By John Helmer, Moscow

Now for those who think the appetite for due diligence and accountability deadens the taste for opportunity, the good news from the Russian goldmines comes today from Alfa Bank’s metals analyst Barry Ehrlich, in a set of three fine reports.

The global supply and demand balance for gold is stable: the gap between under-supply and expanding demand is closing, compared to 2010, but supply growth appears to running at 3% per annum, and demand growth at 5% per annum. If that’s right, the gold price will be secured by the increase in jewellery and bullion buying in China and India, and by government stockpiling of gold worldwide, as a hedge against volatile currency movements.

The latest figures from the Central Bank of Russia show, for example, that gold stocks in Russia’s international reserves (third largest in the world) jumped from a value of $36 billion at the start of the year to $49 billion at the start of September (before dropping to $44 billion this month to pay for the bank’s rouble defence). A total of 192 tonnes of gold were purchased (net) by governments in the first half of this year, compared with net sales of roughly 200 tonnes per annum in earlier years.

At present, about 40% of global gold demand originates from China and India, both for jewellery manufacture and for investment. According to Ehrlich, reporting on World Gold Council data, “Indian jewelry demand has not only caught up with the pre-crisis period but has well surpassed it. China has moved from consumption that was well below 400ktpa prior to 2008 to a level of 750ktpa over the past four quarters.”

Forget Greece’s troubles, and the even bigger problems facing the Euro and the US dollar. For the time being, they support the gold price where it is, and thus, other people’s troubles remain supportive for the value of comparative Russian stability. “We assume there will not be a credible long-term solution to sovereign debt issues in the coming year. This will leave the official sector in a position where it is more likely to be buying rather than selling gold, we believe.”

So looking east, unless you figure that a sudden, grave and sustained loss of Chinese and Indian cash to buy gold is in the offing, the price of gold is likely to stay in the range of $1,600 to $1,700 per ounce.

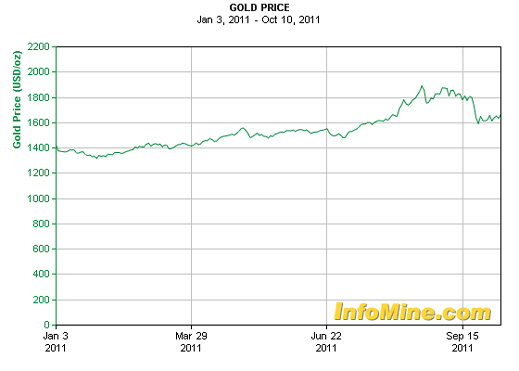

Here is how the gold price has moved in the year to date:

Ehrlich is also forecasting a bottom for gold for the foreseeable year or two ahead of $1,300 per ounce.

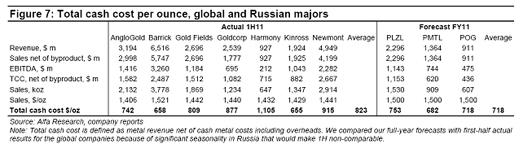

At that price, roughly one in 20 goldmines in the world will cease to be profitable. But none of them is in Russia. Ehrlich’s tabulation of the cash cost of producing gold in Russia demonstrates, not only that there is a plump profit cushion for the Russian goldminers, without accounting for further rouble devaluation; but also that the Russian goldminer’s profit margin should remain comfortably ahead of the international goldmining average. The Russian cost advantage, comparing averages, is 15%.

As can also be seen from the table, Polyus Gold (PLZL) is operating at a cost level that is greater than three of the internationals who have declined to make a takeover or merger offer that Mikhail Prokhorov and Suleiman Kerimov, owners of Polyus Gold, would accept – Kinross, Barrick, and AngloGold Ashanti.

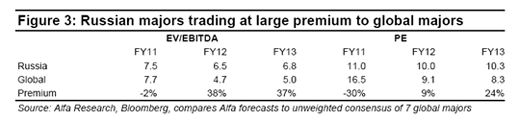

So if the fundamentals of the gold market and of Russian production cost look reassuring – that’s the silver lining – why have the Russian goldminers been dropping in share value on the stock markets? Where’s the opportunity in that?

