By John Helmer, Moscow

Bank robbers of the manual, stick-up type have a reputation for a sense of a humour. That may be a comfort to them, because they usually get caught. Bank robbers of the International Monetary Fund type lack even a sense of irony, because they expect not to be caught, and never are. In the bank- robbing profession also, the driver of the get-away car is usually the least talented, the witless one who doesn’t see the gag, especially not when he or she is the butt of jokes from the rest of the gang.

This week, when Alexander Shlapak, the Ukrainian Minister of Finance, helped himself to $1.39 billion, the second tranche of the IMF’s Ukraine Stand-By Agreement of $17.1 billion, he illustrated the ministry’s Facebook announcement in Kiev with a picture showing an anonymous figure carrying a cheap briefcase away from the IMF headquarters as the Fund’s front-door sign is partially covered up by the Ukrainian flag. Counting the first tranche of $3.1 billion Shlapak took away on May 5, the cover-up is currently blowing at $4.5 billion. Another $1.39 billion had been scheduled for the taking in October. But that has been delayed and doubled to $2.8 billion for payout by December 15.

Shlapak is one of the getaway drivers. For his background as a custodian at Igor Kolomoisky’s Privat Bank, read this. For what IMF officials know about the private interests of their Ukrainian government counterparts, click here.

These IMF officials – Nikolai Gueorguiev (1), head of the IMF Ukraine team; Poul Thomsen (2), acting head of the European Department, to whom Gueorguiev reports; and Conny Lotze (3), the IMF’s press division chief – have been the getaway drivers at the Fund in Washington. They don’t see the funny side of the alibi they have been issuing for the Ukrainian government, and for themselves.

Since Reza Moghadam, head of the European Department, left the IMF in July for a job at Morgan Stanley in New York, he has gotten away from his handshake with Ukrainian prime minister Arseny Yatseniuk (image below), scot-free. At his departure, the IMF issued a release congratulating Moghadam for his “responsib[ility] for… the Fund’s response from one crisis to the next-including the most recent challenge in Ukraine.”

His boss, Christine Lagarde (4), managing director of the Fund, is in other trouble. She is under investigation for a €400 million French government heist several years ago. So far she hasn’t been obliged to make public her alibi. That, said the IMF board on August 29, is because “it would not be appropriate to comment on a case that has been and is currently before the French judiciary.” As for Lagarde’s looking the other way while the Ukraine money goes out the door, the Fund board also said it has “confidence in the managing director’s ability to effectively carry out her duties”. Lagarde says she’s been acquitted by the courts of the big crime of being in on the €400 million job, and is innocent of the current charge against her, “that I was not sufficiently vigilant”.

Vigilance is an alibi for the IMF’s financing for the Ukraine. Fund officials claim to be conducting their due diligence on Ukrainian compliance with the loan conditions in a transparent, publicly accountable manner; based on evidence collected by independent auditors selected openly and without conflicts of interest; their technical assessments have been conducted according to criteria the IMF officials have promised to disclose. None of these claims is true.

Instead, Gueorguiev, Thomsen, Lotze, and Lagarde refer all questions about their conduct to their Ukrainian beneficiaries. “We would suggest that you refer your questions on bank asset audits to the Ukrainian authorities”, Lotze’s department responded when the IMF’s Ukraine team was asked to clarify whether Valeriya Gontareva, Governor of the National Bank of Ukraine (NBU) was telling the truth when she announced in Kiev on August 15: “Conducting banks’ asset quality review is a part of the IMF-backed reform agenda. The fifteen biggest Ukrainian banks have already gone through a review and have not revealed any substantial problems”.

On August 21, Gueorguiev and Lotze were asked “to clarify: 1. what aspects of the Ukrainian bank review, as required by the conditionality of the SBA, have been completed with respect to the leading banks; 2.what tasks remain to be completed by what deadlines; and 3.what IMF approvals have been issued of the NBU submission summarized by Governor Gontareva?”

