, a leading Russian maritime industry expert. What oligarch group has moved into the shipping company? He doesn’t know, he says.

A Sovcomflot insider points to Arkady and Boris Rotenberg. That they are close enough to Putin is well-known; that was also one of the grounds for the US Treasury sanctions to be imposed on them in the first round against the “inner circle”, announced on March 20, 2014. The Rotenbergs were sanctioned at the same time as Timchenko, the Treasury press release said, “because each is controlled by, has acted for or on behalf of, or has provided material or other support to, a senior Russian government official” – that was Putin.

Left to right: Arkady Rotenberg, Gennady Timchenko, and President Putin, May 2015.

The Rotenbergs, according to the Treasury sanctions announcement, “have provided support to Putin’s pet projects by receiving and executing high price contracts for the Sochi Olympic Games and state-controlled Gazprom. They have made billions of dollars in contracts for Gazprom and the Sochi Winter Olympics awarded to them by Putin. Both brothers have amassed enormous amounts of wealth during the years of Putin’s rule in Russia. The Rotenberg brothers received approximately $7 billion in contracts for the Sochi Olympic Games and their personal wealth has increased by $2.5 billion in the last two years alone.”

The US Government appears to have missed the steady accumulation of commercial control by the brothers over Russia’s transportation businesses; for that story, read this archive. There was no mention of the Rotenbergs, nor any trace of their companies, in the Sovcomflot story as it was elaborated in the London court records of the Sovcomflot litigation.

The Sovcomflot insider says it has been the US sanctions war against Russia which created the motive, means and opportunity for the Rotenbergs to move into Sovcomflot, replacing Timchenko and Frank. “Tonkovidov is the FSB’s man,” according to this source. “Rotenberg is in an alliance with the FSB and he is now de facto the minister of transport for the country. All the transport infrastructure is controlled by this group including roads and railroads. Cement and metals are additional items of their interests. Of the two brothers, Arkady is the more influential.”

“Practically speaking, Timchenko has swapped his old interest in Sovcomflot for his new interest in fishing. The oil and gas business he has left remains independent of Sovcomflot. On his interest in Sovcomflot there has been too much attention, too much light, but the profit is miserable.”

By the time the company issued its audited financial report for 2020 on March 15, 2021, Sovcomflot’s market capitalisation had fallen with the share price to just under $2.9 billion; that was less than half the reported value of the company’s fleet assets — $6.2 billion. This market valuation was also several hundred million dollars less than Sovcomflot’s loan debt of $3.2 billion.

Introducing the financial accounts, Nikolai Kolesnikov, chief financial officer of the company, claimed the IPO had “resulted in a strengthening the balance sheet and the financial position of the Group, with net debt to EBITDA ratio falling to 2.6 times [2.6x]. The Company has sufficient investment capacity to undertake large scale projects and to pursue further growth in its core strategic segments.” This ratio is a number on paper; its significance is limited to Sovcomflot’s bankers who have imposed covenants including this ratio for loan terms; and to the ship finance market which has seen the total indebtedness of the company and the debt-to-earnings ratio blow out to a peak of 6.0x in 2017-2018.

Left: Igor Tonkovidov, 57; right, Nikolai Kolesnikov, 58.

According to the IPO prospectus, the company claimed it “intends to use net proceeds from the placement of the Offer Shares for general corporate purposes, including, without limitation, investments in new assets, with a focus on industrial projects, decarbonisation and further deleveraging.”

The accounts reveal this is not what became of the $550 million in gross share sale proceeds announced at the IPO, nor to the net proceeds of $481 million, after the company had bought its own shares back from the banks and paid them their fees. Overall loan debt at September 30, just before the IPO, was $3.45 billion. The number announced at year’s end was $3.23 billion. The reduction in debt appears to have been $220 million.

However, the financial report also revealed that Sovcomflot had signed a fresh contract in January for one new liquefied natural gas (LNG) tanker at a cost of $182.8 million, with an option to build two more. In November it had borrowed $155 million from two Japanese banks to pay for the vessels.

There is no sign in the new financial documents that Sovcomflot has paid the state budget any part of the share sale proceeds. Instead, in the small print it is revealed there has been a large increase in the number on the “cash and cash equivalents” line – from $374.8 million in 2019 to $849.5 million at the end of December 2020, and $851.3 million on June 30, 2021. This is an extra cash pile the company is now sitting on. Kolesnikov’s calculation of the debt-to-earnings ratio counts this money for reduction of the gross debt figure to the net debt figure.