According to Ehrlich, there are two answers. The first is that the listed Russian goldminers have been losing value this year because they were over-valued in relation to their international peers. Here’s the comparison for two ratios, Enterprise Value/Earnings (EV/Ebitda), and share price/earnings (PE):

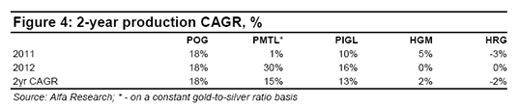

The second and related answer Ehrlich gives is that Russian goldminers can’t be believed when they promise production growth:

Note: PIGL is the successor to Polyus Gold (PLZL) after it completes its transfer on to the London Stock Exchange main board.

Petropavlovsk (POG), the company controlled by Peter Hambro and Pavel Maslovsky, appears to lead with a compound annual growth rate of 18%. Ehrlich warns against trusting that, pointing out that output in the first quarter of this year came in 17% below what Hambro had been advertising. Polymetal (PMTL) overshot by 25%, and according to Alfa estimates, the gap is even bigger if the conversion of Polymetal’s silver production to gold equivalent is taken into account. Polyus Gold may fall short of forecast by up to 22%.

Guessing what lies buried underground, and putting a value on what can be dug up (grade, volume), and a discount for coming up short, is what the mining markets have developed into a fine art. The problem with Russian goldmining companies is that the general lack of credibility with which the control shareholders are viewed translates into scepticism that they can deliver on production growth, or new reserves. Truth-telling is not a habit that is taught at the School of Mines, and the evolution of junior miners into major miners has never followed the Mosaic strictures, not in Russia any more than in Australia, Canada or South Africa. So the telling factor is the is the personal histories of men like Prokhorov and Kerimov at Polyus Gold; Alexander Nesis at Polymetal;Hambro and Maslovsky at Petropavlovsk; Roman Abramovich (aka Primerod International Ltd.) at Highland Gold (HGM); and Alexei Mordashov at High River Gold (HRG).

Over time, these fellows have also convincingly demonstrated to the stock markets what the former Russian regulator, Oleg Mitvol, used to say (before he was fired for saying it) – they are motivated to invest only in their offshore stock price, not in resource development at home.

After all the blandishments to which Moscow stock and sector analysts are subjected from the investment relations departments of the mining companies, not to mention the PR firms of London, here is what Ehrlich concludes about Natalka, the largest unmined gold deposit in Russia currently in development (Sukhoi Log’s licence remains in deep freeze): “Little development progress has been made at Natalka, the company’s main growth project, judging by capex numbers in 1H11. The company’s 1H11 capex was only $170m vs. our full year forecast of $800m. Natalka capex was targeted at $350-400m for 2011 and nothing was spent in 1H11. As a result, the start of development works at Natalka is postponed to 2012, which will likely push back its commissioning. We reiterate our 2015 commissioning forecast. If there is a further half-year delay to the commencing of large-scale development works, our 2015 forecast will no longer be realistic. Company guidance is for commissioning in 2013, but this was last voiced at the beginning of 2009. Ex-Natalka, the company’s 2011 capex will likely be around $400m.”

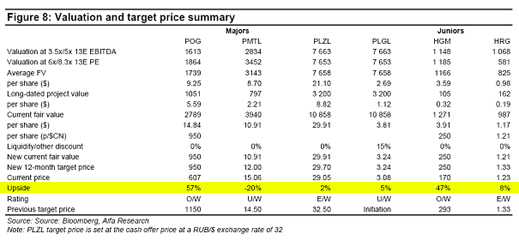

What is the value of Russian gold underground, if the estimation methodologies may be suspect, and the capital cost of bringing the gold up and into the sales market a blue-sky number, which the current stakeholders have little intention to raise or risk on their own?

Answer: not much. So where is the opportunity? Ehrlich recommends a simple rule of thumb – if and when you see Russian gold coming out of the ground, and can count it on the revenue line of the miner’s balance-sheet, then check the upside from market price to valuation. If it’s a big number, that’s the opportunity to buy:

Following the yellow line is still a wager. But never let it be said that I didn’t advise a golden opportunity when I see one.

Following the yellow line is still a wager. But never let it be said that I didn’t advise a golden opportunity when I see one.

Leave a Reply