Two weeks earlier, on August 8, the IMF had issued what it called a board review of the IMF’s “communications strategy”. The review was brand-new — a sequel to the last such review in June 2007. The new review paper, though, had been written by the IMF’s Communications Department. So the directors were reviewing what Lotze had written about her own job performance. According to Lotze’s press release of what the directors thought of the self-audit, the board “observed [sic] that the overall strategy has allowed the Fund to communicate effectively and flexibly. They commended staff responsible for this work, particularly the Communications Department, for the substantial progress in implementing the strategy in a rapidly changing environment.”

Communication, the board reportedly added, “is a strategic tool and integral to the IMF’s improved transparency and broader effectiveness and accountability. Directors stressed nevertheless that good communication cannot substitute for the underlying policies.” As for the disclosure standards by which Gueorgiev, Lotze, Thomsen, and Lagarde should be judged, the board declared: “evolving issues facing the membership, as well as new technologies, require continued flexibility and proactive engagement, including with new media. To this end, they underlined the need to communicate in language that is easily understandable… Directors considered it important to maintain the Fund as an open, flexible, and responsive institution in its external communication, while at the same time preserving its role as a trusted advisor to its members.”

Gueorguiev and Lotze were asked to take these explicit directions into account when answering questions on their Ukrainian assessments — “should you and Ms Lotze not answer, you will be reported as refusing to answer.” They refused to answer.

The next day, Gueorguiev and Lotze recovered their voices when Gueorguiev told the Financial Times: “In all cases we make an unbiased assessment of the macroeconomic outlook based on the current information. Of course, downside risks related to the conflict prevail in the current environment. Difficult times call for difficult measures. And we see that this government is committed to reforms.”

In fact, among the directors on the IMF board serious concerns were being expressed, orally and on paper, that Ukrainian officials weren’t as committed or as compliant as the IMF’s financing conditions and covenants required. The board directors were also struggling to understand how the macro-economic and commercial evidence from Kiev – contraction of GDP, capital outflow, collapse of tax revenues, increase of public expenditures and budget deficit, growing subsidies for gas, rising insolvency risks at the country’s leading banks – could be made to substantiate the fundamental condition of IMF lending – that the recipient of the money is likely to repay it.

Since IMF board director comments are secret, it is rare for the board records to leak, exposing how little confidence the directors have in their staff reporting, or in the promises of recipients of the money. In the case of the IMF’s Cyprus loan of May 2013, dissenting reports from IMF board directors have been published. This record reveals that more than thirty of the board’s directors and their alternates reported their scepticism. They represented several dozen member states, including China, Saudi Arabia, Egypt, Indonesia, Italy, Germany, France, and Japan. They also included the Russian board representatives, Alexei Mozhin and Andrei Lushin.

The Brazilian government representative was blunt: “Every program needs a pinch of optimism but in this one the required dose of good-will – or suspension of disbelief, if you will –goes way beyond the average.” That’s a polite way of charging the IMF staff working on the Cyprus loan with incompetence.

Last week, by the time the IMF board was meeting to decide on the disbursement of more money for Kiev, the scepticism wasn’t less pronounced than it had been with the Cyprus loan. The Ukraine record, however, remains classified. No financial newspaper has reported it. The Russian objections, however, are not exactly secret.

Late in August, when Gueorguiev and Thomsen were trying to convince the board to come across for Kiev, and Lotze was refusing to answer questions, the Russian deputy finance minister responsible for the IMF, Sergei Storchak (right), revealed that there was no prospect of the board accepting that the Ukrainian government could meet the original conditions of the IMF loan. “Further revision is inevitable. Whether this adjustment increases the funding allotted will become known at the next conference expected in October or November with participation of Ukraine’s donor countries if there are still any by that moment.”

Late in August, when Gueorguiev and Thomsen were trying to convince the board to come across for Kiev, and Lotze was refusing to answer questions, the Russian deputy finance minister responsible for the IMF, Sergei Storchak (right), revealed that there was no prospect of the board accepting that the Ukrainian government could meet the original conditions of the IMF loan. “Further revision is inevitable. Whether this adjustment increases the funding allotted will become known at the next conference expected in October or November with participation of Ukraine’s donor countries if there are still any by that moment.”