SOVCOMFLOT’S CASH PILE, DECEMBER 2020-JUNE 2021

Source: http://www.scf-group.com/ and then click to open. In the latest Sovcomflot financial report, issued on August 26, 2021 for the first six months of this year, the bottom-line cash and cash equivalents total had risen by just $1.9 million to $869,165,000.

There has been no explanation from Tonkovidov or Kolesnikov for the decision to do this instead of doing what the IPO prospectus promised. Frank declined to comment on this report.

In years past, the added cash on the asset side of the balance-sheet might have helped boost the bonuses of the senior management of the company. It was reported in the Moscow business press in 2006 that the formula for then-chief executive Frank’s bonus was one-quarter of the management bonus pool, while the pool was filled with company cash calculated from 5% of the dividend declared for the state treasury, plus 2.5% of the asset value added to the company balance-sheet during the year.

Sovcomflot’s annual report for 2019 doesn’t say what the management bonus formula was except to claim that it depended on “the attainment of number of key performance indicators”. As chairman of the board of directors, Frank was then on fixed pay of just under $100,000 per annum. Tonkovidov, Kolesnikov and other senior executives received more in bonuses than in salary – Rb310 million ($4.8 million) versus Rb208 million ($3.2 million) – for 2019. The annual report for 2020 reveals that the board directors, including Chairman Frank, received a fixed salary of Rb50.4 million in total, and no bonuses. The senior management of the company, according to the report, received salary in total of Rb232.6 million, and bonuses of Rb301.8 million.

From the point of view of the men on bonus, the senior managers and the board directors, it hasn’t mattered that the long awaited, much hyped privatisation failed to support the target share price, let alone achieve one-third of the target valuation in the original Sovcomplot.

For the state budget planners, the new shareholding made no difference to the company’s strategy and financial prospects in the short or long run. The share sale had been fabricated; the genuinely non-state or private stake in Sovcomflot was less than 10%. The banks had profited; the private investors had lost money, but the state had neither profited nor lost.

From the Rotenbergs’ point of view as Sovcomflot’s new minority shareholders, the falling share price is advantageous. In time, if their ambition to take control of Sovcomflot is realised, they can hope to acquire the company’s assets cheaply.

This isn’t the result President Putin claimed to have achieved when he spoke at a VTB conference with international investment funds on October 29, 2020. “As I understand,” Putin responded to a question from a Swiss fund manager, “you took part in the Sovcomflot IPO. I want to thank you for that. It is true, as I said, we attracted 42 billion, and I want to draw the attention of our audience to the fact that this money will not be used to pay dividends or other noble but not necessary goals in this case. Paying dividends is very important for improving a company’s capitalisation, but in this case, all this money will be used for the construction of ships of various kinds, for creating work for our enterprises and thus for expanding the capabilities of the Russian carrier.”

Left: Joaquim Nogueira, for the Swiss-based GAM Investment Management firm, asked what sectors Putin intended to open further to privatisation and which he intended to preserve for the state, following the Sovcomflot IPO. Source: http://en.kremlin.ru/ -- Min 1:00:32.

“Sovcomflot was a 100 percent state-owned company”, Putin went on, “and now the state’s share has decreased. The government retains control over the enterprise, but the trend has been set. In the near future, next year, we plan that 180–186 stock companies with state participation and approximately 86 unitary enterprises will take part in the privatization. And another 1,300, I think, various economic entities that belong to the state will also take part in the privatisation process.”

“At the same time, I want to emphasise that there are at least two factors that we take into account and that lie at the root of all privatisation processes. First, we assume that any privatisation deal must improve the enterprise’s efficiency, create new jobs, new investments and technologies. This is the most important thing. And, finally, we cannot forget about the market conditions in which privatisation deals are made. That is, they must be fiscally profitable, bring some profit to the treasury.”

“All of this money” — “42 billion” — “market conditions” — “some profit to the treasury”? At the end of the Sovcomplot, none of these claims of the president has turned out to be true. But Sovcomflot’s share sale had not been a failure. It was a successful fake.

Leave a Reply