Russia holds just 2.39% of the votes on the IMF board, and can exercise no veto. The US and the NATO member states control more than 40% of the board votes. Storchak wasn’t exactly saying that he and other directors who shared his doubt in Gueorguiev’s and Thomsen’s paperwork, would vote against the release of the second tranche of $1.39 billion. Nor was Storchak calling Gueorguiev and Thomsen accomplices to grand larceny. Publicly, though, Storchak did say there was a growing risk that Ukrainian government officials would spend the IMF money in ways the IMF board not only wouldn’t authorize, but couldn’t follow. “The fact that Ukraine’s vast territories with an important economic potential do not work to implement the stabilization program is a major factor that casts shadow on whether the stabilization program is realizable,” Storchak noted. He added that for the first time in its history, the IMF was lending money to one side engaged in civil war.

When Gueorguiev, Thomsen, Lotze, and Lagarde aren’t answering questions about this, they have had to acknowledge publicly the trouble brewing on the IMF board. On Tuesday, Thomsen gave his alibi, er interview, in which Lotze’s department asked the questions. The government in Kiev, Thomsen claimed, “has generally implemented policies as agreed under its economic program, but with ongoing conflict and geopolitical tensions, the country needs to address short-term challenges while not losing sight of deep-seated structural problems and vulnerabilities.” Thomsen admitted that two earlier IMF lending programmes, in 2008 and 2010, had failed for lack of compliance in Kiev, calling them “implementation slippages that marred previous Fund-supported programs with Ukraine”.

There is no mention of war, civilian casualties, destruction of infrastructure, or even of military spending in Thomsen’s account. Instead, “a number of risks have already materialized, including an intensification of the conflict in the eastern part of the country and an escalation of the gas price and arrears dispute between Ukraine’s national gas company Naftogaz and Russia’s oil and gas company Gazprom. This in turn has led to a notable deterioration in the economic outlook, budget performance, and balance of payment flows.” Thomsen says nothing at all about the direction of those “payment flows”. Lotze doesn’t ask him what the IMF has learned of where IMF financing for the NBU, which has been passed through to the commercial banks, has ended up, inside Ukraine or in offshore havens.

“Some temporary deviations from the initial program targets will be accommodated,” Thomsen acknowledged, “while compensatory measures related to foreign exchange market purchases, fiscal measures, and Naftogaz bill collections will also be put in place to ensure that key program objectives are met.” Thomsen did not elaborate on what exactly the new measures are, and what conditions are required to be reported back to the board, before the next payout deadline in mid-December.

By then, he conceded, “we would have to reconsider elements of the program strategy, and the program’s viability could hinge on larger assistance from Ukraine’s international partners. We will have to see.”

Despite Gueorguiev’s and Lotze’s refusal to say last month whether they accepted the NBU Governor’s claim that the audit of the country’s leading banks had been “satisfactory”, Thomsen said the IMF “ now envisages higher potential bank restructuring costs.” That must mean the Ukrainian banks are in far worse condition than Gueorguiev, Lotze, and Governor Gontareva have been admitting publicly.

As for transparency and accountability, according to Thomsen “in consultation with IMF staff, the government conducted a diagnostic study on governance issues to identify areas for reforms, focusing on tackling corruption and improving the business climate and the effectiveness of the judiciary. This report has not been published.

The IMF staff report compiled for last week’s board decision by Gueorguiev admits that fighting is going on in Ukraine. His report also reveals that two-thirds of the $1.39 billion in new money which Shlapak has now received will be spent on the government’s military and security operations, er, budget deficit.

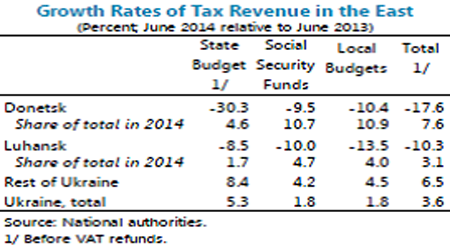

For the first time in any open publication, the IMF staff report reveals the collapse of tax revenues from the eastern regions of the country:

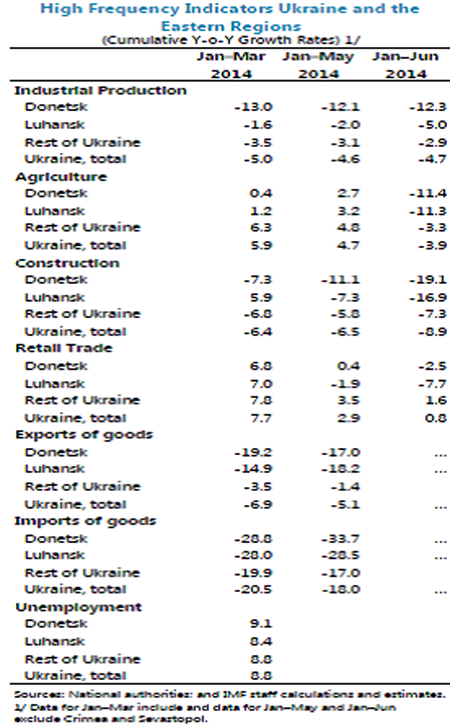

The following IMF staff tabulation also indicates how much economic and fiscal damage to the eastern regions, and to the country as a whole, the war has already done. Independently, World Bank sources say the government in Kiev is not disclosing these data. According to the IMF, it has compiled the evidence on the basis of reports from Kiev, plus “estimates and calculations”. This allows for the possibility of substantial under-reporting and under-counting.

Several admissions are made in the IMF staff report which Gueorguiev and Lotze refused to acknowledge when asked in August. Ukrainian compliance with the IMF’s loan conditions – called “performance criteria” or PCs in the staff report – has already collapsed. “Two end-July PCs are estimated to have been missed; and the end-2014 targets are out of reach”, the report says on its cover page.

As for where the IMF money which has been paid into the Ukrainian banks has gone, the report discloses at page 7: “net capital and financial account outflows were larger than expected by some US$2 billion. While rollover rates for banks and corporate entities were more robust [sic] than expected at the time of the program request, net FDI registered an outflow, and the banking system faced large foreign currency outflows (US$3.1 billion). Capital controls likely prevented larger outflows, but were not fully effective in stemming them.”

In short, of the $3.2 billion disbursed to the Ukrainian treasury by the IMF at the start of May, $3.1 billion had disappeared offshore by the middle of August. The role of the leading Ukrainian banks, and of the Kiev officials allied with them, in arranging this was reported here.

The IMF staff also reported to the Fund directors that it has lost confidence in Governor Gontareva (right) and the NBU as a custodian of the IMF loan money. “[The NBU’s] balance sheet is under strain because of the increasing holdings of government securities and liquidity support to commercial banks. The proportion of government securities and loans to banks increased from 28 percent of NBU total assets at end-2010 to 56 percent at end-April 2014. Second, the NBU’s financial autonomy has been undermined by advance profit distributions to the state budget, which were based on the annual state budget laws rather than permitted amounts under the NBU Law and have significantly eroded the NBU’s financial position…Finally, from a governance perspective, the assessment found that the NBU Council’s mandate is limited and substantial revisions to the NBU’s legal framework are needed to establish sound oversight arrangements of its daily management.” (Page 9.)

The IMF staff also reported to the Fund directors that it has lost confidence in Governor Gontareva (right) and the NBU as a custodian of the IMF loan money. “[The NBU’s] balance sheet is under strain because of the increasing holdings of government securities and liquidity support to commercial banks. The proportion of government securities and loans to banks increased from 28 percent of NBU total assets at end-2010 to 56 percent at end-April 2014. Second, the NBU’s financial autonomy has been undermined by advance profit distributions to the state budget, which were based on the annual state budget laws rather than permitted amounts under the NBU Law and have significantly eroded the NBU’s financial position…Finally, from a governance perspective, the assessment found that the NBU Council’s mandate is limited and substantial revisions to the NBU’s legal framework are needed to establish sound oversight arrangements of its daily management.” (Page 9.)

Instead of supporting Gontareva’s claim that she has already completed the Ukrainian bank audits required by the IMF, and to everyone’s satisfaction in Kiev and Washington, the staff report now discloses the process has yet to begin. “Staff and the [Ukrainian] authorities agreed that proper procedures to monitor the quality of pledged loans, detect collateral quality deterioration, and seek its replacement by performing assets should be established in order to reduce the central bank’s risk exposure.” “Should”, the subjunctive form of the verb, isn’t even as certain as the future form, “shall”.

Even in the most optimistic scenario, Gueorguiev’s report concedes that the Ukrainian banking system will continue to drag down the NBU, and with it, the IMF loan money. “Based on reported bank data for May 2014, preliminary staff stress tests estimate that the system NPLs [non-performing loans] (under the NBU definition) would increase by half by end-2016 under the baseline (to 21.5 percent from 14.7 percent) and almost double under an adverse scenario (to 27.1 percent from 14.7 percent). Assuming that banks were to keep a provision ratio of 60 percent of NPLs, the banking system would need to receive fresh resources in the range of 3.5–5 percent of GDP to meet capital targets of Tier I capital of 7 percent in the baseline and 4.5 percent under the adverse scenario.3 This range raises the lower bound of the capital need, compared to earlier staff estimates of 1.6–5 percent of GDP. Accordingly, staff has revised its projected public sector resources allocated to support bank restructuring from 1 percent of GDP to a more conservative 2.8 percent of GDP over 2014–15, including 0.8 percent of GDP for the Deposit Guarantee Fund (DGF).”

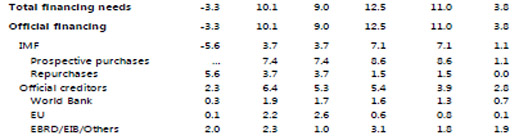

What the technical wording conceals is the amount of extra cash that will be required to prop up the Ukrainian banks: 2.8% of GDP, according to the revised IMF estimates, amounts to between $4 and $5 billion. That must come on top of the $17.1 billion already being spent on other purposes. This table, extracted from a larger one at page 43 of the staff report, indicates by how many billion dollars the IMF loan will fall short of the estimated financing need in Kiev. The numbers also indicate why the European Union and World Bank aid programmes for the country also fall far short.

UKRAINE: IMF PROGRAM SCENARIO – EXTERNAL FINANCIAL REQUIREMENTS

(billions of US dollars)

So, what do Gueorguiev, Thomsen, and Lagarde have to say to convince the IMF board that the government in Kiev isn’t already a deadbeat, the Ukrainian economy a black hole, and that no amount of money can be loaned which has a reasonable likelihood of being repaid? “Ukraine’s capacity to repay the Fund,” concludes the staff report, “remains adequate under the baseline, but is subject to exceptionally high risks.” As for those risks, the report also makes clear that the civil war must stop soon, or else the there can be no reasonable likelihood of repayment. “The program hinges crucially on the assumption that the conflict will begin to subside in the coming months. Should active fighting continue well beyond that, the small buffers under the revised baseline would be quickly exhausted, requiring a new strategy, including additional external financing. A further heightening of geopolitical tensions could also have significant economic consequences. Domestically, policymaking may become more difficult in case of early elections.”

Gabriel Sterne, an Oxford University economist with demonstrable hostility to Russian policy towards Ukraine, has dismissed the IMF’s probability estimates and the repayability assumption on which they depend.

In Moscow the Finance Ministry was asked this morning to confirm whether Russia had voted on the IMF board in favour of the second payment to Ukraine, and whether the Russian directors had put into the record their concerns about Ukrainian government compliance with the loan conditions. Storchak’s spokesman replied:

“In general, the decision was adopted to continue the Fund’s programme for Ukraine, while Russia did not vote against this decision.

However, Russia’s representative in the IMF, along with colleagues from several other countries, including the BRICS, expressed serious concern at the deterioration of a number of key macroeconomic indicators (balance of payments deficit, inflation, rising debt levels, etc.) compared to the original figures contained in the Programme for Ukraine in April. Similar conclusions, as well as a list of the key risks are present, and in the conclusion of the IMF mission [report]. [We] cannot exclude that a further increase in risks will lead to a need to revise the programme in December, when there will be a discussion on whether to provide the next tranche. In any case, the Ministry of Finance will continue to monitor the situation in the Ukrainian economy.”

Leave a Reply